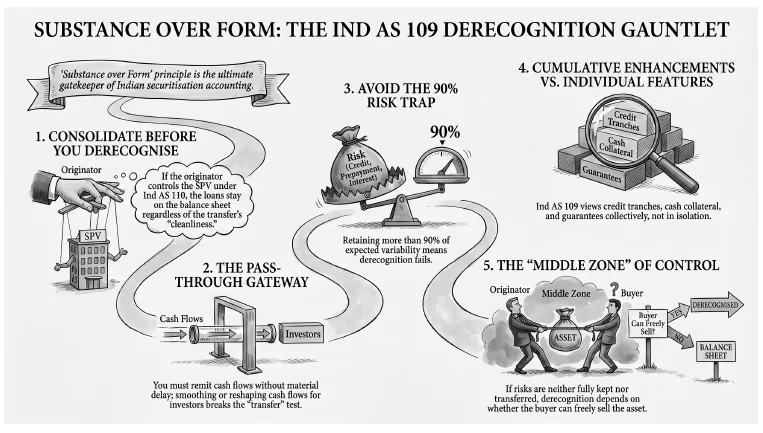

Every quarter, Indian NBFCs and housing finance companies announce securitisation transactions that improve capital ratios, unlock liquidity, and signal disciplined balance sheet management. Yet some of those same transactions are later revisited and, in certain cases, restated as secured borrowings. The issue is rarely legal or structural. It is accounting; specifically, the misapplication of the derecognition requirements under Ind AS 109.

This article walks through where Indian structures most often fail: cumulative credit enhancements that leave economic risk with the originator, servicing arrangements that go well beyond administration, pass-through mechanics that look compliant on paper but are not, and a persistent under-appreciation of partial derecognition and continuing involvement. It also sets those requirements against the parallel; and sometimes divergent; framework under the RBI’s 2021 Master Directions. The aim is to give practising CAs a clear, working framework grounded in the actual decision tree in Ind AS 109.

1. GETTING THE SEQUENCE RIGHT: WHAT IND AS 109 ACTUALLY DOES

The derecognition model in Ind AS 109 is more structured than the familiar “cash flows – risks and rewards – control” shorthand suggests. In practice, five questions have to be answered in the right order.

Step 0: Consolidate First (Ind AS 109 para 3.2.1 read with Ind AS 110)

Derecognition is assessed only after all subsidiaries, including securitisation SPVs and other structured entities, are consolidated under Ind AS 110. If the originator controls the SPV, the loans stay on the consolidated balance sheet regardless of how clean the transfer looks at the SPV level.

This is not a theoretical nicety. Many Indian securitisation SPVs are thinly capitalised, bankruptcy-remote entities with activities narrowly defined by trust deeds and transaction documents. Depending on how decision-making, exposure to variable returns, and key rights are structured, an originator may well have to consolidate such an SPV. Once it does, derecognition at the consolidated level is off the table, even if the SPV itself would have met all the tests.

Step 1: Whole Asset or Component? (para 3.2.2)

The standard next asks whether derecognition should be applied to:

- The entire financial asset (or pool); or

- Only to a part of it.

A part qualifies only if it is:

1. A specifically identified stream of cash flows (for example, only the interest cash flows); or

2. A fully pro-rata share of all cash flows (for example, a vertical 60% interest in every rupee of principal and interest); or

3. A fully pro-rata share of specifically identified cash flows.

Many Indian direct assignment deals and tranche structures sit exactly here: the originator may be transferring, say, the senior 80% of principal cash flows but retaining all excess spread and certain loss-absorbing pieces. If the structure does not fit one of the three categories above, the derecognition analysis applies to the entire asset, not just to the “sold” slice.

Step 2: Have the Rights Expired? (para 3.2.3)

If contractual rights to the cash flows have simply expired; because the loan has been repaid, cancelled, or written off; derecognition follows without further analysis. In securitisation, this is rarely the path; most transactions involve transfers rather than expiries.

Step 3: Has There Been a “Transfer” at All? (paras 3.2.4–3.2.5)

Only now does the standard ask whether the entity has transferred the asset. This can happen in two ways:

1. Transfer of contractual rights to receive cash flows; or

2. Pass-through arrangements, where the originator retains legal title and the right to collect cash flows, but is contractually obliged to pass them on.

The three well-known pass-through conditions (no obligation to pay unless collected; no ability to sell/pledge the asset except as security; remittance without material delay and without reinvestment) sit here in the decision tree. They answer a narrow gateway question: has a transfer occurred at all?

They are not an alternative route that can be invoked when the risks-and-rewards analysis is uncomfortably close. In other words, an originator does not get to say: “The risks and rewards outcome is borderline, so we will instead rely on the pass-through test.” If the contractual rights have been transferred outright, the pass-through limb is simply not engaged.

Step 4: Have Substantially All Risks and Rewards Moved? (paras 3.2.6–3.2.8, B3.2.4–B3.2.5)

Once a transfer is established, the core question is whether the originator has:

- Transferred substantially all risks and rewards of ownership;

- Retained substantially all of them; or

- Landed in the middle, having transferred some but not most.

The standard is deliberately silent on a numeric threshold. The task is to look at the variability of the asset’s future net cash flows before and after the transfer, across reasonably possible scenarios, and to ask who is bearing that variability.

Crucially, “variability” under Ind AS 109 is not a synonym for “credit loss”. The application guidance identifies a broader set of risks and rewards that have to be considered to the extent they are applicable to the specific asset — including credit risk, interest rate risk, prepayment risk, late payment risk, foreign exchange risk, and equity price risk. For a typical Indian retail loan pool — home loans, vehicle finance, unsecured consumer lending — credit and prepayment risk are usually the two dominant drivers of net cash flow variability, and interest rate risk can become material in longer-tenor floating-rate pools. A scenario framework that tests only credit loss paths will, by construction, miss the prepayment and interest-rate channels through which risk is often retained.

In practice, a convention has developed:

- If the originator bears more than around 90% of the expected variability in cash flows, it is viewed as having retained substantially all risks and rewards.

- If it bears less than about 10%, it is generally seen as having transferred substantially all risks and rewards.

That convention draws on IASB implementation guidance and market practice; it is not a safe harbour in the standard. Two cautions follow.

First, the convention should be applied to total variability across all applicable risks, not to credit losses alone. A structure where a senior investor bears material prepayment or interest rate risk but minimal credit risk may show a very different overall variability picture from what a credit-loss-only scenario would suggest — in either direction.

Second, applying the convention mechanically, without examining which risks are being retained, can itself produce wrong answers. A structure where an originator keeps a small, deeply subordinated tranche that absorbs virtually all default losses may fail derecognition even if that tranche is “only” 10–15% of the pool. Conversely, a structure that appears to leave significant residual loss exposure with the originator may, once prepayment and interest rate risk are modelled alongside credit risk, land in the middle zone rather than in outright failure.

Step 5: Control and Continuing Involvement (paras 3.2.9, 3.2.16–3.2.21)

If the risks-and-rewards analysis is clearly one-sided, the answer is simple:

- Substantially all transferred → derecognise.

- Substantially all retained → continue to recognise and treat proceeds as a secured borrowing.

The interesting cases sit in the middle zone, where the originator has neither transferred nor retained substantially all risks and rewards. Here, the standard asks: has control been retained?

- If the transferee has the practical ability to sell the asset in its entirety to an unrelated third party, unilaterally and without further restrictions, the originator has not retained control and derecognition of the entire asset follows, with separate recognition of any continuing involvement (for example, guarantees or options).

- If that ability is missing, the originator is deemed to have retained control and must apply the continuing involvement approach: it keeps the asset on the balance sheet to the extent of its continuing involvement, with the remainder derecognised.

This is an important nuance that tends to be glossed over. Derecognition is not always all or nothing. For guarantees, written or purchased options, or limited credit support, the standard requires

a partial derecognition outcome where the carrying amount of the asset is split between the transferred and retained exposures with reference to the originator’s exposure to changes in the asset’s value.

In the Indian context, this matters for structures with limited first-loss pieces, restricted clean-up calls, or specific loss guarantees: they may support partial derecognition combined with a continuing involvement balance, rather than a simple “keep the whole pool on the books” answer.

2. WHAT A DEFENSIBLE DERECOGNITION FILE LOOKS LIKE

Before getting into the failure points, it is worth front-loading the one thing that tends to be an afterthought in busy closings: documentation. A derecognition conclusion that cannot be traced back to contemporaneous analysis is, in practical terms, a weak conclusion.

At a minimum, a robust file should contain:

1. Scope and consolidation analysis

2. Comprehensive enhancement and support inventory

- All contractual credit enhancements (first-loss pieces, cash collateral, sub-loans, guarantees, liquidity or timing facilities, over-collateralisation, excess spread traps).

- Any implicit or reputational support that management regards as likely in stress scenarios.

3. Probability-weighted scenario analysis

- Base, stress, and severe stress scenarios modelled across all material risks — credit loss, prepayment, and, where relevant, interest rate and foreign exchange risk. A credit-loss-only model is not sufficient evidence of who bears variability.

- Who absorbs what share of losses and upside across those scenarios; how much of the overall variability, aggregated across risks, the originator still bears.

4. Cash flow routing and pass-through mechanics

- Actual collection account structures, sweep instructions, and timing.

- Assessment of commingling, reinvestment rights, and any timing mismatches between collections and investor payouts.

5. Control and continuing involvement analysis

- Whether transferees can sell or refinance their positions without originator consent.

- Treatment of options, guarantees, and limited recourse clauses and their impact on continuing involvement and partial derecognition.

6. Legal and regulatory overlay

- True sale and bankruptcy-remoteness opinion under Indian insolvency law, including learnings from cases such as DHFL.

- Interaction with the RBI’s Master Direction on Securitisation of Standard Assets; especially where regulatory capital treatment diverges from accounting derecognition.

7. Conclusion memorandum

- A clear statement of the derecognition conclusion (full, partial with continuing involvement, or none) and, where applicable, the gain or loss on derecognition and servicing asset/liability treatment.

This is not gold-plating. For a judgement that can move capital ratios, headline profit, and regulatory perceptions, it is the bare minimum.

3. WHERE INDIAN STRUCTURES ACTUALLY BREAK

With that framework in place, it becomes easier to see where Indian securitisations most often run into trouble.

This is not a theoretical concern. RBI inspection findings and supervisory communications over the past several years have documented instances where securitisation transactions; including those by prominent NBFCs; were reclassified as secured borrowings following regulatory review, with consequential impact on reported capital ratios and profit.

3.1 The Credit Enhancement Trap

Consider a vehicle finance company securitising a ₹1,000 crore retail pool. The AAA-rated senior tranche; 75% of the pool; is placed with investors. The originator retains a 10% first-loss piece plus several other forms of support. On paper, investors hold the majority. In substance, the risk picture can be very different.

Suppose a simplified probability-weighted loss analysis looks like this (losses as a percentage of the pool):

| Scenario |

Probability |

Pool Loss |

Loss borne by originator |

Loss borne by investors |

| Base |

50% |

2% (₹20) |

2% (₹20) |

0 |

| Stress |

40% |

6% (₹60) |

6% (₹60) |

0 |

| Severe stress |

10% |

15% (₹150) |

10% (₹100) |

5% (₹50) |

The originator’s expected share of loss is:

- 0.50 × 20 + 0.40 × 60 + 0.10 × 100 = ₹44.

Total expected loss on the pool is:

- 0.50 × 20 + 0.40 × 60 + 0.10 × 150 = ₹49.

So, although investors have bought 75% of the notes, the originator is still swallowing roughly 90% of the expected credit loss. That is very close to the “substantially all” line even before considering other forms of continuing exposure.

The problem is compounded when enhancements are reviewed one at a time and signed off in isolation:

- First-loss tranche? Market standard.

- Cash collateral? Rating-driven and prudent.

- Subordinated loan to the SPV? Necessary capital structure.

- Corporate guarantee on senior notes? Investor comfort.

Ind AS 109 does not permit this piecemeal lens. Enhancements have to be viewed cumulatively. A stylised snapshot of typical features makes the point:

| Enhancement Mechanism |

Typical Quantum |

Derecognition Risk |

Core Concern |

| First-loss tranche retention |

8–12% |

High |

Absorbs most probable credit losses |

| Cash collateral account |

7–10% |

High |

Funded exposure remains with originator |

| Excess spread trapping |

Variable |

Medium–High |

Ongoing residual interest in pool performance |

| Corporate guarantee (senior) |

Full / Partial |

Very High |

Near-complete protection to investors |

| Liquidity / timing advances |

5–8% |

Medium |

Can morph into credit risk if advances are unrecoverable |

| Subordinated loan to SPV |

10–15% |

High |

Originator is economically subordinated |

In one consumer finance deal I observed, there was no explicit first-loss tranche at all; a fact the treasury team leaned on heavily in conversations. On closer reading, the structure featured a sizeable cash collateral account, a subordinated loan to the SPV, a mechanism to trap excess spread, and a timing guarantee. Individually, none of those elements was outside what the market would consider normal. Taken together, they left investors with very little exposure to the pool’s everyday credit risk.

When the numbers were run, the originator’s exposure to variability easily crossed the 90% line. Derecognition failed. The genuine surprise within the deal team at that conclusion says something about how strongly “form” still dominates “substance” in many structuring discussions.

3.2 Servicing: When Administration Turns into Ownership

In India, it is almost a given that the originator continues as servicer. Changing EMI mandates for hundreds of thousands of borrowers, re-documenting security, and altering customer communication flows is expensive and often undesirable. The question is not whether the originator services. It is how.

In one mortgage securitisation, the core sale documents were clean. The real issues lived in the 50-page servicing agreement. Three provisions, taken together, changed the analysis from “agent” to “principal”:

1. Advance servicing fee: the servicer was paid, upfront, the present value of three years of expected servicing fees. If the pool performed poorly, its future workload would fall, but its remuneration would not. That is not a straightforward fee; it is an exposure to pool performance.

2. Clean-up call: the servicer had the right to repurchase the residual pool once it fell below a fixed percentage of original balance. Clean-up calls are common globally, but when combined with local court practice and insolvency risks, an option that can be exercised precisely when the remaining loans are the most distressed has to be examined as a potential continuation of risk.

3. Delinquency repurchase right: any loan hitting 90 DPD could be repurchased at par “for administrative convenience”. Economically, this looked very much like a guarantee on early defaults; the riskiest part of the curve.

The derecognition conclusion was not difficult. This was not a neutral servicing mandate. It was a bundle of rights and obligations that left the bank materially exposed to the same credit risk it claimed to have sold.

Where derecognition does succeed and servicing is retained, there is a further accounting step that is often overlooked:

- If the expected fees for servicing are higher than the consideration the market would require for such services, a servicing asset is recognised.

- If the expected fees are lower, a servicing liability arises.

In both cases, Ind AS 109 requires that the original carrying amount of the asset be allocated between:

- The portion derecognised; and

- The retained servicing right (asset or liability);using their relative fair values at the date of transfer. This “splitting” is not an optional nicety; it is part of the derecognition mechanics.

3.3 Pass-Through: Why the Gateway Test Often Fails in Practice

Where the originator has not transferred the contractual rights to receive cash flows, derecognition is only possible if the arrangement qualifies as a pass-through transfer. That requires all three conditions in para 3.2.5 to be met:

1. No obligation to pay the eventual recipients unless equivalent amounts are collected from the asset;

2. No ability to sell or pledge the asset other than as security for the obligation to pay the recipients;

3. An obligation to remit cash flows without material delay and without reinvestment except in cash or cash equivalents during the settlement period.

In one direct assignment, for operational reasons, borrower EMIs continued to hit originator-controlled accounts. The originator swept funds to the SPV monthly, retained any excess as a “performance incentive”, and advanced shortfalls to ensure investors were paid on schedule; recovering those advances from future excess collections.

Every feature had a commercial explanation. Taken together:

- EMIs were commingled in originator accounts for the better part of the month.

- The “performance incentive” created a continuing residual interest well beyond a pure servicing fee.

- Investor cash flows followed a predetermined schedule, not the actual timing pattern of underlying collections.

From an Ind AS 109 standpoint, the originator had not passed cash flows through. It was managing timing differences, bearing gaps, and sharing upside. The gateway “transfer” test failed; the risks-and-rewards and control tests never even properly arose.

This is not an isolated pattern. Monthly waterfalls; standard in Indian securitisation; are not automatically fatal, but they do create timing differences that need to be weighed against the “no material delay” requirement. Where the originator is, in substance, smoothing and reshaping cash flows, a pass-through conclusion is difficult to sustain.

4. PARTIAL DERECOGNITION AND CONTINUING INVOLVEMENT: THE MIDDLE GROUND

Indian practice often treats derecognition as a binary choice: either the pool is off the books or it is not. Ind AS 109 is more nuanced.

Where:

- The originator has transferred the asset (or a qualifying part under para 3.2.2);

- It has neither transferred nor retained substantially all risks and rewards; and

- It has retained control; the standard requires recognition of the asset to the extent of continuing involvement.

The most common forms are:

- A limited credit guarantee on transferred receivables;

- Written or purchased put and call options;

- Deeply subordinated residual interests or credit-enhancing interest-only strips.

In such cases, the carrying amount of the asset is split into:

- A portion that is derecognised; and

- A portion that continues to be recognised, measured by reference to the originator’s maximum exposure to changes in the asset’s value.

The associated liability or derivative is measured separately. This approach is particularly relevant where the originator’s support is capped (for example, a guarantee limited to 10% of principal). Treating such structures as a complete failure of derecognition over-states the asset on the originator’s balance sheet and understates the transfer that has actually occurred.

5. IMPLICIT SUPPORT: THE PRESENT AND THE FUTURE

Ind AS 109 and Ind AS 107 both address implicit support; situations where the originator, though not contractually obliged, steps in to support a securitised pool. The standard is clear on two fronts.

First, for the current transaction:

• If assets have been derecognised and the originator later provides non-contractual support; by making good shortfalls, waiving fees, or absorbing losses; the derecognition conclusion must be revisited. Depending on the nature and extent of support, the originator may have to recognise:

- A new financial asset;

- A guarantee or other liability; or

- In some cases, a renewed continuing involvement in previously derecognised assets.

Second, for future transactions:

- Once an originator has demonstrated a pattern of stepping in to protect investors beyond contractual terms, users of the financial statements; and, importantly, auditors and regulators; are entitled to assume that similar support is likely in future deals.

- IFRS 7 (Ind AS 107) explicitly contemplates this forward-looking dimension: disclosures are required that enable users to understand both the support actually provided and the extent to which derecognition conclusions on future transfers may be affected by that history.

For practitioners, the practical takeaway is uncomfortable but unavoidable: a one-off “reputational” support decision can cast a long shadow. It not only creates an immediate accounting event; it also colours the derecognition analysis for every subsequent securitisation the originator undertakes.

6. A WORKED NUMERICAL EXAMPLE

An end-to-end illustration helps to see how the pieces fit together.

6.1 Structure and Assumptions

• Originator holds a homogeneous retail loan pool:

- Gross carrying amount: ₹1,000

- Loss allowance (ECL): ₹20

- Net carrying amount: ₹980

• The originator transfers the pool into an SPV, which issues notes as follows:

- Senior notes of ₹900 sold to investors.

- Subordinated notes of ₹100 retained by the originator.

- The originator also acts as servicer, receiving an annual fee equal to 0.75% of outstanding principal.

Assume:

- The fair value of the entire pool at the date of transfer is ₹1,020.

- Fair value of the senior notes issued is ₹918.

- Fair value of the subordinated notes retained is ₹94.

- Fair value of the servicing right (based on expected fee flows versus market servicing fee) is ₹8.

Total fair value of the pieces (₹918 + ₹94 + ₹8 = ₹1,020) matches the fair value of the pool.

6.2 Risk and Reward Analysis

A probability-weighted loss analysis similar to the earlier example suggests:

Total expected credit loss on the pool: ₹49.

Expected loss absorbed by the subordinated tranche: ₹44.

The originator therefore bears about 90% of expected credit loss through its subordinated notes. There is no other credit enhancement beyond this tranche. On these numbers alone, and looking only at credit loss, most audit and regulatory reviewers would conclude that substantially all credit risk has been retained. A 90% absorption of expected credit loss sits squarely in the territory where, in practice, the risk-and-reward test is treated as failing — not as an ambiguous middle-zone outcome. The reader should not take 90% as a number that supports derecognition with continuing involvement; in isolation, it does not.

Two considerations, however, are worth running through before closing the analysis:

The subordinated tranche is capped at ₹100. In a truly severe tail scenario, losses above that cap flow through to investors. The absolute ceiling on originator loss is a relevant data point even if the expected-loss share is heavily skewed.

Credit loss is only one dimension of variability. Prepayment risk, interest rate risk, and — where relevant — foreign exchange risk have to be brought into the same calculation. In this example, those risks are borne broadly pro-rata by senior and subordinated holders, so they do not shift the conclusion. In a mortgage pool, they typically would.

Two treatment paths therefore need to be illustrated.

Path A — Risk-and-reward test fails (the likely conclusion on these numbers). The originator has retained substantially all risks and rewards. The pool continues to be recognised on the balance sheet in full. The proceeds of ₹918 received on the senior notes are accounted for as a secured borrowing. No gain on derecognition arises. Interest income on the pool continues to be recognised; interest expense on the borrowing is recognised separately. This is the outcome practitioners should expect to reach on facts of this kind.

Path B — Risk-and-reward outcome is genuinely inconclusive. The numbers above, combined with a fuller scenario model that brings prepayment and interest-rate variability into the frame, may in some structures produce an overall variability share for the originator that is materially below the 90% credit-loss figure — for example, where heavy prepayment optionality in the underlying loans is in substance passed through to investors. Where that fuller modelling pushes the overall variability share into the 40–60% range across the full risk spectrum, the transaction sits in the middle zone and control has to be tested. If the transferee has the practical ability to sell the senior notes freely to an unrelated third party, control has not been retained, and the pool qualifies for derecognition in full with separate recognition of continuing involvement (the subordinated notes and the servicing right). Section 6.3 works through the mechanics for this path, so that the allocation methodology under Ind AS 109 is visible end-to-end.

6.3 Allocation of Carrying Amount and Gain Recognition

The mechanics that follow assume Path B has been reached — that is, that fuller modelling of credit, prepayment and interest rate risk together has placed the originator’s overall variability share within the middle zone, and that the control test (free saleability of the senior notes by the transferee) is satisfied. The allocation and gain computation below then follows.

Ind AS 109 now requires the originator to allocate the net carrying amount of ₹980 between:

- The portion derecognised (cash flow rights sold via the senior notes);

- The retained subordinated interest; and

- The servicing right.

Using relative fair values:

- Senior notes: 918 / 1,020 = 90%

- Subordinated notes: 94 / 1,020 ≈ 9.2%

- Servicing right: 8 / 1,020 ≈ 0.8%

Allocated carrying amounts:

- To derecognised portion: 90% × 980 ≈ ₹882

- To retained subordinated interest: 9.2% × 980 ≈ ₹90

- To servicing asset: 0.8% × 980 ≈ ₹8

(rounded totals reconcile to ₹980).

Accounting entries at the originator level, assuming the transaction falls within Path B of Section 6.2, would be, in simplified form:

- Dr Cash: ₹918 (proceeds for senior notes)

- Dr Investment in subordinated notes: ₹94 (initial recognition at fair value — see classification note below)

- Dr Servicing asset: ₹8

- Cr Loans (pool): ₹980 (derecognition of carrying amount)

- Cr Gain on derecognition: ₹40 (balancing figure in this simplified illustration)

Two points on the mechanics are important, because the entry above is easily misread.

Classification of the retained subordinated notes.

The debit of ₹94 is the fair value at the date of transfer. The allocated carrying amount of the retained interest is ₹90 (9.2% × ₹980, per the allocation above). The subordinated notes can be recorded at fair value at inception only if their classification under Ind AS 109 supports that measurement basis. In a typical securitisation structure, the subordinated tranche is designed to absorb credit losses before the senior tranche is touched. Its contractual cash flows are therefore unlikely to represent solely payments of principal and interest on the principal amount outstanding — the subordination feature itself introduces exposure going beyond basic lending risk. In most Indian structures, a subordinated tranche of this kind will fail the SPPI test and be classified at fair value through profit or loss. If the instrument is at FVTPL, the ₹4 difference between the allocated carrying amount (₹90) and the fair value (₹94) flows through P&L on Day 1 alongside the derecognition gain. If, on the specific facts of a transaction, the retained interest does satisfy SPPI and the relevant business model, it would be carried at amortised cost at the allocated carrying amount of ₹90, and the ₹4 gap would not be recognised up front. The classification analysis is therefore not a footnote — it drives the numbers.

The ₹40 gain as a balancing figure.

The gain of ₹40 is shown here as the residual that makes the entry balance under Path B assumptions. The formal computation under Ind AS 109 is prescribed by paragraph 3.2.12 (difference between the carrying amount measured at the date of derecognition and the consideration received, including any new asset obtained less any new liability assumed), and the application methodology for structures of this kind — allocating the carrying amount of the larger financial asset between the part derecognised and the parts retained, based on relative fair values — is worked through in paragraph 3.2.13 and the application example at B3.2.17. Practitioners applying the framework to their own transactions should work from those paragraphs rather than from the stylised entries above; the actual gain will depend on the classification of each retained component and on the relative-fair-value inputs at the date of transfer.

The conceptual takeaway remains:

- The gain or loss on derecognition is recognised immediately in profit or loss under Ind AS 109.

- The originator recognises a servicing asset and a retained investment, both measured and tracked separately going forward — the retained investment in accordance with the classification and measurement requirements applicable to it.

6.4 RBI Guidelines: Why the Gain May Still Not “Count”

Under the RBI’s 2021 Master Direction on Securitisation of Standard Assets, gains arising from securitisation are typically not available for immediate distribution or unrestricted capital recognition. They are required to be amortised over the life of the transaction or appropriated to a separate reserve.

This creates an explicit and deliberate tension:

- Ind AS 109 wants the full derecognition gain in profit or loss on Day 1.

- The RBI wants the economic benefit of that gain to emerge in regulatory capital and distributable profits only over time.

NBFCs and HFCs have addressed this in practice by:

- Recognising the full gain in P&L in accordance with Ind AS 109; and

- Creating a corresponding appropriation; often styled as a “securitisation reserve”; to align with the RBI’s requirement that gains be spread over the life of the transaction.

From a practitioner’s standpoint, this means that a transaction can pass the derecognition tests robustly and yet leave management explaining why the large headline gain it produced does not translate into immediate regulatory capital relief.

7. REGULATORY CAPITAL VS ACCOUNTING DERECOGNITION

The RBI’s Master Direction on Securitisation of Standard Assets sits alongside Ind AS 109 and often answers a different question: how much regulatory capital relief does this transaction justify?

Two points are worth underlining.

1. The RBI’s framework focuses on:

- Minimum Retention Requirement (MRR);

- Minimum Holding Period (MHP);

- True sale and bankruptcy remoteness;

- Limits on total retained exposures (for example, the 20% cap on total exposure to a securitisation structure, excluding certain interest-only strips).

A transaction that fails accounting derecognition because the originator still bears, say, 80% of the expected credit loss may still satisfy the RBI’s conditions for regulatory capital relief, provided the formal criteria around MRR, MHP and true sale are met.

2. The reverse is also possible. A structure might satisfy Ind AS 109’s derecognition tests; particularly in synthetic arrangements or highly tailored tranche designs; but not qualify for capital relief under the Directions.

The practical implication is that “failed derecognition” in accounting terms is not automatically a failure in regulatory terms. CAs advising boards and audit committees need to keep those frameworks separate in their analysis and in their explanations.

8. PARTIAL TRANSFERS IN INDIAN STRUCTURES (PARA 3.2.2 IN PRACTICE)

Partial derecognition is not merely a theoretical corner case; it is directly relevant to common Indian structures:

- Direct assignments where only specific interest cash flows or a pro-rata share of all cash flows are sold;

- Transactions where senior tranches are sold but junior tranches and excess spread are retained;

- Deals involving interest-only or principal-only strips.

Where the part transferred is:

- A specifically identified cash flow stream (for example, only interest), or

- A fixed pro-rata slice of all cash flows,

Ind AS 109 allows derecognition of that part, provided the rest of the decision tree is satisfied for that component. The remaining part of the asset continues to be recognised.

This matters in practice because it prevents an originator from packaging a subordinated tranche and a residual spread into a single amorphous “retained interest” and then treating the sold tranche as if it were the whole asset for derecognition purposes. Paragraph 3.2.2 forces an explicit analysis of what exactly is being sold and what is being retained.

9. CO-ORIGINATION, IBC, AND TRUE SALE: LEARNING FROM DHFL

Co-origination structures; where NBFCs and larger banks jointly originate loans and then one party seeks to securitise or assign its share; raise questions that go beyond pure credit analysis.

The DHFL proceedings brought that into sharp relief. In that case, receivables that had been assigned to third parties came under a court-ordered freeze when DHFL entered insolvency, at least in the initial stages of litigation. Although the legal position was later clarified and reinforced in favour of bankruptcy remoteness, the episode highlighted two uncomfortable facts:

- A transaction that looks like a clean assignment on paper can still be caught in the slipstream of an originator insolvency, at least temporarily, if courts or resolution professionals take a broad view of the estate.

- For Ind AS 109 purposes, the question of whether contractual rights to cash flows have truly been transferred; and whether the transferee has the practical ability to enforce and sell those rights; cannot be answered by reading the transaction documents in isolation from the insolvency framework and enforcement practice.

In co-origination and similar structures, the continuing relationship between the parties, the way security interests are perfected, and how courts have behaved in stress cases all feed into the derecognition analysis. The DHFL experience should, at a minimum, find its way into the legal and risk sections of any serious derecognition file involving Indian receivables.

10. NEW STRUCTURES, SAME UNDERLYING QUESTIONS

The market is experimenting with forms that did not exist when the early Ind AS 109 guidance for India was written. The decision tree, however, has not changed.

- Synthetic securitisation: credit risk is transferred through credit derivatives or guarantees, while the loans stay on the originator’s balance sheet. Regulatory capital relief may be available if the RBI’s conditions are met. Accounting derecognition is generally not, because contractual cash flow rights remain with the originator and pass-through conditions are not satisfied.

- Co-origination and loan-by-loan assignments: intertwined underwriting, cross-default arrangements, and shared security require careful unpacking before any conclusion can be drawn on whether a qualifying “part” has been transferred and whether risks and rewards have genuinely shifted.

- Portfolio sales to ARCs and private credit funds: earn-outs, upside-sharing arrangements, and minimum return guarantees often create continuing involvement. Those features may block full derecognition at inception or require a continuing involvement model that recognises only partial derecognition.

The questions remain the same:

- Has the right entity been consolidated?

- Is derecognition being applied to the right unit of account; the whole asset or a qualifying component?

- Have contractual rights been transferred or is this merely a funding arrangement?

- Who still bears the real economic variability in cash flows?

- Does the transferee truly control the asset?

- What is the extent of continuing involvement?

11. THE PROFESSION’S ROLE

There is a version of securitisation that works well under Ind AS 109 and under the RBI’s Directions:

- Risk is meaningfully transferred.

- Enhancements are proportionate rather than overwhelming.

- Pass-through mechanisms are clean, operationally as well as legally.

- Servicing arrangements pay for work done without smuggling credit exposure back onto the originator.

- Any residual exposures are transparent, capped, and accounted for under the continuing involvement model.

That version is achievable. The difficulty is that it often conflicts with the instinct to retain upside, protect investor relationships at all costs, and squeeze capital benefits from structures that, in substance, leave the originator still holding the risk.

For CAs in audit, advisory, and industry roles, the obligation is two-fold:

- To understand and apply the full decision tree of Ind AS 109; including consolidation, partial derecognition, pass-through gateways, continuing involvement, and implicit support; rather than relying on a simplified three-question checklist;

and

- To be clear with boards and management teams that accounting conclusions should follow the economic design of the transaction, not the other way around.

Substance, as Ind AS 109 has insisted from the start, is not negotiable.