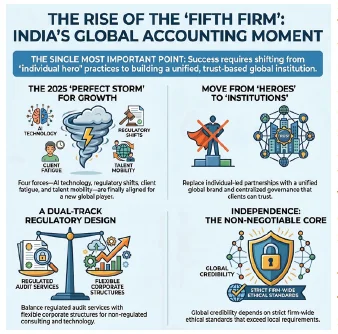

India missed the chance to build a global accounting firm in 2002, but converging forces of technology, client fatigue, and regulatory shifts have reopened the window for a “Fifth Firm.” To succeed, Indian firms must evolve from fragmented, partner-led practices into unified institutions. This requires mastering complex regulatory dimensions across jurisdictions, maintaining strict audit independence, and managing cross-border conflicts. Firms must strategically separate regulated audit from non-regulated advisory services, embracing multidisciplinary structures and external capital to fund growth. Ultimately, Indian firms must view regulation not as a barrier, but as the foundational architecture of trust required for global scale.

1. INTRODUCTION – THE NEED FOR AN INDIAN FIRM WITH A GLOBAL PRESENCE

Some opportunities come once in a generation. They arrive quietly, without hype or hoopla, and leave just as quietly. You recognise them much later, when the world has moved on.

‘Professional Services’ had such a moment when a multinational firm collapsed. The crash opened the doors wide for a new entrant. For someone in India or the Global South. We didn’t seize the moment. We let it go uncashed.

In 2002, Arthur Andersen, the world’s top audit and accounting firm, went Kaput, courtesy of Enron, shredded documents, and broken trust. A once storied entity with over 80,000 professionals across more than 80 countries vanished overnight. The tsunami left many things under the debris, including hope, innocence, and trust.

The four remaining firms—Deloitte, PwC, EY, and KPMG—moved double fast. Within months, they absorbed Andersen’s people, practices, and clients. The Big Five became the Big Four. That moment was the crack through which an Indian firm could have emerged. A firm with different soil, different story, and different DNA. But it didn’t happen.

We lost the opportunity. Andersen disappeared, and the Big Four continued to party. The Fifth never showed up.

Now, in 2025, India has over 400,000 CAs. She is the headquarters for global back offices. She audits global subsidiaries. Her professionals speak the language of IFRS, ESG, and PE exits. Yet, India has not built a single professional services firm to match the Four.

This is the time to build The Fifth firm, in other words a large Indian firm with a global presence which could equal the Big Four at some point in time in the future. Thank fully the Government of India has embarked on the initiative of building more Indian firms to increase the options available in the market place.

AT ITS CORE, WHAT DOES THE FIFTH FIRM REPRESENT?

It represents a choice for clients seeking a longer shortlist. It represents the ability to interpret things through a dual lens, viz., global in structure, but local in insight. It represents the possibility of a world-class institution born not in Europe or America, but in Asia.

‘Professional Services’ remains perhaps the only trillion-dollar industry where four firms hold a vice-like grip. Here, market concentration is mistaken for competence. When clients select a Big Four, they believe they are managing risk. When ambitious talent joins them, they assume it is a shortcut to success.

Unfortunately, the brand has become a proxy for legitimacy. When clients choose a ‘Big Four’ firm they believe their actions would be justified as they have picked one of the best in the business in the belief that the world considers size as equivalent to capability and quality.

This has created a paradox: a high-trust industry with low innovation and zero institutional mobility. And India stays in the second tier. Not because it lacks capability, but because capability alone doesn’t build institutions. To scale globally, you need belief, which today is represented by brand, capital, governance, and an internal culture that can weather storms.

The globalisation of Indian accounting firms cannot be viewed merely as an exercise in opening offices abroad, joining international networks, or serving Indian clients in overseas markets. At its core, it requires the ability to operate within multiple regulatory systems, each with its own rules on licensing, audit eligibility, independence, confidentiality, data protection, quality review, disciplinary jurisdiction and ownership structures. A firm seeking to grow globally must therefore develop not only commercial ambition, but also regulatory awareness and an institutional ability to take considered positions on difficult questions before they arise in client situations.

That’s why dozens of mid-sized firms, some of which are technically excellent and trusted locally, have never crossed the line to achieve global relevance. Because the leap from regional to global isn’t about scale; it’s about design. It requires governance that clients can trust. It needs talent models that retain stars. It should have brand equity that signals both competence and confidence.

This is particularly important because accounting firms occupy a distinctive position in the economy. In advisory services, they compete like professional businesses. In audit and assurance, however, they perform a public-interest function. The audit opinion is relied upon not only by the client that pays the fee, but also by shareholders, lenders, regulators, employees and capital markets. Consequently, global accounting practices must reconcile two sometimes competing impulses: the commercial need to scale and the professional duty to remain independent, credible and ethically consistent.

For Indian firms, this balance will be central to global expansion. The firm of the future may combine audit, tax, transaction advisory, forensic, sustainability, technology and risk consulting services. It may work through Indian partnerships, LLPs, network arrangements, foreign affiliates, corporate entities for non-regulated services, or multi-disciplinary models. Each model creates opportunities, but also raises regulatory and ethical questions.

FOR DECADES, THE FIFTH FIRM FELT OUT OF REACH. BUT TODAY, THE GROUND IS MOVING.

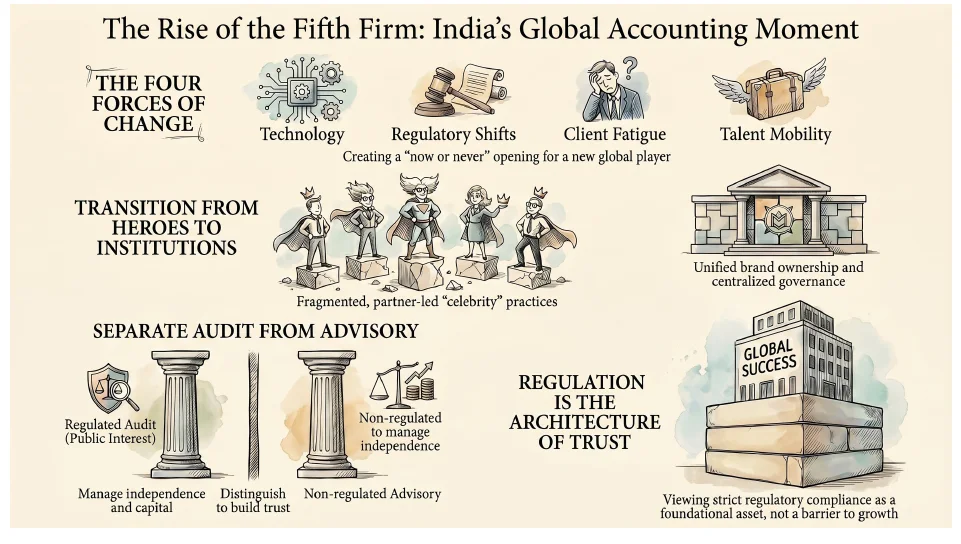

First, there’s technology. AI and automation are transforming the face of delivery. Routine work, such as reporting, reconciliations, and document preparation, is getting commoditised. The traditional advantage of large firms, namely, their scale of delivery, is slipping. The differentiator is shifting from execution to interpretation, from templates to trust. And trust can’t be outsourced.

Second, regulators worldwide (from the UK’s Financial Reporting Council to India’s NFRA) are raising concerns about audit concentration and advisory conflicts. They’re looking for alternatives. The question now is “Why hasn’t someone else done it yet?”

Third, there’s client fatigue. After two decades of transformation programs, PowerPoint decks, and playbooks, clients are becoming less tolerant of generic value. They’re willing to work with smaller, smarter, and more contextually sharp partners—if they can trust them.

Fourth, talent is shifting. Young professionals today are not looking for ten-year ladders and corner-office titles. They want purpose and autonomy.

For the first time in decades, all four forces—technology, regulation, client sentiment, and talent mobility—are moving in the same direction. The forces reshaping this industry are already here. It depends on who steps forward and what they choose to build.

And the timing is not just right. It may be now or never.

2. THE INDIAN REGULATORY BASE: WHAT CAN TRAVEL AND WHAT CANNOT

Indian accounting firms begin their global journey from a regulatory base that is significantly shaped by the Chartered Accountants Act, 1949, the Chartered Accountants Regulations, 1988, the Code of Ethics issued by the ICAI, the Companies Act, 2013, and, for certain audit engagements, oversight by bodies such as the National Financial Reporting Authority. This base is not merely procedural. It determines who may practice, in what form, under what ethical obligations, and with what limitations on services.

A useful distinction must be drawn between regulated services and non-regulated services. Statutory audit, tax audit, certification and certain assurance functions are regulated professional services. They are typically required to be performed by members holding a certificate of practice, and the ability to sign reports is tied to professional registration and disciplinary control. In contrast, many non-assurance services—such as consulting, technology implementation, process transformation, transaction support, business advisory, risk management and outsourcing—may be capable of being delivered through other legal vehicles, subject of course to applicable laws and restrictions arising from independence or professional conduct rules.

This distinction is important for globalisation. If an Indian firm treats all services as though they must be delivered only through the traditional audit partnership model, it may constrain its ability to raise capital, hire non-CA professionals, build technology platforms and compete with integrated global firms. Conversely, if a firm treats all services as commercial services without recognising the regulated character of audit and assurance, it may compromise independence and invite regulatory action.

The corporate entity therefore has a legitimate role in the globalisation debate, particularly for non-regulated services. A limited liability company or other corporate structure may be appropriate for technology consulting, business process services, research support, data analytics, ESG advisory support, training, outsourcing or global capability services, provided it does not hold itself out as performing reserved professional functions and provided conflict, branding and independence issues are properly managed. The challenge is not whether corporate entities should exist around professional firms; they already do in many forms. The more important question is how the relationship between the regulated practice and the non-regulated entity should be governed.

Section 144 of the Companies Act, 2013 illustrates the issue sharply. It prohibits an auditor from rendering specified non-audit services to the audit client, its holding company or subsidiary company, including accounting and book-keeping, internal audit, design and implementation of financial information systems, actuarial services, investment advisory, investment banking, outsourced financial services and management services. The provision also expands “directly or indirectly” to include services through related entities or entities using the auditor’s name, trade mark or brand. This shows that merely shifting a prohibited service to a separate entity may not solve the problem if, in substance, the service remains connected with the auditor or its brand.

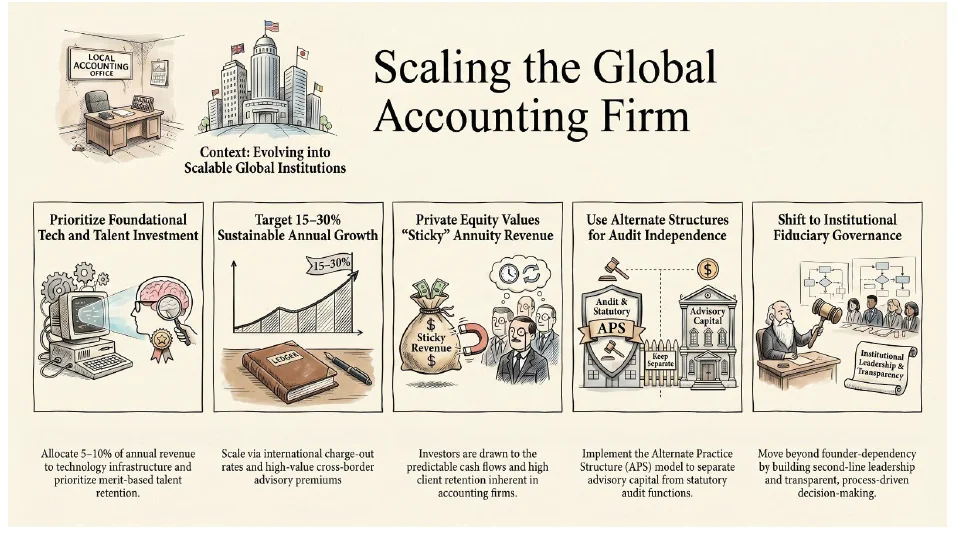

At the same time, the regulatory framework is slowly recognising the need for scale. It began with the setting up of LLP and now leading to allowing Multi Disciplinary Entities to be created. Additionally networks are being encouraged and the regulations around them are evolving despite the reluctance to open it up fully and jettison the past ‘controlled’ culture. Just as India opened up in the early 1990s the recent regulatory are welcome ‘green shoots’. These developments are important not because they immediately create global firms, but because they recognise that the traditional fragmented practice model needs institutional pathways for scale.

The Indian regulatory base, therefore, should not be seen as a barrier to globalisation. It is the starting architecture. But Indian firms must understand what part of that architecture is portable across borders and what part is jurisdiction-specific. The right to audit in India does not automatically create the right to audit in another country. Likewise, a network name may create market recognition, but it may also create independence, liability and quality-control expectations. For global practice, structure must follow regulation; it cannot be designed purely by reference to tax efficiency or branding convenience.

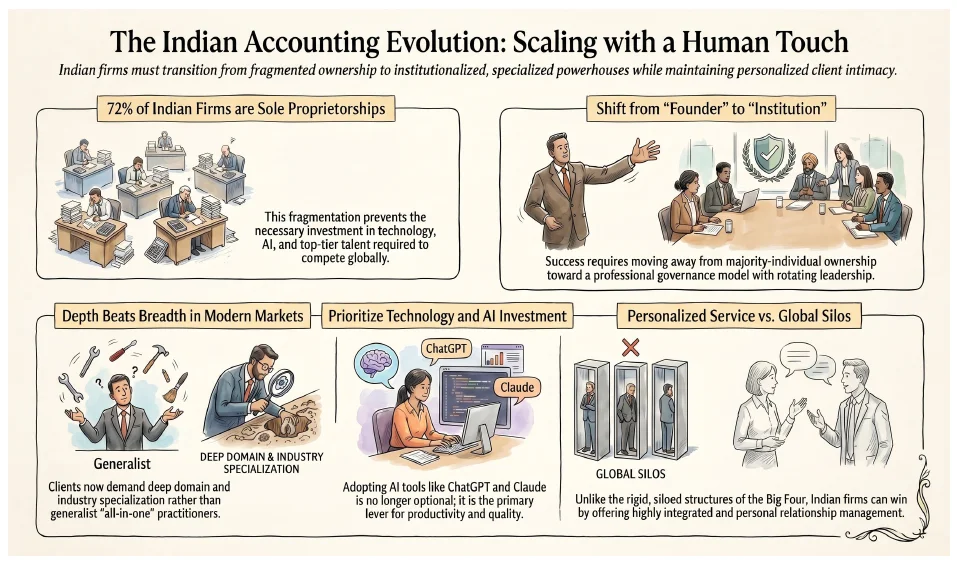

What the Big Four got right was that they built firms, not confederations of partners. In many professions, partnerships evolve into loose alliances of celebrities. There, clients belong to individuals, revenues are jealously guarded, and the firm exists as a shared letterhead. The Big Four resisted this movement, even at the cost of internal friction. They centralised brand ownership, partner admissions, and client acceptance norms. The logo did not belong to any one partner. The firm’s credibility no longer depended on a single individual.

The Key, therefore, is creating a model where no single firm, geography, individual or practice controls the firm. The model should facilitate regulatory compliance, balance risks, reward fairly and democratise decision making. One way of doing this is to form a non-practising entity which owns the brand, where leadership resides, where intangible assets are owned and licensed to individual entities in the network, cost are incurred for research and development, IT initiatives in each service line to develop new products and processes, manage the network through central policies, provide funding support to entities in need, etc.

In India, initially, this model feels unnatural. After all, Indian firms had been shaped by towering founders whose personal credibility carried client relationships. The Big Four model, by contrast, appeared impersonal. Partners rotate off marquee clients. Personal brands are deliberately submerged beneath a global identity.

This suppression of individual prominence allows for the emergence of continuity. Over time, clients will not leave when partners do. Relationships will outlive personalities. The firm, not the individual, will become the unit of trust. Single hero led firms will give way to numerous leaders with democratisation of ownership, decision making and choosing leaders with fixed terms through and unbiased merit based selection process.

All of this is possible within one network comprising of regulated and non-regulated entities with checks and balances to ensure that the regulated entities continue to comply with regulatory requirements.

3. INDEPENDENCE: THE NON-NEGOTIABLE CORE OF GLOBAL PRACTICE

Independence is the most sensitive regulatory issue in the globalisation of accounting firms. It is also the issue most likely to be misunderstood. Independence is not only a state of mind; it is also a matter of appearance. A firm may believe that its professional judgment is unaffected, but if the surrounding circumstances create a reasonable perception that the firm is financially dependent, commercially conflicted, or reviewing its own work, the independence concern remains.

The IESBA Code of Ethics has become an important global reference point. The 2024 IESBA Handbook includes revisions relating to the definition of public interest entity, including replacing the earlier “listed entity” category with the broader “publicly traded entity” concept for relevant provisions effective for audits of financial statements for periods beginning on or after 15 December 2024. (Ethics Board) The IESBA framework is based on identifying threats to compliance with fundamental principles and applying safeguards where available. However, for public interest entity audits, many non-assurance services are not merely subject to safeguards but are prohibited or tightly restricted.

Different jurisdictions apply independence requirements through different mechanisms. Some rely substantially on professional ethical codes; others combine professional codes with securities law, audit regulator rules, audit committee pre-approval and statutory prohibitions. A global Indian firm cannot rely only on Indian rules when servicing clients with overseas reporting, listing or audit requirements.

| Jurisdiction / Framework |

Main Source of Independence Regulation |

Key Features Relevant to Global Firms |

Practical Implication for Indian Firms |

| India |

Companies Act, 2013; ICAI Code of Ethics; NFRA/ICAI oversight |

Section 144 prohibits specified non-audit services by auditors directly or indirectly to audit clients, holding companies and subsidiaries. |

Indian firms must map services across the audit client group and across entities using the same brand or network. |

| United States |

SEC independence rules; PCAOB standards and inspections |

Audit committees are expected to pre-approve audit and permissible non-audit services; SEC guidance identifies prohibited services such as bookkeeping, financial information systems design and implementation, management functions and advocacy roles. |

If an Indian firm audits or supports audit work for an SEC registrant, US independence standards may become relevant even where Indian rules appear less restrictive. |

| European Union |

Regulation (EU) No. 537/2014 for statutory audits of public-interest entities |

Article 5 prohibits statutory auditors and audit firms auditing PIEs from providing specified non-audit services to the audited entity, its parent and controlled undertakings within the prescribed framework. |

Network-level service mapping is critical, especially where advisory services are provided in one country and audit services in another. |

| United Kingdom |

FRC Ethical Standard for Auditors |

The FRC Ethical Standard applies to audits and other public interest assurance engagements; the 2024 update is effective from 15 December 2024. |

UK-related audit work requires attention to fee caps, non-audit services, long association and public-interest restrictions. |

| Singapore |

ACRA Code and Practice Monitoring Programme |

ACRA regulates public accountants and accounting entities, including registration, ethics and practice monitoring. The PMP assesses whether audits are performed according to prescribed professional standards. |

Singapore-facing work requires readiness for regulator-led practice monitoring and quality-control expectations. |

There are a number of case studies of actions against professional firms by regulators for breach of independence. The lesson is clear: independence is not managed only by engagement partners. It requires firm-wide systems, consultation protocols, technology-enabled tracking, training and accountability.

For Indian firms aspiring to operate globally, independence should be treated as a design principle. Before accepting a client or service, the firm must ask: Who is the audit client? Who are its affiliates? Which network firms serve the group? Are there financial interests, employment relationships, family relationships, fee dependence issues, self-review threats or advocacy threats? Is the service prohibited absolutely, permissible with safeguards, or permissible only after audit committee approval? These questions must be asked before commercial discussions have matured, not after the engagement letter is ready.

Large global networks manage independence by classifying their global client base into attest and non-attest clients. They monitor compliance through continuous monitoring through using technology besides cross border conflict checks and have a rigorous oversight over individual partner and professionals’ independence through compliance tools requiring disclosure of holdings and other interests of themselves and their family members.

4. NETWORKS, ALLIANCES AND THE PROBLEM OF SHARED IDENTITY

Networks and alliances are attractive pathways for Indian firms because they allow access to global referrals, methodologies, training, branding and cross-border execution without immediate merger into a single global partnership. However, networks create their own regulatory complexity. The larger the network, the greater the risk that one-member firm’s services may affect another member firm’s independence.

In audit regulation, the concept of a “network firm” is significant because independence concerns may extend beyond the signing firm. Under international independence standards, non-assurance services provided by a network firm to an audit client or its related entities may affect the independence of the audit firm. The IESBA Handbook specifically addresses communication with those charged with governance before a firm or network firm provides non-assurance services to entities within the corporate structure of a public interest entity audit client.

This is where many mid-sized firms underestimate the challenge. A network may be marketed as “independent member firms,” but from the client’s or regulator’s perspective, common branding, shared methodologies, referral arrangements, common quality standards and global pitches may create expectations of coordinated conduct. The phrase “independent member firm” cannot become a shield against poor coordination. If a network markets itself globally, it must also govern itself globally.

Indian firms joining networks must therefore examine the network agreement carefully. Questions of exclusivity, brand use, referral obligations, quality control, inspection rights, client acceptance procedures, independence databases, confidentiality obligations, dispute resolution and exit consequences are not merely legal drafting points. They determine whether the network is a real institutional platform or only a loose referral club. Globalisation through networks is viable, but only if the firm understands that shared identity brings shared risk.

5. CONFLICTS OF INTEREST: BEYOND INDEPENDENCE

Conflicts of interest are related to independence, but they are not identical. Independence is primarily associated with audit and assurance objectivity. Conflict of interest is broader. It can arise in advisory, tax, valuation, insolvency, transaction support, forensic, litigation support and consulting assignments, even where no audit relationship exists.

For example, a firm advising a buyer on due diligence may previously have advised the seller on tax structuring. A firm assisting a company in a regulatory investigation may also be advising a whistle-blower or a competing bidder in another jurisdiction. A firm providing transfer pricing advice to two companies in the same supply chain may be asked to support positions that are commercially adverse. A firm providing forensic support to a board committee may have earlier designed internal controls that are now under review. In each case, the question is not merely whether the firm can technically perform the work. The question is whether its objectivity, loyalty, confidentiality obligations or professional credibility are compromised.

Sometimes firms claim to have “Chinese Wall” between teams providing services to get around conflict of interest situations. This is a mere fig leaf and firms have to realise that even the legendary Great Wall of China was breached. In today’s highly connected world where physical locations don’t matter and the spread of communication in the digital world and social media are lightning swift “Chinese Wall” is illusory.

A global firm faces a higher conflict risk because client relationships are dispersed across offices, legal entities and practice lines. The tax team in one country may not know that the transaction team in another country is advising an adverse party. A consulting entity may not know that the audit practice has a relationship with the same group. Without a centralised conflict check process, the firm may discover the conflict only after it has received confidential information from both sides.

A practical conflict-check framework for global Indian firms should include the following:

| Conflict Area |

Practical Question |

Required Control |

| Client identity |

Who is the real client: parent, subsidiary, promoter, board committee, lender, investor or management? |

Client and beneficial ownership mapping |

| Adverse party |

Is the firm or any affiliate advising a counterparty or competitor in the same matter? |

Matter-level conflict search |

| Prior work |

Has the firm earlier advised on the structure, valuation, control, tax position or system now being reviewed? |

Prior engagement review |

| Confidential information |

Has the firm received non-public information from another party that may be relevant? |

Information barrier assessment |

| Scope creep |

Can a permitted advisory assignment become advocacy or management decision-making? |

Scope approval and periodic review |

| Network impact |

Does any network firm have a relationship that affects acceptance? |

Network-wide conflict confirmation |

| Resolution |

Can the conflict be cured by disclosure and consent, or is refusal/resignation required? |

Ethics partner approval |

The most important discipline is to define the “matter” correctly. A conflict check limited to client name may fail where the conflict is transaction-specific. Global firms therefore need databases that identify clients, related parties, beneficial owners, engagement types, industry restrictions, independence status, confidentiality restrictions and adverse parties. More importantly, they need a culture where partners accept that a lucrative engagement may have to be declined.

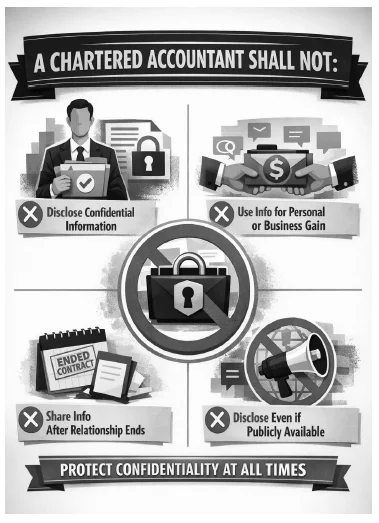

6. CONFIDENTIALITY AND INFORMATION BARRIERS

Confidentiality deserves separate treatment because it is not merely a subset of conflict of interest. Professional accountants receive sensitive information: financial statements before publication, tax positions, merger plans, pricing models, payroll data, board papers, litigation strategies, regulatory exposures, whistle-blower complaints and personal data. In cross-border practice, confidentiality risk increases because information may move across countries, cloud platforms, shared service centres, network firms and subcontractors.

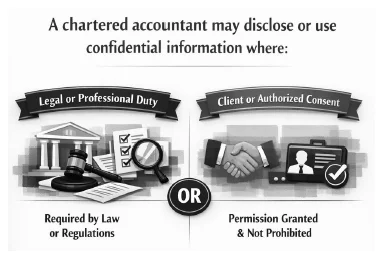

The ethical duty of confidentiality requires firms not to disclose information acquired through professional relationships without proper authority, unless there is a legal or professional duty to disclose. But in a global firm, the practical question is: who within the firm should have access? The answer cannot be “everyone under the same brand.” Access must be need-based.

Information barriers should therefore be formal, not informal. Engagement teams should be ring-fenced where necessary. Data rooms should have role-based access. Internal emails should avoid unnecessary circulation. Shared drives should be controlled. Consultants and external experts should sign confidentiality undertakings. Cross-border transfer of data should be checked against applicable data protection law. Where the firm operates through a network, confidentiality obligations must be contractually imposed across member firms and subcontractors.

The growing use of artificial intelligence and analytics tools adds a further dimension. Firms must ensure that client data is not uploaded into tools in a manner that breaches contractual confidentiality, data protection obligations or regulatory expectations. A global Indian firm should have a clear AI-use policy covering approved tools, client consent, anonymisation, retention, access control and prohibition on training public models using confidential client data.

7. DATA PROTECTION: FROM BACK-OFFICE ISSUE TO BOARD-LEVEL RISK

Data protection is now a core regulatory issue for global accounting firms. Accounting firms process large volumes of personal data relating to employees, customers, vendors, investors and directors. They also handle sensitive financial and commercial data. When services are delivered across borders, personal data may be transferred between jurisdictions with different privacy standards.

Indian firms must consider India’s Digital Personal Data Protection Act, 2023, but global work may also trigger the EU GDPR, UK GDPR, Singapore PDPA, UAE data protection laws or sectoral confidentiality rules depending on the client, data subject, place of processing and contractual terms. A single global engagement may involve data collected in Europe, processed in India, reviewed by a team in Singapore and stored on servers of a cloud provider located elsewhere. The regulatory analysis cannot be left to the IT department alone.

From a governance perspective, every cross-border engagement should answer certain basic questions: What data will be accessed? Does it include personal data? Who is the controller or processor? Is there a data processing agreement? Is cross-border transfer permitted? What security standards apply? What is the retention period? What is the incident reporting protocol? Are subcontractors involved? Has the client consented to offshore processing?

Data protection also intersects with professional secrecy. A firm may be contractually permitted to process data but ethically required to restrict access. Conversely, a regulatory demand in one jurisdiction may conflict with confidentiality expectations in another. Global firms must therefore establish escalation mechanisms for regulatory notices, data breach incidents and client information requests.

8. AUDIT OVERSIGHT, INSPECTION AND PEER REVIEW

Global accounting practices operate in a world where audit quality is no longer left only to self-regulation. Public oversight bodies, audit regulators, peer review mechanisms and inspection programmes increasingly shape the credibility of firms.

Internationally, audit oversight is perceived to be more intrusive than in India though NFRA in its recent inspections and investigations has changed this perception. The PCAOB oversees audits of public companies and SEC-registered brokers and dealers, and its responsibilities include registration, inspection, standard-setting and enforcement. Singapore’s ACRA Practice Monitoring Programme assesses whether audits are performed in accordance with prescribed professional standards and other requirements. These regimes demonstrate that global audit practice requires readiness for external inspection, not merely internal confidence.

Indian firms that aspire to global work must therefore invest in quality management systems, methodology, engagement documentation, consultation processes, EQCR/EQR mechanisms, independence tracking, training records and archival discipline. The firm’s quality file must be capable of being reviewed by an external inspector who was not part of the engagement and may not share the firm’s informal understanding of the client.

Indian firms must adopt quality practices which compare with the best in the world. Quality has to be consistent across clients and geographies and not different for listed companies and private limited companies. Global practices must be embraced including acting swiftly and firmly on non-compliances.

9. DISCIPLINARY JURISDICTION AND CROSS-BORDER ACCOUNTABILITY

Globalisation complicates disciplinary jurisdiction. A partner may be registered in India, the client may be incorporated in Singapore, the parent may be listed in the United States, the work papers may be stored in India, and a network firm may have contributed specialist input from the United Kingdom. If something goes wrong, which regulator has jurisdiction?

The answer may be: more than one. Professional bodies may discipline their members. Audit regulators may sanction registered firms. Securities regulators may act where listed-company filings are affected. Courts may entertain civil claims. Data protection authorities may investigate breaches. Insolvency, anti-money laundering, sanctions and anti-corruption regulators may also become relevant depending on the assignment.

This creates a major governance issue for Indian firms. Engagement letters and network agreements must address governing law, liability, confidentiality, cooperation with regulators, ownership of work papers, document retention, subcontracting and responsibility for specialist work. However, contractual provisions cannot override statutory jurisdiction. A firm cannot contract out of disciplinary obligations.

For global practice, the safest approach is to assume that work may be reviewed by regulators beyond India if it feeds into an overseas audit, listing, transaction, tax filing, investigation or assurance report. Firms must therefore avoid the attitude that “the signing happens elsewhere, so our risk is limited.” Component work, offshore support and specialist memoranda can all become part of a regulatory record.

10. MULTI-DISCIPLINARY PRACTICE: OPPORTUNITY WITH ETHICAL BOUNDARIES

Multi-disciplinary practice is a natural response to modern client needs. Clients do not experience problems in professional silos. A cross-border acquisition may require financial due diligence, tax structuring, regulatory review, valuation, accounting advice, integration support, technology assessment, ESG review and internal control design. A firm that can bring multiple disciplines together has a commercial advantage.

The key regulatory question in MDP is control of professional judgment. Can non-audit professionals influence audit decisions? Are revenue targets creating pressure on assurance teams? Are consulting partners rewarded for selling services to audit clients? Is confidential audit information being used for advisory opportunities? Are clients being offered bundled services that impair independence? These are not theoretical issues; they are structural risks.

A well-designed MDP must therefore have ring-fenced audit governance, independent ethics oversight, service-line restrictions, clear profit-sharing rules, conflict checks, independence systems and disciplinary accountability. The firm must be able to demonstrate that multi-disciplinary capability enhances service quality without diluting professional independence.

11. EXTERNAL CAPITAL

The interest of private equity and other investors in accounting firms has increased globally, driven by the need for technology investment, succession planning, consolidation, growth capital and professionalisation of management. Accountancy Europe has noted that private equity and third-party ownership are reshaping the European accountancy and audit sector and has highlighted both opportunities and risks relating to quality, independence and governance. (Accountancy Europe)

For Indian firms, external capital raises difficult questions. Audit is a public-interest function. If investors seek short-term returns, cost rationalisation or aggressive cross-selling, there may be pressure on audit quality and independence. On the other hand, without capital, Indian firms may struggle to invest in technology, training, global infrastructure, cyber security, quality systems and international expansion. The policy issue is not whether capital is good or bad. The issue is what type of capital, in what entity, with what governance rights, and with what restrictions.

One possible approach is to distinguish between the regulated audit practice and non-regulated service platforms. External investment may be more feasible in technology, consulting, outsourcing, analytics or training entities, subject to safeguards that prevent interference with audit judgment, misuse of brand and independence violations. If external capital is ever permitted in regulated audit entities, it would require stringent restrictions on voting rights, profit rights, governance influence, exit arrangements, confidentiality, independence and regulator access.

This debate should not be postponed. Global competitors are already investing heavily in technology and multidisciplinary capability. Indian firms cannot become global institutions solely through partner capital if the scale of investment required is far beyond traditional practice economics. But capital must serve the profession; the profession cannot become captive to capital.

There are many who argue against private capital in regulated firms. In my view if in the medical profession doctors can continue to save lives and yet be accountable despite the ownership of their institutions by non-doctors there is not reason why professional firms cannot have private capital. The day is not far off when professional firms would be also listed in stock exchanges!

12. RECOGNITION, MOBILITY AND QUALIFICATION BARRIERS

Professional mobility is another critical dimension of globalisation. A chartered accountant qualified in India may be highly competent, but the right to sign audit reports, appear before regulators, undertake insolvency work or provide reserved services in another jurisdiction depends on local law. Mutual recognition arrangements, qualification pathways, local licensing and residency requirements can determine how far an Indian firm can globalise through its own professionals.

For Indian firms, mobility should be viewed at three levels. The first is people mobility: the ability of Indian professionals to work abroad, obtain local qualifications where needed, and participate in global engagements. The second is firm mobility: the ability of Indian firms to register, affiliate, merge or practise in foreign jurisdictions. The third is service mobility: the ability to provide cross-border services remotely without violating licensing rules in the destination jurisdiction.

Technology may make cross-border delivery easier, but it does not eliminate licensing restrictions. A team sitting in India may support a foreign audit, but the signing rights, review obligations and regulatory responsibility may remain with a locally registered auditor. Similarly, tax advice may cross into unauthorised practice of law in some jurisdictions if not structured properly. Global firms therefore need jurisdiction-wise service maps: what can be delivered from India, what requires local registration, what requires collaboration, and what cannot be done.

13. ETHICAL CONSISTENCY ACROSS JURISDICTIONS

A global Indian firm cannot operate with variable ethics—strict in one country, flexible in another. Regulatory requirements may differ, but the firm’s ethical floor must be consistent. Where local law is less stringent, the firm should still follow its internal global standard. Where local law is more stringent, the firm must comply with the higher standard.

Ethical consistency requires written policies, but it also requires leadership behaviour. Partners must see that independence breaches, confidentiality lapses, poor documentation and aggressive client acceptance are taken seriously. Staff must be trained to escalate concerns. Ethics partners must have authority. Commercial success must not become the only measure of performance.

The reputation of a global accounting firm is cumulative. A failure in one office can affect credibility elsewhere. This is especially true in the age of public enforcement orders, inspection reports, social media and cross-border regulatory cooperation. Indian firms aspiring to global stature must therefore build reputational resilience by investing in ethics before scale, not after scale.

14. CONCLUSION: REGULATION AS THE ARCHITECTURE OF TRUST

The globalisation of Indian accounting firms is both necessary and possible. Indian businesses are global, Indian professionals are capable, and Indian firms have the opportunity to build institutions that combine technical depth, cost competitiveness, cultural adaptability and entrepreneurial energy. But globalisation cannot be built on ambition alone.

The successful global Indian accounting firm will not be the one that merely has the most offices or the widest network. It will be the firm that understands regulated and non-regulated services clearly, manages independence before conflicts arise, separates confidentiality from convenience, treats data as a fiduciary responsibility, welcomes peer review and external inspection, builds systems for multi-jurisdictional compliance, and balances capital with professional control.

Policy support will be useful—particularly in areas such as regulatory harmonisation, recognition of qualifications, facilitation of firm aggregation, and clarity on permissible structures. But the primary responsibility will remain with firms themselves. They must build governance before growth, quality before branding, and trust before scale.

If Indian accounting firms are to move from domestic practices to global institutions, they must recognise a simple truth: regulation is not the enemy of globalisation. Properly understood, it is the architecture that makes global trust possible.

The decisive difference between the past and the present is this: hero partners are no longer enough. Cross-border reporting, ESG assurance, forensic analytics, and technology-enabled audit require systems, platforms, and capital investment in methodology and risk governance. These are baseline expectations.

In earlier decades, caution preserved stability. Today, excessive caution may lead to irrelevance.

The emergence of a Fifth Firm would not be to fight the Big Four. It would be a response to conditions that now make institutional scale feasible within India.

History reminds us that windows do not remain open indefinitely. Competitors respond. Markets consolidate. So, the question is no longer whether India has the conditions for scale. It is whether its professional institutions recognise that the ground beneath them has shifted.