Legal “deeming fictions” are assumptions treated as true by law, regardless of reality. Under the Income Tax Act, these provisions have evolved from narrow anti-abuse tools into central components governing residency, deemed dividends, and income characterization. For example, Section 50 deems gains on depreciable assets as short-term for computation purposes, though it does not alter the asset’s inherent nature. Significant contention surrounds Section 56(2)(x), which taxes property receipts for inadequate consideration, leading to debates over its application to bonus and rights issues. Furthermore, the Finance Act 2024 shifted buyback taxation from companies to shareholders, treating proceeds as deemed dividends. Complexities also arise when domestic fictions, such as indirect transfer rules, conflict with Double Taxation Avoidance Agreements (DTAAs), which generally prevail. While essential for plugging loopholes, the expansive use of these fictions increasingly triggers interpretational challenges and litigation.

INTRODUCTION

Fiction is something invented by the imagination, i.e., ‘make believe’. The term ‘legal fiction’ can in the simplest of forms be explained as an assumption believed to be true and present in the eyes of the law. Once a particular assumption by way of a legal fiction is made, it is irrelevant as to whether the same is line with the actual truth or not.1

A famous American author once remarked that “The difference between fiction and reality? Fiction has to make sense”. But do the deeming fictions under the Income Tax Act, 1961 (‘the Income Tax Act’) really make sense?

The immediate mention of the term “deeming fiction” springs to mind provisions such as section 56(2)(x), explanations 5 to 7 of Section 9(1)(i) [‘Indirect Transfer’], or the much-beleaguered section 56(2)(viib)2. Below are some examples such as residency, characterization of losses, timing of taxation, etc. illustrating the various types of deeming fictions embedded within the Income Tax Act:

- Deemed Resident– Sub-section 1A of section 6 provides that an individual who is a citizen of India, has total income (other than income from foreign sources) exceeding INR fifteen lakh rupees during and is not liable to tax in any other country on account of certain connected factors shall be deemed to be resident in India.

- Carry forward and set-off of losses and unabsorbed depreciation- Section 72A provides that upon satisfaction of certain conditions, in case of amalgamation3, the accumulated loss and the unabsorbed depreciation of the amalgamating company shall be deemed to be the loss and unabsorbed depreciation of the amalgamated company.4

- Timing of taxation– Section 45(5A) of the Income Tax Act provides for determining the timing of taxation in case of a joint development agreement entered into by an individual/HUF (deemed to be taxable in the year in which the certificate of completion is issued).

- Full value of consideration- Deeming fictions aimed at curbing tax avoidance and determining full value of consideration in case of certain transactions include section 50C (Transfer of land/building or both being capital asset), section 50CA (transfer of shares other than quoted share)

- Deemed Dividend- Whereby the statute aims to expand the meaning of the word ‘dividend’ to curb mechanisms used by taxpayers to repatriate cash or assets to their shareholders such as by way of loans or advances (applicable for closely held companies), capital reduction or distribution of assets pursuant to liquidation.

- Scope of total income- Clubbing provisions under section 64 of the Income Tax Act seek to expand the scope of total income of an individual to tax income arising to another individual (such as a minor child) in the hands of that particular individual.

- Computation of tax in case of specific transactions/ instruments- Sections such as section 50 (computation of capital gains in case of sale of a depreciable asset), section 50B (computation of capital gains in case of slump sale), section 50AA (computation of capital gains in case of Market Linked Debenture) are just some examples.

1 CIT vs. Swaroop Krishan [1985] 21 Taxman 404/153 ITR 1 (Pun & Har HC) 2 Section 56(2)(viib) was introduced by the Finance Act, 2012, to tax the share premium received by closely held companies when issued above fair market value. It was sunset by the Finance Act, 2024, and has been rendered inapplicable from 1 April 2025 (Assessment Year 2025–26 onward) 3 This section is also applicable on demerger and provides that in case of demerger, where the loss or unabsorbed depreciation is directly relatable to the undertakings transferred same shall be allowed to be carried forward and set off in the hands of the resulting company. In case of loss and UAD not directly relatable, same is apportioned between the demerged company and the resulting in the ratio of assets being transferred as part of the demerger 4 Finance Act 2025 had introduced an amendment seeking to confine the carry forward of losses to a total of eight years from the year in which such losses arose, rather than eight years from the previous year when such merger was undertaken

The above examples illustrate how the role of deeming fictions has evolved and now serves distinct purposes under the Income Tax Act which may range from taxing a particular instrument, item or transaction, prescribe methods of computation, or restrict/ allow carry-forward of losses. Let us examine how courts have interpreted some specific deeming fictions over time and some of the challenges posed in interpreting the same.

FROM FICTION TO FUNCTION: THE EVOLVING ROLE OF DEEMING PROVISIONS IN TAX LAW

- Decoding the section 50 conundrum:

Section 50 of the Act creates a deeming fiction that capital asset on which depreciation is allowed and it forms part of block of asset, then irrespective of definition in section 2(42A), gain from such asset would be deemed as gain from transfer of short term capital asset.

Further, section 50 prescribes a method of computation adjusting provisions of section 48 and 49. However, the provisions of section 50 do not expressly ascribe a rate of tax to the gains computed and also do not restrict the exercise of section 112.

The provisions of section 50 are relevant to be analyzed in case of itemized sale of assets on which depreciation has been allowed under the Income Tax Act. The operation of the provisions of section 50 of the Income Tax Act had rendered share sale or slump sales more attractive for tax efficiency considering possible elevated tax exposure (since section 50 would deem any gain on transfer of depreciable asset as gain from transfer of short term capital asset)

The above problem came up for consideration most recently before the special bench of the Mumbai Tribunal5 wherein the crux of the question revolved around rate of tax to be ascribed to sale of a capital asset of the nature referred to in section 50.

The Tribunal while adjudicating the matter in favour of the assessee relied on the decision of Ace Builders6 where the scope of the deeming fiction under section was interpreted by the Hon’ble Court in context of availability of benefit under section 54E of the Income Tax Act and it was observed that the deemed fiction created in sub-section (1) & (2) of section 50 is restricted only to the mode of computation of capital gains contained in Section 48 and 49 of the Income Tax Act. The judgement of the Tribunal was a majority decision and the Hon’ble Accounting Member had rendered a dissenting view holding that concessional rate under section 112 of the Income Tax Act shall not be available to the assessee inter alia for the reason that the above view would render provisions of section 50 redundant.

Conclusion:

The intent of section 50 of the Income Tax Act is to compute the capital gains in case of a depreciable asset by way of a deeming fiction overriding the provisions of section 48 and section 49. However, this insertion in section 50 does not alter the inherent nature of an asset.

The period of holding determines the inherent nature of a capital asset, i.e., whether long-term or short-term, which consequentially determines the applicable rate of tax. In my view, the above decision is correct in law and cements the settled principle that deeming fictions may be restricted to the section(s) for which they were originally intended for7.

5 SKF India Limited vs. Dy. Commissioner of Income Tax: [2025] 121 ITR(T) 307 (Mumbai - Trib.) (SB) 6 CIT vs. Ace Builders (P.) Ltd: [2006] 281 ITR 210 (Bom.) 7 CIT vs. Mother India Refrigeration Industries (P.) Ltd: [1985] 155 ITR 711 (SC); Imagic Creative Pvt. Ltd. vs. Commissioner of Commercial Taxes: Appeal (Civil) 252 of 2008 (SC)

- The Gift That Isn’t- Understanding section 56(2)(x) on issue of shares:

Section 56(2)(x) was introduced vide Finance Act, 2017 expanding the scope of the erstwhile anti-abuse provisions. In simple terms, section 56(2)(x) seeks to tax receipt of property (including shares) for nil or inadequate consideration.

The language of the section begins with “where any person receives” and thereafter bifurcates into specific cases of receipt of sum of money/immoveable property and any other property (including shares and securities). Thus, from a bare reading of the provisions, for a transaction to fall within ambit of section 56(2)(x) of the Income Tax Act, it should constitute a ‘receipt’.

Thus, whether fresh issue of shares constitute a ‘receipt’ and accordingly can be said to be within ambit of section 56(2)(x) of the Income Tax Act. In case of fresh issue of shares, there cannot be any ‘receipt’ since the property in question being shares are brought into existence for the first time on issue. Support for the above can be firstly drawn from the explanatory notes to finance bill at the time of including transactions involving shares within ambit of section 56(2)(viic), which sought to curb “the practice of transferring unlisted shares at prices much below their fair market value”.

Thus, it can be said that there is a difference between issue of a share to a subscriber and the purchase of a share from an existing shareholder. The first case is that of creation whereas the second case is that of transfer.8

On the contrary, it has also been argued that the exact term used in section 56(2)(vii)(c) is ‘receive’ which cannot be restricted to ‘transfer’ or ‘receipt by way of transfer’ alone.9 Accordingly, limiting the scope of ‘receipt’ to transfer would tantamount to reading down the provision.10

8 Khoday Distilleries Ltd vs. CIT: [2008] 307 ITR 312 (SC) 9 Jigar Jashwantlal Shah vs. ACIT: [2022] 226 TTJ 161 (Ahd Trib) (Confirmed in PCIT vs. Jigar Jaswantlal Shah: [2024] 460 ITR 628) 10 Sudhir Menon HUF vs. ACIT: [2014] 148 ITD 260 (Mum Trib)

Given that fresh issue can be undertaken by many modes, i.e., rights issue or bonus issue or preferential issue, thus, it is at this stage critical to diverge and analyze applicability of section 56(2)(x) on some of the different modes of issue of shares, viz, rights issue and bonus issue. The same has been analyzed under:

| S.No | Particulars | Remarks |

| 1 | Applicability on section 56(2)(x) on bonus issue |

A strict interpretation of law may give the impression that section 56(2)(x) is attracted in case of bonus issue considering no consideration is paid for receipt of shares. In my opinion, the above view is incorrect and would lead to absurd consequences as bonus issue does not lead to any accretion of property held by the shareholder. In substance, when a shareholder gets a bonus shares, the value of the original share held by him goes down and the market value as well as intrinsic value of two (original and bonus) shares put together will be the same. Thus, any profit derived by the assessee on account of receipt of bonus shares is adjusted by depreciation in the value of equity shares held by him.11 Recently however, the Hon’ble Apex Court12 had admitted a SLP against the decision of the Hon’ble Madras HC on the above issue where it was held that section 56(2)(x) of the Income Tax Act would not apply in case of bonus issue. |

| 2 | Section 56(2)(x) of the Income Tax Act in case of Rights Issue |

Where there is a proportionate allotment to existing shareholders, there is only apportionment of existing value of the company over larger number of shares and consequently there is no scope for any property being received by the shareholder. However, the above view was distinguished by adoption of a stricter interpretation that rights issues are nowhere excluded from the express provisions of section 56(2)(vii)(c). The CBDT has also supported applicability of section 56(2)(vii)(c) on fresh issue of shares [Refer to Circular No. 3/2019 by withdrawing its earlier Circular 10/2018] |

11 PCIT vs. Dr Ranjan Pai : 431 ITR 250 (Ktk High Court) 12 SLP admitted in CIT vs. M/s Tangi Facility Pvt Ltd: SLP (C) Diary No. 57035/2025 against Madras HC order in the case of CIT vs. M/s Tangi Facility Pvt Ltd: ITA No. 259/2024

THE CASE OF SUDHIR MENON- A DISPROPORTIONATE TAX?

As can be seen above, in case of rights issue of shares leading to a proportionate shareholding, it can be argued that provisions of section 56(2)(x) of the Income Tax Act may not be attracted. But what happens in case of fresh issue of shares leading to a lopsided shareholding, i.e., the proportionate ownership among shareholders becomes uneven after the rights issue. This scenario can be better explained with the help of the below scenario of Co A which is proposing to undertake a rights issue:

| S. No | Name of shareholder | Existing shares held | Existing shares held (%) | Fresh rights allotment | Whether subscribed or not | Shares held post rights issue | Fresh shares held (%) |

| 1 | Mr. AA | 1,000 | 25% | 1,000 | No- renounced in favor of Mr.AD | 1,000 | 12.50% |

| 2 | Mr. AB | 1,000 | 25% | 1,000 | 1,000 | 12.50% | |

| 3 | Mr. AC | 1,000 | 25% | 1,000 | 1,000 | 12.50% | |

| 4 | Mr. AD | 1,000 | 25% | 1,000 | Yes | 5,000 | 62.50% |

| Total | 4,000 | 100% | 100% | 8,000 | 100% | ||

As seen above, Mr. AA, AB,AC and AD are four shareholders of Co A each holding 25% each. Co A decides to undertake a rights issue, and each shareholder is offered shares commensurate to its shareholding.

However, Mr. AA, AB and AC decide to renounce the right to subscribe to shares in favour of Mr.AD and accordingly Mr.AD subscribes to his rights shares as well as to the shares pursuant to renouncement of rights by all the other shareholders. As a result, the shareholding pre and post rights issue becomes skewed, i.e., Mr. AD’s shareholding increases from 25% to 62.50% granting him control of Co A pursuant to such allotment.

Considering that there is a shift in value in the hands of the shareholders because of the above issue, it can be said that as a result of the above allotment of shares, there is a disproportionate value shift in the hands of Mr. AD.

Thus, it can be said that if there is no disproportionate allotment, i.e., shares are allotted pro rata to the shareholders, based on their existing holdings, there is no scope for any property being received by them on the said allotment of shares.13

13 Sudhir Menon HUF vs. ACIT: [2014] 148 ITD 260 (Mum Trib)

Further, in an alternative scenario, where shares of Co A are not subscribed by Mr.AA, AB and AC but are also not renounced in favor of Mr.AD, which would still lead to increase in shareholding of Mr.AD from 25% to 40%, it maybe argued that due to non-renunciation of the rights to subscribe in favor of Mr.AD, section 56(2)(x) may not be applicable in the present case.

Conclusion:

While it may be a fresh issue of shares, the controversy around applicability of section 56(2)(x) remains age old. It can be safely said that even fresh issue is not truly out of the ambit of section 56(2)(x) of the Income Tax Act. In my view, the principle of taxing a value shift or a disproportionate allotment is not something in line with the original intent of the provisions of section 56(2)(x) of the Income Tax Act and is advocating of a ‘see-through’ approach.

While the Tribunal in the judgement of Sudhir Menon (above) has made findings to the contrary, in my view, the principles given in the above decision have lent a more investigative lens at of looking at transactions outreaching the existing provisions which brings into question even bona-fide transactions under the lens of the tax authorities.

INTERPLAY OF DEEMING FICTIONS WITH DOUBLE TAXATION AVOIDANCE AGREEMENTS (‘DTAA’):

In the foregoing sections, we had an overview of how the deeming fiction operates under the domestic Income Tax Act. But what happens in case of a transaction involving a non-resident?

THE CRUX OF THE QUESTION IS WHETHER A DEEMING FICTION UNDER THE INCOME TAX ACT CAN BE EXTENDED TO DTAA?

To answer this question, it is first important to understand the role of a DTAA. In layman’s terms, DTAA is an agreement for assigning taxing rights between two countries, while the domestic tax act (in this case the Income Tax Act) provides the rule of taxation within the jurisdiction of a nation.

In the Income Tax Act, section 90/90A provides the power to the Central Government to enter into agreements with other nations inter alia for: (i) Providing relief from the income charged in both the countries; (ii) Eliminate the double taxation in respect of income; (iii) Exchange of information for the prevention of evasion or avoidance of income tax; and (iv) For recovery of income under the ITA and corresponding law in other country.

In an ideal world, a domestic tax act and a DTAA would co-exist with the utmost harmony and there would be no contradictory provisions or need for intervention to interpret the said agreements.

Since this utopian assumption does not hold true, it becomes essential to understand that the purpose of DTAA and the Income Tax Act are overlapping and can be sometimes contradictory to each other. The Income Tax Act being an act of Parliament, while the DTAA being an agreement negotiated between two countries is not expected to be fully in harmony with each other.

Thus, what happens in case the provisions of the DTAA and the Income Tax Act are not complimentary to each other- CBDT had shed some light on the above issue in the past and stated that where a specific provision is made in the double taxation avoidance agreement, that provisions will prevail over the general provisions contained in the Income-tax Act.14

14 Circular No. 333 of 1982 dt 02.04.1982

The above issue also came up for consideration before the Hon’ble SC from time to time and it has been observed that the terms of the DTAs would override the provisions of the Income-tax Act in the matter of ascertainment of chargeability to income tax and ascertainment of total income, to the extent of inconsistent with the terms of the domestic tax act.15 Let us look at the below practical examples to understand the interplay between the Income Tax Act and DTAAs better.

15 [2003] UOI vs. Azadi Bachao Andolan: 263 ITR 706 (SC)

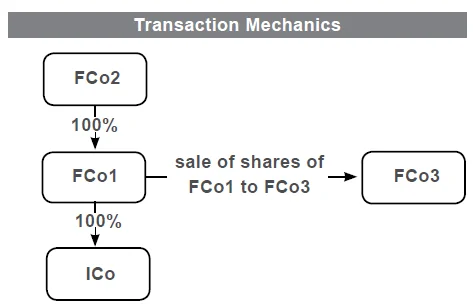

- Indirect transfer of shares:

Background

Perhaps the most disputed use of the deeming fiction was exercised by the legislature in 2012 by way of taxation of indirect transfers. Essentially, the Indian legislature sought to tax sale of shares between two non-residents which involved value shifting of an Indian company. The above can be better understood with the following example:

FCo1, FCo2 and FCo3 are foreign companies. FCo1 has only one asset which is the shares held in the Indian company, viz, ICo. Similarly, FCo2 in-turn has only one asset, viz, shares held in FCo1. FCo3, another foreign company is keen to buy out the interest of FCo2 in ICo. Therefore, it is decided to sell the shares of FCo1 to FCo3 by FCo2 as against selling shares of ICo directly.

The Revenue, in the said case advocated the application of a ‘look through’ approach and contended that if there is a transfer of a capital asset situated in India ‘in consequence of’ an action taken overseas, then all income derived from such transfer should be taxable in India. The Hon’ble Apex Court, however, held that the transfer of shares of a foreign company which had an Indian Company as its subsidiary does not amount to transfer of any capital asset situated in India.

Thus, prior to 2012, the above transaction would not lead to any adverse tax implications in India as it is essentially sale of foreign company shares from non-resident to another non-resident. To bring such apparent value shift transactions within the tax net of India, the erstwhile government moved a retrospective amendment deeming that shares of a foreign company that derive their value substantially from Indian assets (in this case FCo1) shall be deemed to have their situs in India and overruling prevailing decisions in the favor of the taxpayer16

16 Vodafone International Holdings B.V. vs. UOI: [2012] 204 Taxman 408 (SC)

TAXATION OF INDIRECT TRANSFER UNDER THE INCOME TAX ACT

For a non-resident to be taxed in India, section 5 of the Income Tax Act provides that income which accrues/arises or received or is deemed to accrue/arise or received in India shall form part of total income taxable in India.

Explanation 5 to section 9 (1)(i) of the Income Tax Act, provides for levy of tax in India on gains arising on transfer of shares of a foreign company if shares of such foreign company derive substantial value from assets located in India. Given the threshold provided under explanation 6 to section 9(1)(i) of the Income Tax Act are satisfied, the sale of the shares of FCo1 would be taxable in India as the same would be deemed to have their situs in India.

INTERPLAY WITH DTAAs

The interplay of indirect transfer provisions with the provisions of DTAA has been an intensely debated one. This question came up for consideration before the Andhra Pradesh High Court17: whether sale of shares of a French company (which derived value substantially from shares of an Indian company) to another French company would be brought to tax as per the provisions of section 9(1)(i) of the Income Tax Act read with the provisions of the India-France DTAA.

17 Sanofi Pasteur Holding SA vs. Department of Revenue: [2013] 354 ITR 316 (AP)

The Revenue had put forth an argument that the provisions of article 14(5) of the India-France DTAA be interpreted to adopt a more see through approach, however, that was swiftly rejected by the Hon’ble Court on the ground that Article 14(5) does not provide for an enabling language to effect a see through and bring the tax of the same into India.

On the contrary, such indirect transfer maybe brought to tax had the criteria laid out in article 14(4) of the India-France DTAA be fulfilled. Article 14(4) of the India-France DTAA provides for taxing the gains arising out of sale of capital stock of a company the property of which consists directly or indirectly principally of immovable property situated in India. Similar enabling provisions are also captured in the India-UAE DTAA [Article 13(3)].

In the absence of fulfilling the above criteria, the provisions of indirect transfer would not be applicable on a foreign company. The tax authorities have also litigated the aspect of residency (which would directly impact the availability of DTAA benefit) and have urged the Courts to lift the corporate veil and differentiate between via the ‘head and brain test’. This issue has been recently adjudicated by the Apex Court18 in favour of the Revenue. The present article does not take into account the change brought in by such ruling.

18 The Authority for Advance Rulings vs. Tiger Global Internal II Holdings (Civil Appeal No. 262 of 2026) The Authority for Advance Rulings vs. Tiger Global Internal IV Holdings (Civil Appeal No. 263 of 2026) The Authority for Advance Rulings vs. Tiger Global Internal III Holdings (Civil Appeal No. 264 of 2026)

- Period of holding and grandfathering benefit:

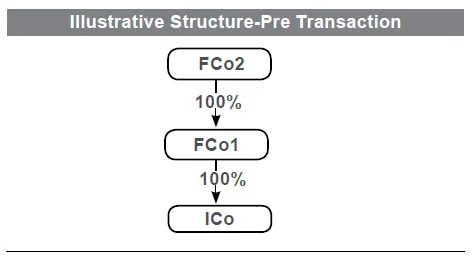

The above issue can be better understood with the help of an example. ICo is an Indian company and the entire share capital of ICo is held by FCo1, and in turn the entire share capital of FCo1 is held by FCo2.

FCo1 and FCo2 are residents of Mauritius. The shares of ICo were acquired by FCo1 on 01.04.2015 and thus are eligible for grandfathering benefit under the India-Mauritius DTAA. The transaction structure, transaction mechanics and resulting structure are as under:

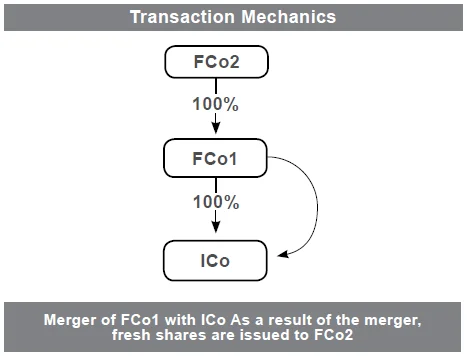

As part of an internal group restructuring exercise undertaken on 01.04.2025, FCo1 is proposed to be amalgamated with ICo and accordingly, ICo would issue fresh shares to FCo2. The proposed transaction mechanics and resulting structure are as under:

Let us first examine the implications under the Income Tax Act on the above transaction- In the above amalgamation, there would be no tax in the hands of FCo2, i.e., the shareholder of the Amalgamation Company, the Income Tax Act provides specific exemption under section 47(vii).

At the time of sale of shares of ICo, FCo2 would be granted the period of holding of FCo1 as well, i.e., period of holding of the previous owner by virtue of section 2(42A) r.w. section 49(1) of the Income Tax Act. Thus, considering the above, the question arises whether the period of holding in the hands of FCo2 of shares of ICo for the purposes of the India-Mauritius DTAA would be considered from 01.04.2016 or 01.04.2025.

The Indian Income Tax Act provides the continuity of period of holding in case of transfer by way of amalgamation. Thus, for the purposes of the Income Tax Act, the period of holding shall be taken from 01.04.2016, i.e., date of original acquisition by FCo1. Thus, the taxpayer can contend on these lines to argue availability of grandfathering benefit on the above shares.

While on the other hand, the tax authorities can place reliance on the provisions of article 13(3A) of the India-Mauritius DTAA, which are operative on the shares acquired on or before 01.04.2017. The tax authorities may further contend that ‘to acquire’ would mean to simply ‘be in control or possession’. In the present case, while the original shares were acquired by FCo1 prior to 01.04.2017, there being a fresh issue pursuant to the merger may result in diluting the position of the taxpayer in claiming the benefit of grandfathering.

Conclusion

Given the language used in the DTAA, the above view to avail grandfathering would in my opinion be extremely litigative considering that there is no enabling provisions replicating the benefit of period of holding granted under the Income Tax Act in the DTAAs.

- Section 2(22)(f)- The Buyback Maze:

Most recently, Infosys, announced a plan to buyback approx. 2.41% of its total share capital for a total consideration of ₹1,800 crores with an aim to boost EPS and market value. Let us look at the implications in the hands of the shareholder(s)/ in the hands of the company in case of a buyback from a tax point of view.

As per the Income Tax Act, buy-back means purchase by a company of its own shares. Prior to Finance Act, 2024, buyback was taxed in the hands of the company under section 115QA of the Income Tax Act. Tax was levied at 20% (plus 12% surcharge and cess) and the buyback would be exempt in the hands of the shareholder.

FINANCE ACT, 2024- POLICY SHIFT:

Finance Act, 2024 introduced a paradigm shift in buyback taxation. By way of Finance Act 2024, the government announced that buyback done post October 1, 2024 would be exempt in the hands of the company undertaking the buyback and would be taxed in the hands of the shareholder as dividend under section 2(22)(f) per their applicable slab rates.

Further, cost of acquisition of the shares would be allowed as capital loss in the hands of the shareholder. This policy shift has brought buyback on par with dividend but has taken away the sheen of buyback being a lucrative choice of cash repatriation. In many DTAAs such as the India-Netherlands DTAA, it can be argued that given the meaning ascribed to dividend, the proceeds from buyback shall fall within the ambit of the same.

CAN ANTI-ABUSE PROVISIONS SUCH AS SECTION 56(2)(x) OR SECTION 50CA BE APPLIED ON BUYBACK POST FINANCE 2024?

Section 50CA of the Income Tax Act is applicable in case of transfer of unquoted shares at a value less than the fair market value of such shares determined in accordance with the provisions of Rule 11UAA of the Income Tax Rules, 1962 (‘the Income Tax Rules’). Therefore, section 50CA provides for substituting the consideration with the fair market value (determined as per Rule 11UAA of the Income Tax Rules) for the purposes of section 48 and is applicable in the hands of the Seller.

While as discussed above, section 56(2)(x) of the Income Tax Act seeks to tax receipt of property (including shares) for nil or inadequate consideration. Therefore, a key differentiating factor is that section 56(2)(x) is applicable in the hands of the ‘recipient’ of shares (i.e., buyer in case of a transaction of sale/purchase of shares) and section 50CA of the Income Tax Act is applicable in the hands of the seller of shares (in case of a transaction of sale/purchase of shares).

In the present case, the risk of buyback being engulfed under the ambit of section 56(2)(x)/section 50CA of the Income Tax Act is enumerating from the plain reading of provisions of the said sections. The crux of the problem- can two deeming fictions be read on a conjoint basis? Or can a deeming fiction be read into another deeming fiction?

SECTION 50CA AND BUYBACK:

In case of section 50CA of the Income Tax Act, as discussed above, it is applicable in case of ‘transfer’ of unquoted shares. The term ‘transfer’ has been

defined under section 2(47) of the Income Tax Act and includes the relinquishment of any asset or extinguishment of any rights therein. In case where a company buys back its own shares for the

purpose of cancellation/extinguishment, the same can be said to fall within section 2(47) of the Income Tax Act and thus within ambit of section 50CA of the Income Tax Act.

However, since payment made a company on buyback of its own shares from a shareholder in accordance with the provisions of section 68 of the Companies Act, 2013 is covered within section 2(22)(f) of the Income Tax Act, the same may not be taxed again under the head capital gains in line with the provisions of section 46A of the Income Tax Act. Thus, where section 50CA is sought to be invoked by the tax authorities, the same may leave the provisions of section 46A (supra) otiose.

SECTION 56(2)(x) AND BUYBACK:

In case of section 56(2)(x) of the Income Tax Act, the company receives its shares from the shareholder for the purpose of cancellation of the same. At the outset, arguments can be made that receipt of shares for the purposes of cancellation may not fall within purview of section 56(2)(x) of the Income Tax Act keeping in mind the intent for which the provisions of section 56(2)(x) were introduced.

Further arguments can also be made that in case of buyback, the shares are being tendered which would constitute consideration. The action of a deeming fiction is to be restricted to the section(s) for which they were originally intended for and the extension of the said scope under the Act is not permissible.

However, alternative arguments may be advanced by the departments that on a bare reading of section 56(2)(x) of the Income Tax Act, only trigger(s) required are receipt of property (including shares) for inadequate consideration. The intent of receipt (in the present case for cancellation) may not be principally examined for application of section 56(2)(x) of the Income Tax Act.

In my view, the above anti-abuse provisions also no longer find any application in case of a buyback for the plain reason that post Finance Act, 2024, the companies undertaking a buyback would need to incentivize the shareholders to tender their shares by way of a premium on prices (as seen in the case of Infosys). Thus, there would not be any practical applicability of the above anti-abuse provisions.

CONCLUDING REMARKS

Deeming fictions under the Income Tax Act have transitioned from being narrow anti-abuse tools to becoming a cornerstone of tax legislation, influencing computation, timing, and characterisation of income.

While they serve the purpose of plugging loopholes and ensuring uniformity, their expansive use has also introduced interpretational challenges and litigation risks. Like in mathematics, in a world full of variables it is essential to introduce and keep constants as a balancing factor, likewise in law interpretation to keep up with our dynamic world, it is important to keep some constant premise for a meaningful and desired interpretation.

It was also discussed how we can prioritize the different aspects of our life like Financial, Professional, Social, Personal, Physical, Spiritual and bring harmony and purpose in our life, while we grow as well as be happy all the time. The presenter taught how to overcome distractions in the way of accomplishments and retain the mindset to focus.

It was also discussed how we can prioritize the different aspects of our life like Financial, Professional, Social, Personal, Physical, Spiritual and bring harmony and purpose in our life, while we grow as well as be happy all the time. The presenter taught how to overcome distractions in the way of accomplishments and retain the mindset to focus.  This meeting was conceived by the Corporate and Allied Laws Committee of BCAS and was jointly organized with the BSE. Mr. Neeraj Kulshrestha (Chief of Business Operations – BSE) was the Guest of Honour, Mr. Ajay Thakur (Head – BSE SME) was the keynote speaker and Mr. Mahavir Lunawat, (Founder – Pantomath Group) was the speaker for the day. Mr. Kanu Chokshi (Chairman, Corporate & Allied Laws Committee) chaired the meeting. Mr. Raman Jokhakar (President, BCAS) welcomed the participants and highlighted the relevance of the topic in view of the proposed ‘Startup India’ and ‘Standup India’ initiatives, launched by the Government of India. Mr. Kanu Chokshi briefly introduced the speakers and the topic.

This meeting was conceived by the Corporate and Allied Laws Committee of BCAS and was jointly organized with the BSE. Mr. Neeraj Kulshrestha (Chief of Business Operations – BSE) was the Guest of Honour, Mr. Ajay Thakur (Head – BSE SME) was the keynote speaker and Mr. Mahavir Lunawat, (Founder – Pantomath Group) was the speaker for the day. Mr. Kanu Chokshi (Chairman, Corporate & Allied Laws Committee) chaired the meeting. Mr. Raman Jokhakar (President, BCAS) welcomed the participants and highlighted the relevance of the topic in view of the proposed ‘Startup India’ and ‘Standup India’ initiatives, launched by the Government of India. Mr. Kanu Chokshi briefly introduced the speakers and the topic. Moving to the product zone, the team saw samples of each product processed out of the refinery, namely Propylene, Naptha, Gassoline, Jet/Aviation Turbine Fuel, Sulphur, Petcock etc. Participants were fortunate to visit control room. The entire refinery is controlled from this area. The control room has earmarked the area for each unit – Fluid catalytic cracking unit (FCCU), clean fuel plant (CFP), Hydrogen manufacturing unit (HMU), Reliance tank farm (RTF ) and so on.

Moving to the product zone, the team saw samples of each product processed out of the refinery, namely Propylene, Naptha, Gassoline, Jet/Aviation Turbine Fuel, Sulphur, Petcock etc. Participants were fortunate to visit control room. The entire refinery is controlled from this area. The control room has earmarked the area for each unit – Fluid catalytic cracking unit (FCCU), clean fuel plant (CFP), Hydrogen manufacturing unit (HMU), Reliance tank farm (RTF ) and so on.