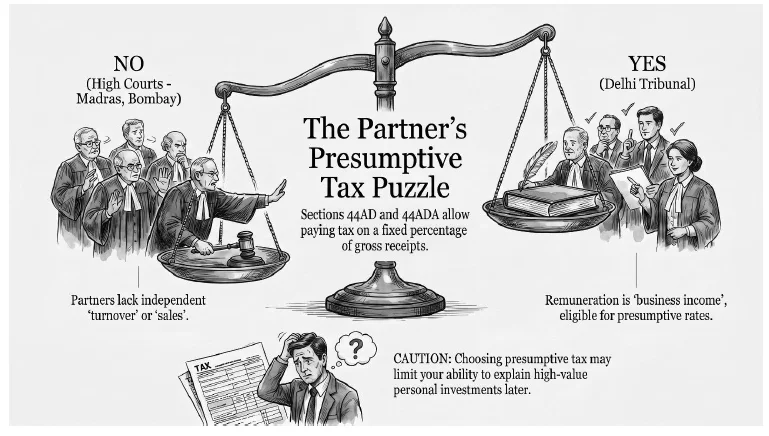

Sections 44AD and 44ADA provide presumptive taxation of business or professional income. A Controversy exists as to whether partner remuneration and interest constitute “gross receipts” for the purpose of these schemes. The Madras and Bombay High Courts have held that these receipts are distributions of firm profits rather than independent turnover, thereby making partners ineligible. Conversely, the Delhi ITAT allowed a professional partner to avail the benefit of section 44ADA, holding that there is no legal requirement for independent activity. While the restrictive view currently carries judicial weight, the Supreme Court must ultimately resolve this conflict.

ISSUE FOR CONSIDERATION

Section 44AD and 44ADA deal with the presumptive scheme of taxation for computing the profits and gains from business or profession respectively, subject to fulfillment of the prescribed conditions. Quite often, the issue arises as to whether these provisions, dealing with computation of profits and gains on a presumptive basis, can be applied in respect of the interest and remuneration received by a partner from a partnership firm.

The Chennai bench of the tribunal had earlier taken a view that the provisions of section 44AD are not applicable for computing the income arising from remuneration received by the partner from a partnership firm. In contrast, the Delhi bench of the tribunal recently held that an individual assessee, who was a partner in a firm of chartered accountants, was entitled to compute his income arising from the remuneration received from the said firm on a presumptive basis under section 44ADA.

A. ANANDKUMAR’S CASE

The issue first came up for consideration before the Chennai bench of the tribunal in the case of A. Anandkumar v. ACIT (ITA No. 573/Chny/2018).

In this case, for assessment year 2012-13, the assessee, who was a partner in a few firms, had received remuneration and interest from partnership firms aggregating to Rs.58,53,000. The income of the firms were computed under the regular provisions of the Act without applying the presumptive taxation provisions. While filing return for the relevant assessment year, the assessee had applied the presumptive rate of 8% under section 44AD of the Act and returned Rs.4,68,240 as income from the such remuneration and interest. The Assessing Officer was of the opinion that section 44AD could be availed only by an eligible assessee engaged in an eligible business. According to him, the assessee was not carrying on any independent business but was merely a partner in the firms. Further, according to the Assessing Officer, the assessee had no turnover, and the receipts on account of remuneration and interest from the firms could not be construed as “gross receipts” mentioned under section 44AD of the Act. He, therefore, denied the benefit of section 44AD and brought to tax the entire amount of remuneration and interest received from the firms. The appeal filed by the assessee before the CIT (A) was also dismissed.

Before the tribunal, the assessee submitted that section 28(v) of the Act clearly specified that interest, salary, bonus, commission or remuneration received by, or due to, a partner of a firm from such firm had to be assessed under the head “Profits & gains of business or profession”. Section 44AD enabled an assessee having turnover or gross receipts from an eligible business to apply the presumptive rate of 8% in computing his income from business or profession. By virtue of the Explanation to Section 44AD, “eligible business” included any business other than the business of plying, hiring or leasing goods carriages referred to therein. The assessee contended that since remuneration and interest were considered as profits and gains of business or profession by virtue of section 28(v) of the Act, such receipts became receipts from an eligible business. Since the gross receipts of the assessee from interest and remuneration was below ₹1 crore for the relevant assessment year, the assessee argued that he was eligible to apply the presumptive rate of 8% on such receipts for estimating the income. The assessee placed reliance on the judgement of Hon’ble Apex Court in Munjal Sales Corporation v. CIT (289 ITR 298) (SC) and an order of Kolkata bench of the tribunal in Sagar Dutta v. DCIT in ITA No.692/Kol/2012 dated 03.05.2013.

After examining the scheme of taxation applicable to partnership firm and partners, the Tribunal held that if remuneration and interest paid to partners had not been charged in the accounts of the firm, the taxable profits of the firm would have been higher, resulting in a higher tax liability for the firm. The payments of interest and remuneration, therefore, had to be construed indirectly as a form of distribution of profits of a firm, on which the firm would otherwise have been taxed. Though the legislature, in its wisdom, chose to tax such remuneration and interest as profits and gains from business or profession in the hands of the partners, that by itself, would not convert such remuneration and interest into gross receipts or turnover arising from the business of being partners in firms. In other words, such receipts in the hands of a partner could not be construed as gross receipts or turnover of a business independently carried on by the partner.

By referring to the Explanatory Notes to the provisions of the Finance (No. 2) Act, 2009 vide Circular No. 5/2010 dated 3-6-2010, the Tribunal observed that the intention behind the provision was to help small businesses to comply with the taxation provisions, and it was never intended to treat a partner’s remuneration or interest as business turnover. The decisions relied upon by the assessee were held to be not applicable on the ground that they did not relate to the provisions of section 44AD. On this basis, the tribunal dismissed the appeal of the assessee and affirmed the view which was taken by the lower authorities.

RANU GUPTA’S CASE

The issue recently came up for consideration before the Delhi bench of the tribunal in Ranu Gupta v. ACIT (ITA No. 2224/Del/2025).

In this case, for the assessment year 2018-19, the assessee had received the remuneration of Rs.27,00,000 as a partner of a firm of Chartered Accountants. The assessee had offered 50% of the same as his income under the provisions of section 44ADA of the Act. Before the Assessing Officer, the assessee contended that he was eligible to compute the income under section 44ADA since he had fulfilled all the conditions provided prescribed therein. The remuneration was received by him in his capacity as a Chartered Accountant holding a certificate of practice issued by the Institute of Chartered Accountants of India. The assessee relied upon the decisions in Sagar Dutta (ITA No. 692/Kol/2012), the decision of the Hon’ble Supreme Court in Ramnik Lal Kothari (1969) 74 ITR 57 (SC,) and the decision of the Hon’ble ITAT Delhi in Aman Tandon (ITA No. 3469/Del/2015).

The Assessing Officer did not accept the claim of the assessee stating that the remuneration was received by him as a working partner of the firm and not as an individual independently carrying on the profession specified u/s. 44AA(1). The Assessing Officer also relied upon the Circular No. 3 of 2017 dated 20-10-2017, wherein it was stated that section 44ADA was introduced to reduce compliance burden of small taxpayers earning professional and to facilitate ease of doing business. The Assessing Officer further noted that the assessee himself had declared the entire remuneration received from the firm as business income in AY 2016-17 and 2017-18. Distinguishing the decisions relied upon by the assessee, the Assessing Officer placed reliance on the decision of the Chennai bench of the tribunal in A. Anandkumar (supra). Finally, the Assessing Officer held that a partner’s remuneration from the firm could not be treated as gross receipts for the purposes of section 44ADA in view of section 28(v) and 40(b) of the Act.

The CIT (A) concurred with the view of the Assessing Officer and held that the remuneration was not received for carrying on or practicing the profession, but was received in the capacity of a working partner of the firm. The remuneration received by the partner was distinct and separate from income from profession. The CIT (A) relied upon the decision in A. Anandkumar (supra), which had been affirmed by the Hon’ble Madras High Court. In so far as reliance was placed by the assessee on the decision in Ramnik Lal Kothari (1969) 74 ITR 57 (SC), the CIT (A) observed that the Assessing Officer had not allowed any expenditure against the remuneration, since no details were furnished by the assessee in spite of the specific show cause issued in that regard.

Before the tribunal, nobody appeared on behalf of the assessee. The revenue contended that the assessee had neither claimed any expenditure, as noted by the Assessing Officer during the assessment proceedings, nor was he entitled to claim benefit of the presumptive scheme under section 44ADA in respect of the remuneration received from the partnership firm.

The tribunal held that there was no merit in the revenue’s twin arguments, as there was no such pre-condition in section 44ADA either to claim the corresponding expenditure (in light of sub-section (2) thereto) nor was he supposed to carry out his independent professional activities otherwise than as a partner in any establishment. On this basis, the tribunal invoked rule of strict interpretation by relying upon the decision in the case of Commissioner of Income-tax v. Dilip Kumar (2018) 9 SSC 1 (SC) to reject the Revenue’s foregoing arguments and directed the Assessing Officer to assessee the income of the assessee under section 44ADA of the Act.

OBSERVATIONS

Section 44AD and 44ADA provide for determination of profits and gains arising from the business or profession carried on by the assessee on presumptive basis, subject to fulfillment of certain conditions. Under these provisions, the income of an eligible assessee is computed on a presumptive basis, and a specified percentage of the turnover or the gross receipts is deemed to be the profits and gains of the business or profession carried on by the assessee.

Primarily, two conditions are required to be satisfied for the application sections 44AD or 44ADA. First, the assessee should be engaged in business or profession i.e. the business or profession in respect of which the income is sought to be computed on a presumptive basis should belong to the assessee. Secondly, there must be the turnover or gross receipts from such business or profession on basis of which the income can be computed at the prescribed percentage.

In so far as the first condition is concerned, it is the partnership firm that carries on the business or profession, albeit through its partners. It is true that the business carried on by the partnership firm has been regarded as nothing but the business carried on by the partners collectively. In this regard, the reference can be made to the decision of Gujarat High Court in the case of CIT v. Rasiklal Balabhai (1979) 119 ITR 303, wherein it was held that the assessee must be considered to be carrying on business when such business is that of a partnership firm since a partnership firm has no legal entity and is merely a compendious expression for all the partners.

In the context of section 44AD or 44ADA, the requirement is to compute the income on a presumptive basis at the specified percentage of the turnover or gross receipts of the concerned business or profession. A difficulty may arise, in the context of the Income Tax Act and particularly under the presumptive taxation, in contending that the firm and the partner are carrying on the same business and that the turnover of the business or profession is the same for both assessees, it may then become difficult to contend that the same business has resulted in different amount of turnover or gross receipts in the hands of the partnership firm and in the hands of the partners.

The view taken by the Chennai bench of the tribunal in the case of A. Anandkumar (supra) has been affirmed by the Madras High Court [Anandkumar vs. Assistant Commissioner of Income Tax, Circle-2, Salem [2020] 122 taxmann.com 252 (Madras)]. The Madras High Court held that, in order to avail the benefits of section 44AD, the assessee must establish that he is an eligible assessee engaged in an eligible business and that such business has total turnover or a gross receipt. Admittedly, the assessee, being a partner was not carrying on any business resulting in such turnover. Therefore, the remuneration and interest received by the assessee from the partnership firm could not be termed as the turnover of the assessee, who was merely a partner in the firm. Similarly, a partner could not contend that such receipts constituted his gross receipts. The High Court referred to the definition of the term ‘turnover’ as provided in the statement issued by the ICAI on the Companies (Auditors report) Order 2003, wherein it was defined to mean the aggregate amount for which sales are effected or services rendered by an enterprise. Admittedly, the assessee, being a partner in the firm, had neither effected any sales nor rendered any services independently, but had merely received remuneration and interest from the partnership firms, which amounts had already been debited in the profit and loss account of the firms. Therefore, the High Court agreed with the revenue’s contention that remuneration and interest could not be treated as turnover or gross receipts.

Further, the High Court observed that the payment of interest and remuneration had to be construed indirectly as a type of distribution of profits of a firm, on which the firm would otherwise have been taxed. Therefore, though the legislature, in its wisdom, chose to treat such remuneration and interest as part of profits and gains from business or profession, that could never translate into gross receipts or turnover arising from the business of being partner in a firm.

The Delhi bench of the tribunal, however, did not follow the decision of the Madras High Court in the case of A. Anandkumar (supra) although the same had been relied upon by the CIT (A).

In Perizad Zorabian Irani vs. Principal Commissioner of Income-tax [2022] 139 taxmann.com 164 (Bombay), the Bombay High Court also agreed with the view expressed by the Hon’ble Madras High Court in the case of A. Anandkumar v. Asstt. CIT (supra) and held that a partner’s remuneration cannot be treated as gross receipts from profession.

There is one more aspect which is equally important for deciding the issue under consideration. The amount treated as deemed profits under section 44AD or 44ADA is either the sum computed in the manner prescribed therein or a higher sum claimed to have been earned by the assessee. Indirectly, this implies that, for the purpose of explaining investments in assets, or otherwise, the assessee may not be able to claim that he had earned the income higher than the amount of profits computed on a deemed basis under section 44AD or 44ADA, if he opts for these provisions. In other words, for purpose such as explaining the source of investment made out of the income etc., the assessee may not be able to contend that the actual income from business or profession was higher than the deemed profits offered to tax on a presumptive basis. Therefore, one should be cautious of this limitation while taking a view that income in respect of interest or remuneration received from a partnership firm can be computed on a presumptive basis.

In our respectful submission, the view taken by the Chennai bench of the tribunal appears to be the correct view, particularly since the same has also been upheld by the High Courts of Madras and Bombay. However, the contrary view is also possible, and therefore one will ultimately have to await the decision of the Supreme Court on the issue.