The Income-tax Act, 2025 replaces the 1961 law, effective from 1 April 2026, with the stated aim of simplification, modernisation, and digital alignment. It introduces a single “Tax Year”, logical reorganisation of provisions, removal of redundant clauses, and greater use of tables and formulae. The Act codifies faceless governance, modernises residence rules, streamlines assessment timelines, strengthens dispute resolution, and consolidates deductions and retirement benefits. It explicitly taxes Virtual Digital Assets (VDAs) and empowers authorities to access digital space during searches. While the Act improves readability and aligns with global practices, critics argue it largely preserves old complexities. Transitional provisions on losses, MAT credits, and incentives may trigger litigation. Key pain points—complex TDS/TCS rules, refund delays, weak taxpayer rights, and lack of automatic indexation—remain unresolved. Thus, the Act represents progress in design and digital readiness but is viewed as a missed opportunity for deeper structural reform.

The Income-tax Act, 2025(‘Act’) is introduced as a significant legislative reform in India’s direct tax landscape, replacing the six and a half decade old Income-tax Act, 1961(‘ITA’). While the core

principles of taxation and the scheme of taxation of income remain broadly the same, the 2025 legislation has the objective of introducing clarity, simplicity, and modernity to align with present-day business realities and digital compliance needs. The focus of the Act is on reducing complexity, consolidating provisions, and strengthening the governance framework.

It has attempted to improve taxpayer access and compliance by reorganising provisions logically besides removing obsolete provisions, consolidating duplicate rules, harmonising definitions, and introducing a formal “tax year” concept to align administrative and accounting practices. Special emphasis on use of plain English, sequential numbering, avoiding alphanumeric clauses is clearly visible.

The Act comes into effect from 1 April 2026 (Tax Year 2026-27 onwards). It contains the mandatory transitional provisions that ensures the continuity for pending matters under the ITA. It saves the applicability of the otherwise repealed provisions of the ITA for the ongoing assessments, appeals, and proceedings pending or initiated under the ITA, which will continue under the old law until concluded. New filings and compliances w.e.f. 1st April 2026 will fall under the framework of the Act. This phased transition has the effect of ensuring stability and avoiding disruption for taxpayers and the administration.

In 2017, the Prime Minister proposed replacing the Income-tax Act, 1961, echoing Kanga and Palkhiwala’s concern in their Eighth Edition of 1990, warning that excessive amendments had made the law a “national disgrace”. The revered authors also cautioned against mistaking constant change for progress and stressed stability in fiscal policy. The 2025 Act, while not a radical departure, represents a modernization of direct tax law. It emphasizes simplicity, digital readiness, global alignment, and dispute reduction. Key features include the tax year, consolidated deductions, faceless governance, and recognition of digital assets. Though concerns remain over search powers and delegated legislation, the Act promises clarity, stability, and reduced complexity.

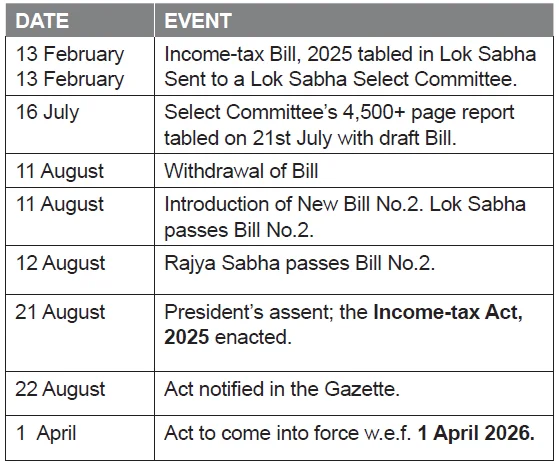

For statistically oriented readers, the Timeline of the journey of the Bill to Act in 2025 is tabulated below:

The important recommendations of the PSC that made it into the final Act are consolidation of the faceless schemes and administration, enabling powers of the search party to access the virtual digital space, clarifying the rules for the tax treaty interpretation for undefined terms, need for DRP to pass a reasoned order, maintaining the status quo for determination of the annual value of the vacant house property, saving small taxpayers from penalties and continuity of rates and structure. The Legislature accepted the suggestions that the act of fixing the drafting anomalies in the ITA under the Act should not be construed as a policy change and the core architecture of the ITA is retained.

Structurally, the Act reorganises chapters and sections to group related concepts (residence, charge, exemptions, computation, assessments, appeals and penalties) in a more logical order. The Act replaces many legacy cross-references with self-contained provisions and removes archaic language.

A visible drafting change is sequential numeric sectioning (no “80C(a)(i)”) and an attempt to shorten and standardise definitions. The section count changed (some commentators note fewer words but reorganised numbering), but substance is largely intended to be continuous with earlier law unless expressly altered. The Act also reorganises timelines for assessment, reassessment and collection to be more consistent with modern IT systems and taxpayer needs.

Use of tables (increased to 57 from 18) and formulae (increased to 46 from 6) and illustrations in many sections instead of long textual (proviso/explanation) clauses are laudable and will have the effect in simplifying the otherwise complex provisions of law. This is intended to make computation / interpretation more straightforward. More use of schedules to group related items, clearer definition sections make the law easier to understand. Explanations / provisos are replaced by sub-sections or clauses, making the law modular.

Income tax in India began in 1860 to meet post-1857 financial needs, evolving through license and certificate taxes, and regular income tax in 1869, which was soon abolished. The 1886 and 1918 Acts formalized taxation, introducing six heads of income. The 1922 Act centralized administration, and was later replaced by the Income-tax Act, 1961, which became dense, amendment-heavy, and litigation-prone. Attempts to replace it with the Direct Tax Code (2012) failed. The Task Force appointed attempted to draft a modern, simplified tax law addressing global practices, faceless assessments, compliance reduction, and dispute minimization. The Income-tax Act, 2025 was enacted, modernizing and replacing the 1961 framework.

Territorial connection, and extraterritorial operation of the Act. The Bill introduced as a Money Bill, on enactment is made applicable to the whole of India, including the Union territories and the state of Jammu & Kashmir, as also to the Continental Shelf of India and the Exclusive Economic Zone of India for the extraction and production of mineral oils and the specified services, with the intended application to extra-territorial transactions. The extra-territorial operation of some of the deeming provisions of the Act should not render such provisions invalid or ultra vires the Indian legislature. Given a sufficient territorial connection or nexus between the person sought to be charged and India, levy of income-tax is validly extended to that person in respect of his foreign income. Like under the ITA, once the connection to the Indian territory is real, its extent is not relevant in considering the validity of the legislation. The connection under the Act is founded on the residence of the person or business connection within the Indian territory and the situation within India, of the money or property from which the taxable income is derived. These factors of the Act are sufficient to establish a territorial connection.

Constitutional validity: At first blush, the Act imposing the tax is constitutionally valid in as much as it has been passed by the legislature that was competent to pass it; and does not prima facie in its overall form contravene any of the fundamental rights guaranteed by Part III of the Constitution. Being a law relating to economic activities, it will be viewed with greater latitude than laws touching civil rights, such as freedom of speech, freedom of religion, etc. Unless and until a Court declares any provision to be ultra vires, the Act appears to be constitutionally valid and would be treated as such. In any case, there is always a presumption in favour of the constitutionality of a statute passed by the legislature, and the burden is upon him who attacks it to show that there has been a clear transgression of the constitutional principles.

Legislative Competence: In ‘pith and substance’ the legislation passed falls within the Seventh Schedule, List I and III of the Constitution of India. The four essential ingredients in a taxing statute namely: – (a) subject of tax; (b) person liable to pay the tax; (c) rate at which tax is to be paid, and (d) measure or value on which the rate is to be applied, are present in the Act. The Act that has been passed by the Legislature is within its competence to levy tax. Provisions carry the mechanisms and machinery for assessment of income and do not appear to be arbitrary. Provisions of presumptive taxation provide for opting out. Adequate transitional provisions are put in place and the classifications appear to be fair and reasonable. It contains the necessary machinery for levy of tax and its collection.

Article 246 read with Entry 82 of List I; Seventh Schedule of the Constitution empowers Parliament to levy taxes on income other than agricultural income. Article 265 requires that no tax be levied or collected except by authority of law. The 2025 Act, being a duly enacted parliamentary statute, satisfies this requirement. Article 14 (Equality clause) and Article 19 (1) (g) (Right to trade) place limits: taxation must not be arbitrary, discriminatory, or confiscatory. Classification for taxation under the Act appears to be valid as it is based on an intelligible differentia and has a rational nexus with the object of the law.

Thus, while particular provisions may face judicial scrutiny (especially transitional and incentive-related clauses), the Act as a whole stands on solid constitutional footing.

The Act is Exhaustive: The Act is Exhaustive in as much as it is a self-contained code, exhaustive of the matters dealt with therein. It however does not override the power of the Supreme Court under Article 32 of the Constitution, and of the High Courts under Article 226 of the Constitution, to issue, in appropriate cases, writs in the nature of certiorari, prohibition or mandamus or other directions or orders to examine the vires of the Act.

CONCEPTUAL & IMPORTANT CHANGES

1. Structural Overhaul and Simplification: The most visible feature of the Act is the streamlined structure. The ITA had around 819 sections spread across 47 chapters with a word count of nearly 500,000. The Act consolidates the provisions into 536 clauses under 23 chapters, reducing the word count to approximately 260,000.

- About 650 Provisos and 490 Explanations have been eliminated and are replaced by formula-based and tabular presentation wherever possible and/or are captured as sub-sections and sections.

- Presentation of the chapters follows a more logical sequence by first covering charging, compliance, assessments, TDS, TCS, taxes, recovery and dispute resolutions including the appeals followed by the penalty and prosecutions chapters in a linear manner.

- The simplification reduces interpretational ambiguities and ensures easier navigation for taxpayers, practitioners, and judicial authorities.

This design move alone is expected by the Government to improve compliance and cut down on litigation, which was often driven by complexity and multiple provisos.

2. Introduction of the “Tax Year”: One of the most important conceptual innovations is the replacement of the dual concept of “Previous Year” and “Assessment Year” with a unified “Tax Year.”

- Under the old regime, income was earned in the “Previous Year” but taxed in the “Assessment Year.”

- The new Act simplifies this by taxing income in the same Tax Year in which it accrues or arises.

This global best practice reduces confusion for taxpayers and aligns India with international tax systems. It also eliminates several interpretational disputes that arose from mismatches between the two years.

3. Emphasis on Digital Governance and Faceless Regime: The Act codifies India’s transition towards technology-driven administration.

- Faceless assessments, reassessments, appeals, and penalty proceedings are given a consolidated statutory foundation.

- All schemes for reducing interface between taxpayers and officials are brought under one enabling provision, subject to parliamentary oversight.

- E-filing of reports, returns, online payment of taxes, and digital communication of notices and responses are made the norm, reinforcing transparency and reducing subjectivity.

This shift supports the government’s vision of “minimum government, maximum governance” in tax administration.

4 Scope of taxation: One important conceptual strand in the Act is emphasis on “taxation on receipt” for certain items, and clearer rules for deemed income; the Act expressly addresses the issue of when income is to be treated as arising or being received. This clarity is intended to limit disputes over accrual versus receipt.

5. Residence: Residence rules have been rewritten to reflect modern mobility. The definitions and thresholds for residence and ordinarily resident status are rationalised to reduce uncertainty for digital nomads, expatriates and cross-border workers. Practitioners must check transitional rules carefully for individuals who change residence around the enactment date.

6. Deeming fictions: For particular classes of income (certain transfers of capital assets, stock-in-trade receipts from specified persons/entities) the Act contains express deeming provisions to tax amounts on receipt or on specified events — a shift intended to close gaps that previously caused mismatch and litigation.

7. Timelines and procedures for assessment, etc: The Act shortens and clarifies assessment and reassessment timelines, introduces clearer grounds and procedures for reopening assessments, and puts emphasis on pre-deposit and fast track dispute resolution mechanisms in some categories. It requires dispute panels to state points of determination and reasons for decisions.

These procedural changes aim to reduce lengthy litigation and multiple revisits of facts, but they also shift pressure onto initial fact-finding and show-cause stages. If case records are incomplete or notices poorly drafted, taxpayers may face hard choices within shorter windows.

8. Expanded Search and Seizure Provisions: The Act modernizes the powers of the revenue authorities in conducting the search and seizure operations.

- The Act explicitly empowers officers to access “virtual digital space” during searches.

- Tax authorities can access emails, social-media accounts, online trading platforms, and cloud storage, even by bypassing access codes.

- These powers aim to curb tax evasion in an era where digital transactions are widespread.

While such provisions strengthen enforcement, they also raise privacy and constitutional concerns, requiring careful implementation and judicial oversight.

9. Virtual Digital Assets (VDAs) Brought Within the Net: Unlike the ITA, the new law explicitly recognizes Virtual Digital Assets (VDAs) such as cryptocurrencies, NFTs, and digital tokens as capital assets or stock-in-trade.

- VDAs are included in the definitions of “property” and “income.”

- They are also covered under provisions relating to undisclosed income and search powers.

- The Act, while explicitly widening the coverage for “virtual digital assets” (VDAs), cryptocurrencies and income generated through online platforms, aims to update the tax-base, define reporting obligations, and (in some cases) prescribe withholding rules. The aim is to reduce ambiguity that existed under piecemeal amendments to the ITA.

- Simultaneously, withholding, reporting and data exchange rules are strengthened to leverage digital reporting (AIS, TDS/TCS modernisation). Practical implementation depends heavily on IT systems and data quality. That reliance both enables better compliance and creates operational risk if systems or guidance lag.

By acknowledging digital wealth, the Act ensures that taxation keeps pace with financial innovation, while providing clarity to investors and businesses dealing in such instruments.

10. Rule-Making Powers and Delegated Legislation: The Act strengthens the hands of the Central Board of Direct Taxes (CBDT).

- CBDT has been given wider authority to frame schemes, rules, and notifications to operationalise provisions.

- This reduces the need for constant legislative amendments while ensuring adaptability to changing circumstances.

At the same time, these rules must be placed before both the houses of the Parliament, preserving accountability and checks on delegated legislation.

11. Rationalisation of Deductions and Exemptions: The Act consolidates numerous deductions and exemptions which were earlier scattered across multiple sections.

- Benefits relating to gratuity, leave encashment, voluntary retirement, and commuted pension are grouped under one head for ease of reference.

- Deductions under sections like 80G (donations) and 80TTA/80TTB (interest income) are rationalised and clarified.

- Formula-based ceilings and tabular presentation make the provisions more user-friendly.

This rationalisation reduces duplication and ensures that taxpayers understand eligibility in a straightforward manner.

12. Modernised Dispute Resolution Framework: The Act seeks to address the chronic problem of tax litigation through enhanced dispute resolution mechanisms.

- The Dispute Resolution Panel (DRP) must now record specific points for determination and provide reasoned directions.

- Provisions for Dispute Resolution Committees (‘DRC’s) offer relief to small taxpayers by enabling faster settlements.

By providing multiple forums and streamlining procedures, the Act aims to reduce prolonged litigation and increase certainty.

13. Anti-Avoidance and International Taxation: The General Anti-Avoidance Rule (GAAR) has been retained but clarified. Arrangements lacking commercial substance and aimed primarily at tax benefits will be disregarded.

- Treaty interpretation is codified: if a term is undefined in the treaty, the Act, or relevant notifications, it’s meaning may be sourced from other central laws.

- The Act attempts to update many international tax linkage points: residence tests, source rules, permanent establishment concepts and rules addressing cross-border digital supplies. It attempts to harmonise domestic law with BEPS/follow-up OECD standards and recent treaty models, but practical divergence and map-ping to treaty text will remain a complex exercise.

- Issues will arise in interpreting domestic withholding obligations where treaties provide differing attribution rules; practitioners should watch guidance on treaty override, operation of tax credits and thin-capitalisation or withholding rules that interact with treaty relief.

- This hierarchy of interpretation provides clarity and consistency in cross-border tax matters.

Such provisions strengthen India’s stance against aggressive tax planning while ensuring harmony with international tax laws.

14. Privacy, Safeguards, and Checks: While the Act grants sweeping powers for search and seizure, including access to digital devices, it simultaneously emphasizes transparency and accountability.

- Schemes for faceless procedures must be notified and laid before Parliament.

- The DRP’s requirement of speaking orders increases judicial discipline.

- Penalties are rationalised to ensure that taxpayers are not punished for minor or technical defaults.

Balancing enforcement with rights protection remains a key theme of the new Act.

15. Pension and Retirement Benefits: Retirement benefits have been streamlined for clarity.

- Provisions relating to pension, gratuity, and commuted pension are now consolidated.

- Exemptions are clearly defined with formula-based thresholds and moved into schedules for easier reference.

- The Act ensures that salaried employees and retirees can understand their entitlements without navigating through scattered provisions.

This will benefit senior citizens, a category often affected by interpretational challenges under the old law.

16. Transition: The devil lies in the details. Any new codification requires transitional rules. The Act contains express transitional provisions for pending assessments, appeals, unabsorbed losses, credits, and ongoing litigations. These provisions are crucial because they determine whether prior tax positions will be preserved or reinterpreted under the new drafting.

Practitioners must scrutinise each transitional clause: loss carryovers, depreciation bases, pending notices and the status of settled legal interpretation under the ITA may be dealt with differently. Early commentary warns that insufficiently precise transitional wording can spawn fresh litigation.

17. Penalties, compliance costs and rationalisation: The Act retains penalties but seeks to rationalise and tier them to reduce disproportionate fines for technical defaults. Nonetheless, new reporting obligations (especially for VDAs and platform economy) may increase compliance costs, particularly for small-medium enterprises and individuals unfamiliar with digital reporting.

Where no tax is payable or refund is due, the provisions for levy of penalty are relaxed to exempt such cases from levy of penalty in MSME and other small cases. Where levy of penalties is administrative and automated, appeals will likely increase if taxpayers perceive disproportionate enforcement; hence the interplay between automated data matching and human oversight is a systemic risk.

What Remains /Conserved: Some core principles remain unchanged and are retained:

- Tax rates/slabs have largely been retained; the new Act is not introducing new rates drastically in many segments.

- Fundamental heads of income (salaries, house property, business/profession, capital gains and other sources) remain but are refined.

REPEALS & SAVINGS AND TRANSITIONAL PROVISIONS FOR RETAINING THE LEGACY

Section 536 of the Act explicitly repeals the ITA. At the same time, it contains the savings clause for protecting the past operations. Actions already taken, rights acquired, or obligations incurred under the ITA remain unaffected by the repeal. Pending proceedings for example, assessments, reopening, reassessments, rectifications, appeals, penalties, references, revisions, or any related proceedings related to tax years beginning before 1 April 2026 would continue under the ITA; procedures. penalties and proceedings for the earlier years in respect of pre -1st April 2026 tax years would continue to be initiated and pursued as if the ITA has not been repealed but is continued and has remained in force. Pending proceedings before the tax authorities, initiated under the ITA and pending on 1 April 2026, will be adjudicated under the ITA. Refunds or defaults transiting into the Act after 1 April 2026, but relating to the proceeding under the ITA, shall be governed by the ITA for the period up to 31st March, 2025 and thereafter under the Act.

Importantly, no revival or reopening of the lapsed opportunities would be possible under the Act where the time limit to file an application, appeal, reference, or revision has already expired under the ITA on or before 1 April 2026; the Act does not revive or reopen any of them even if it offers longer periods. To reiterate, the legacy law of the ITA shall remain in force in the above referred cases even though the law is otherwise repealed w.e.f 01.04.2026. Law of limitation of the ITA shall apply to the filings, including of the appeals, and where such limitation had expired under the ITA before 1st April 2026, will not get the fresh lease of time under the Act, even if the latter provides more generous timelines.

Express provisions that save the application of the ITA ensures the legal continuity, guarantee a smooth transition without legal uncertainty and render fairness to taxpayers in as much as no pending matters or rights are disrupted or lost due to the repeal of the ITA. Importantly, administrative clarity is achieved with the clear demarcation between old and new regiments.

The principle underlying s. 6 of the General Clauses Act, 1897 providing for the savings for proceedings for liabilities incurred during the currency of the previous law may apply to a law that is repealed. Section 24 of the General Clauses Act, 1897 provides for continuation of orders, notifications etc., issued under enactments repealed and re-enacted. In such instances, if repealed and re-enacted provisions are not inconsistent with each other, any order or notification made under the repealed provisions is deemed to be an order made under the reenacted provisions. Having noted the process, it appears that the prescription will fall short of ensuring the litigation free transition as is highlighted, while dealing with the shortfalls of the exercise.

KEY TRANSITIONAL AREAS AND CHALLENGES

During the transition from the ITA to the Act, several key areas, particularly the following require careful consideration;

- Pending assessments and reassessments initiated under ITA will continue under that law or may be deemed under the Act in specified cases. However, disputes may arise on whether the old or new procedure applies, particularly where reassessment timelines differ.

- Appeals already filed under the ITA will proceed before the existing appellate forums, but issues of forum shopping and jurisdictional objections may surface if the new Act alters hierarchy or timelines.

- Unabsorbed losses and depreciation under the ITA are intended to be carried forward into the new Act. Nonetheless, disagreements may occur regarding speculative or business losses, and whether the restrictions of the old law or the new law would govern such carry forwards.

- Similarly, MAT/AMT credits and tax credits such as TDS, TCS, and foreign tax credits accumulated under the ITA will be permitted under the new Act, though timing mismatches – especially for foreign tax credits claimed on accrual—could lead to litigation.

- Exemptions and deductions available under the ITA, including SEZ, start-up, and infrastructure incentives, will be grandfathered until expiry. Yet, ambiguity is likely where such benefits are linked to repealed provisions, leading to potential disputes on preservation of benefits.

- Corporate restructurings commenced under the ITA but completed after 2025 are intended to retain tax neutrality, though gaps may arise if the new Act omits certain neutralisation provisions, such as those relating to demergers or dividend upstreaming.

- Lastly, penalties and prosecutions for defaults committed under the ITA remain punishable under that law. Complications may occur where defaults span both the regiments, and constitutional challenges could arise if penal consequences differ between the two laws.

INTERPRETATION OF THE ACT

The Act of 2025 must be interpreted strictly according to its express words, with no tax imposed without clear legislative authority. Implied intentions or “spirit of the law” cannot create liability. The principle “there is no equity in taxation” applies, so equity cannot override statutory language. Ambiguities favour the taxpayer, and taxation cannot be extended by inference, analogy, or implication. Interpretation is confined to what is explicitly stated in the statute.

The Act of 2025 must be interpreted as a whole, ensuring harmonious construction so that no section renders another redundant and apparent inconsistencies are reconciled within the Act or with related statutes. Beneficial interpretation applies: where two meanings exist, the one most favourable to the taxpayer prevails, recognizing the power imbalance with authorities. Natural justice principles also apply unless explicitly excluded, requiring meaningful opportunity to be heard and substantive consideration of submissions. Ritualistic hearings or orders ignoring taxpayer arguments are unsustainable. Overall, interpretation must balance consistency, fairness, and protection of the taxpayer while furthering the Act’s purpose.

Legislative Simplification – Reality or Illusion? The Act has been presented as a major simplification exercise. Provisos, Explanations, and Non-obstante clauses have been formally removed, and definitions consolidated into a single section. The term ‘as maybe prescribed’ is replaced with ‘as prescribed’. The government has argued that this will reduce complexity and litigation.

Many of these important aids to interpretation, the meaning whereof is judicially settled, have merely been reintroduced as sub-sections or substantive provisions. If their language remains, but in a different form, it is debatable whether genuine simplification has been achieved. Historically, provisos, explanations, and non-obstante clauses served special interpretive functions. By converting them into sub-sections, the Act may blur distinctions and give rise to fresh interpretive disputes. Judicial rulings on the role and effect of these interpretive devices may or may not remain applicable. It is, therefore, premature to conclude that the changes will reduce litigation. Courts will ultimately determine their true import.

Provisos. Traditionally, a proviso carves out exceptions or qualifies the main provision. It cannot nullify the substantive enactment, but it may provide conditions or remedy unintended consequences. A proviso may:

- Qualify or except certain cases from the main enactment.

- Impose mandatory conditions necessary to make the enactment workable.

- Become so integral as to acquire the colour of the main enactment.

- Serve as an explanatory addendum clarifying legislative intent.

Provisos must always be construed harmoniously with the main provision. In some cases, where necessary to give effect to legislative intent, a proviso may even operate retrospectively. In the circumstances, it is difficult to concur with the Government that the Provisos were a burden under the ITA and shifting them to the sub-sections shall retain the same meaning, more so where the understanding of the true import of the Provisos has been justified by the courts.

Explanations. An Explanation is designed to clarify ambiguities, widen scope, or reinforce the object of the Act. Generally, clarificatory and retrospective in effect, Explanations cannot override substantive provisions but can guide interpretation. They may explain phrases, supply missing links, or resolve vagueness in language.

Although ordinarily not substantive, Explanations can sometimes expand the scope of a section, depending on legislative intent. Courts will give effect to such intention even if the provision is labelled as an “Explanation.” It is again difficult to concur with the Government that the Explanations were redundant and its purpose is served by shifting to the main provisions; shifting them to the sub-sections may not retain the same meaning, more so where their understanding of the true import has been justified by the courts.

Non-Obstante Clauses. A non-obstante clause, typically beginning with “notwithstanding anything,” gives overriding effect to the section it qualifies, in case of conflict with other provisions. It is a legislative device to ensure primacy in specified circumstances. The scope of a non-obstante clause is determined by its context and the scheme of the Act. While it provides clarity in resolving conflicts, excessive reliance may undermine coherence.

The Act has replaced everywhere the term ‘notwithstanding’ with the new term ‘irrespective of’. Dictionary meaning of both the terms is interchangeable and therefore neither any harm nor any gain is perceived by the change; it does not complicate the act nor simplify the same.

Definitions and Undefined Words. The Act adopts a novel approach by consolidating definitions into a central section, while also retaining section-specific definitions where necessary. This is intended to create uniformity in interpretation.

However, contextual interpretation remains vital. Defined words ordinarily carry the statutory meaning unless context dictates otherwise. Extended definitions cannot override ordinary meaning unless compelling language demands it. One must ensure that definitions do not destroy the essence of the concept being defined. Thus, while the consolidated definition clause aids clarity, interpretation must remain context-sensitive.

As may be prescribed and As prescribed. At several places the Act, in the name of simplification, has used the term ‘ as prescribed’ in place of the term ‘ as may be prescribed’. It is not possible to corelate with the understanding of the government here. The two terms differ in its meaning as one used under the ITA was futuristic and the other used under the Act has its roots in present. The later requires that the prescription is mandatory and the failure to prescribe may not be made up by the later day prescription.

Deeming Provisions and Legal Fictions: The Act continues to extensively rely on deeming fictions. The best solution would have been to do away with such fictions by using such language that does not require fictions, and instead explains the intent in simple language for creating the effective charge of taxation. Use of legal fictions in the Act is an admission of the legislature of its’ inability to create a specific charge in simple terms. A deeming provision enlarges the meaning of a word or phrase beyond its ordinary sense. Legal fictions must be given full effect, carried to their logical conclusion, but only within the limits of the purpose for which they are created. Courts cannot extend them beyond their defined scope.

While legal fictions may include the obvious, uncertain, or even impossible, they cannot be applied in a way that causes injustice. They are legislative tools to remove doubt, broaden scope, or simplify administration, but require strict interpretation.

Relevance of Legislative History and Judicial Precedent: Legislative history, surrounding circumstances, and background may be considered to understand the object of the Act, though not to alter the plain meaning. Historical context helps identify the mischief the law seeks to remedy. Previous judicial interpretations of similar provisions may also be relevant, particularly where identical wording has been carried forward.

Where Parliament repeats phrases already judicially interpreted, one may infer that the same meaning was intended. At the same time, judicial interpretations under the 1961 Act will not automatically apply; their relevance must be tested in the context of the 2025 Act.

Rules, Circulars and Notifications issued in the context of the ITA may not automatically apply unless specifically provided by the legislature or accepted by the Central Board of Direct Taxes. Recommendation of the Parliamentary Select Committee on this aspect may be seen to understand the position of these useful aids of constructing the Act.

Key Litigation Issues Under the 2025 Act. Despite claims of simplification, several interpretive disputes are anticipated:

- Ambiguity of Key Terms: Definitions of “business connection,” “virtual digital asset,” and “tax year” may give rise to litigation over scope and application.

- Transition from ITA to Act: Whether facts arising before enactment are governed by the repealed Act or the newly enacted Act will be contested. Saving clauses, retrospective application, and transitional provisions will require judicial resolution.

- Set-off and Depreciation: Treatment of losses and unabsorbed depreciation carried forward from the ITA involving high-value cash-flow implications, will be fertile grounds for disputes.

- Corporate Restructuring: Lack of explicit provisions for tax neutrality in reorganisations, fast-track mergers, demergers, and dividend upstreaming may create asymmetries, leading to corporate tax litigation, more so in cases where the restructuring initiated under the ITA is concluded under the Act.

- AIS and Automated Matching: The Act relies heavily on Annual Information Statements (AIS) and automated data matching. Errors in data, lack of human oversight, and limited correction mechanisms may lead to unfair assessments. Taxpayers are expected to challenge these on grounds of accuracy and procedural fairness.

The Act of 2025 represents an ambitious attempt at simplification, but its true test will lie in judicial interpretation. While the express words of the statute remain paramount, the removal and reclassification of interpretive devices, such as provisos and explanations, may lead to fresh uncertainty. Courts will play a crucial role in shaping how the Act functions in practice.

Ambiguities in definitions, transitional provisions, and reliance on technology-driven assessments are likely to drive the first wave of litigation. Until judicial clarity emerges, taxpayers and advisors must proceed with caution, guided by the long-settled interpretive principles that taxation depends strictly on the language of the law, nothing more and nothing less.

IN THE END – MISSED OPPORTUNITY & ROAD AHEAD

Whether the Act of 2025 is a case of a missed opportunity, and what more could / should have been done which the reform did not quite deliver, is the question. While the Act of 2025 is a step forward in reformation of the income-tax law, many observers feel it could have gone further or could have addressed certain areas more fully. Let us first summarise what seem to be the gaps and then suggest what might have been done better.

WHERE THE ACT FALLS SHORT — WHAT IT MISSED

- Incomplete simplification of core tax base and dispute-prone provisions

- Some core concepts like income, scope of total income, deemed income, capital receipts, revenue and capital expenditure and overlapping heads of income remain substantially unchanged, continuing old complexities and challenges.

- Deletion of the deeming fictions that provide for taxation of a receipt that is not an income by any stretch of imagination or of the provisions that presume higher income than the actual or real income.

- Making provisions redundant that provide for disallowance of the legitimate expenditure incurred in earning an income for defaults unrelated to income of a person.

- Scrapping of the provisions that mandate for compulsory payment in cases of persons following the mercantile system of accounting for a legitimate deduction.

- Removal of unfair limitations like mandatory filing of reports, return of loss or income including the revised return of income by due dates. All such provisions that limit the legitimate right to be assessed on the true and correct income irrespective of the date of filing should have been withdrawn.

- Provisions for reopening assessments (which are a large source of litigation and uncertainty), which have largely been retained.

- TDS/TCS rules remain complex; for example, TDS on partner’s salary, interest, drawings in partnership firms is retained, which leads to practical difficulties (many firms lack TAN, etc.).

2. Refunds, late filing, fairness issues

- No mandatory timelines for disposal of appeals / grievance petitions or revisional orders by the authorities. Delays in timely disposal continue to be pardoned.

- Provisions for exemption from liability to pay interest for the period where the disposal of appeals are delayed by any appellate authority, including the courts.

3. Uneven treatment, inequity, mismatch of incentives

- Savings-/investment-friendly incentives have not been significantly strengthened; some observers think the new tax regime doesn’t sufficiently reward long-term savings or investment relative to old regime obligations or expectations.

- Marginal relief under the Old Tax Regime (OTR) is less favourable compared to the New Tax Regime (NTR) in some respects, which may push taxpayers into making choices that are sub-optimal for their financial planning.

4. Privacy, oversight and risk of overreach

- The moulding of digital / algorithmic / data-driven triggers for reassessment and compliance is stronger in the 2025 Act but are not backed by the procedural safeguards, definitions, limits, oversight mechanisms; these are not sufficiently built in. This raises risks of arbitrary or heavy-handed action.

5. Lack of clarity / roadmap in implementation

- Though the law reduces sections, changes language etc., actual implementation (IT systems, staffing, training, taxpayer interface, etc.) might lag. Observers worry about capacity to handle digital records, data matching, appeals.

- Transition rules (for those who have made long-term commitments under the old law, or whose income/assets fall across regimes) could have been more clearly spelt out.

6. Missed opportunity in broadening tax base / reducing exemptions

- Though the law claims simplification, many exemptions, deductions, overlapping rules remain. Some think the tax base hasn’t been meaningfully broadened in certain areas (like real estate, informal receipts, etc.).

- More progressive changes in rates or rebalancing burden could have been considered, especially as inflation erodes real thresholds. Tax slabs etc., still leave some taxpayers in discomfort.

7. Support for smaller firms / MSMEs / those with low capacity

- Many of data requirements, reporting, TDS, digital obligations impose fixed overheads. Small businesses, partners without formal structures etc. find compliance burdens high relative to their capacity. Observers feel more relief provisions or simplified rules for such groups could have been included.

8. Transparency, legislative oversight

- Some key provisions (like faceless assessments / appeals etc.) are moved to be governed by rules rather than being embedded in the law itself. This gives administrative flexibility, but reduces parliamentary visibility and makes redress harder.

The temptation to suggest what could have been done differently is irresistible; suggestions that may pave way for additional reforms. Some of them are;

- Stronger deadlines mandating fixed timelines for every stage: issuance of notices, disposal of appeals by CIT (Appeals) and ITAT; grievance/redressal mechanisms; timeline for refunds etc.

- Procedural fairness by ensuring the automatic stay of demands / assessments where appeals or rectification petitions are pending, to reduce hardship.

- Wider margin of relief / incentives for savings and investments or simplified exemptions for retirement savings, health insurance, education etc., especially in the new regime. Possibly rebalancing marginal relief to make old regime less penalising for those with existing obligations.

- Simplified regime for small businesses / partnerships including the presumptive taxation and lighter reporting (less frequent TDS / less frequent returns) for small firms or partners.

- Removal or postponement of the TDS obligations that create cash flow burdens (e.g. on partner salaries or drawings) especially where profit is uncertain.

- Greater clarity on data / digital enforcement / rights by defining the safe harbour thresholds and introducing the de minimis rules for “unexplained income / assets / credits” so ordinary informal transactions aren’t penalised.

- Stronger privacy protections and oversight for use of personal / digital data.

- Meaningful expansion of the tax base by outreach to a good part of the population by covering the informal sectors, digital / gig economy more comprehensively.

- Introducing transparency in the effective rate of taxation by pruning and consolidating the provisions for exemptions/deductions more aggressively.

- Auto Indexation of thresholds, rates, etc. to adjust for inflation, cost of living etc. so that taxpayers are not pushed into higher tax brackets simply due to inflation rather than real income growth.

- Transitional clarity, especially for those with investments, deductions etc under the old Act.

- Continuity of harmless clauses for some years for minimising the disputes arising from overlapping rules.

- Greater legislative embedding of taxpayer rights by including more rights of taxpayers (Taxpayer Charter) in the main body, not just in rules.

- Ensuring transparency in reopening, reassessment, and appeal (for example, reasons to be stated, officer escalations etc.).

- Continuous review mechanism that involves periodic review of the law, say every few years, involving stakeholders, to identify parts that are still overly burdensome or have led to disputes.

- Mechanism for better feedback and active public consultation and solicitation at the pre-legislative stage. An exercise should be carried out to measure the effect of the legal and economic effect and the counter-productive consequences of the Act for posterity.

Putting it all together, yes, there was a strong case for the enactment of the new law, it could have been much more transformative. Many observers feel that the legislature missed a great opportunity to really reform the income-tax law in preference for presenting the old wine in a new bottle; may be there was a lack of will or the courage to take the bull by its horns or was it the tacit acceptance that the law of income tax is beyond simplification? The government took a cautious path, balancing simplification with retaining significant legacy structures, possibly to avoid revenue risk or political backlash. The law improves readability, removes redundant parts, modernises in parts, these are all commendable, but many classic pain points remain. A tax administration which disposes of appeals promptly and reaches a fair and final settlement speedily, is itself to be classed as a tax incentive. But: it’s not fair to say the Act is a failure; it achieves many important reforms and is likely to reduce compliance costs and increase clarity.

The Act has achieved simplicity, readability. cohesiveness, lesser verbosity, modernity, some best global practices and removal of archaic provisions, has missed the structural issues like TDS complexity, refund fairness generally, appeals delays, taxpayers’ rights, MSME reliefs, automatic indexation of slabs with the passage of time. Some of the long-standing issues that cause taxpayers anxiety or litigation remained unaddressed or only partially addressed. Importantly the absence of clarity in the transitional provisions leaves a high potential source of disputes. In essence the Act is a step forward in form and readability, but not a game-changer in substance.

The Act’s strengths lie in modern language, logical regrouping of provisions, and an explicit intention to address digital economy issues and reduce routine litigation. It is a long-needed structural reform that aligns statute design with 21st century record-keeping and digital reporting.

Risks remain in drafting gaps, transitional complexity, and the speed at which administrative guidance will be issued. Simplification of language does not automatically ensure simplification of outcome; poor transitional drafting or omissions create new ambiguity and litigation.

Practitioners should act now to: map exposures, check transitional rules for each client, engage with the tax department’s FAQs and circulars, and prepare to litigate strategic issues if administrative clarification is delayed. The next 24 months will determine whether the Act delivers the promised reduction in disputes or simply reshuffles controversies.