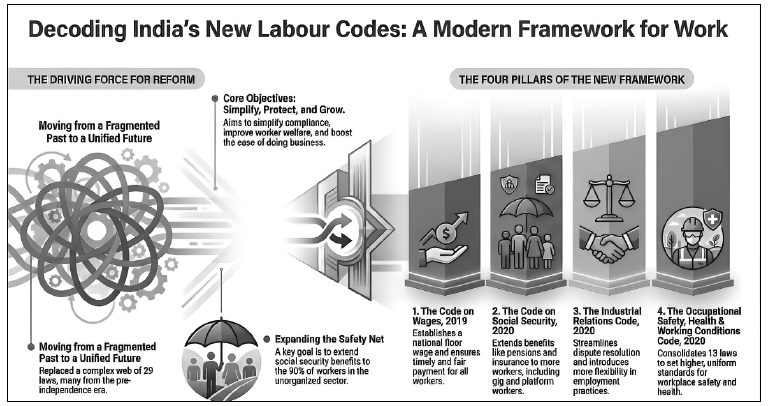

India’s four Labour Codes—the Code on Wages, 2019, the Industrial Relations Code, 2020, the Code on Social Security, 2020, and the Occupational Safety, Health and Working Conditions (OSH) Code, 2020—seek to consolidate 29 central labour laws into a unified framework governing wages, industrial relations, social security and workplace safety. The Codes have been passed and notified, but are yet to be brought into force; implementation will follow separate commencement notifications, and recent policy statements indicate an intention to make them fully operational from 1 April 2026, after re-publication and finalisation of rules by the Centre and States.

The reforms introduce several cross cutting features: a uniform definition of “wages” with a 50% cap on specified exclusions; broader definitions of “worker” and “employee”; an inspector cum facilitator regime; digitisation of registers and returns through portals such as Shram Suvidha; and a common licensing framework, particularly relevant for contract labour and inter State migrant work. At the Code specific level, key changes include a statutory floor wage and universalised wage coverage, expanded social security to gig and platform workers funded partly by aggregator contributions, higher thresholds for prior permission on lay off and closure and for standing orders, recognition of a sole negotiating union with 51% membership, rationalised applicability thresholds under the OSH Code, and formal recognition of fixed term employment.

For professionals, three areas deserve immediate attention: restructuring of CTCs and payroll systems around the new wage definition; re assessment of contract labour and outsourcing strategies in light of new thresholds and licensing; and readiness for digital compliance and transitional issues once commencement notifications are issued. The Codes have the potential to ease doing business and extend social protection, but their success will depend on state-level rule-making, administrative capacity, and how stakeholders navigate the trade offs between flexibility and security.

1. INTRODUCTION

For decades, India’s labour law landscape has been characterised by a dense web of central and state statutes, many with overlapping subject matter, conflicting definitions and dated assumptions about the nature of work. Employers have struggled with fragmented compliance and multiple inspections, while a large majority of the workforce, especially in the unorganised and informal sectors, has remained outside effective social security coverage.

The four Labour Codes are designed to move from a purely regulatory mindset to a facilitative, risk-based framework, recognising contemporary forms of work such as platform work and fixed-term employment. All four Codes have received Presidential assent and stand notified in the Gazette, but they will come into force only on dates to be appointed by separate notifications under the respective commencement provisions. Recent ministerial statements and press releases indicate that the government’s present plan is to make the Codes fully operational from 1 April 2026, aligning with the financial year and allowing time to finalise central and state rules.

The principal reason for the delay has been the federal nature of labour as a Concurrent List subject: the Centre must frame rules on matters within its ambit, while States and Union Territories must frame their own rules where empowered. As of late 2025, most States and UTs have pre-published draft rules under some or all of the Codes, but a small number still lag behind, and several jurisdictions are revisiting their drafts in light of stakeholder feedback. This staggered readiness explains why commencement has been repeatedly deferred, despite the Codes having been passed in 2019–2020.

2. KEY THEMES CUTTING ACROSS ALL CODES

Broader definitions of “worker” and “employee.”

Across the Codes, the definitions of “worker” and “employee” are significantly broader than in many legacy statutes, generally covering persons employed in any industry to do manual, unskilled, skilled, technical, operational, clerical or supervisory work, subject to specified wage ceilings for certain categories. This enlarged coverage is particularly relevant for supervisory and middle management layers that were previously excluded under some laws by virtue of salary thresholds or nature of duties tests.

For advisory and litigation practice, this implies that classification disputes may shift from the question of “workman versus non-workman” to the precise application of statutory exclusions and state-specific rules. Employers will need to revisit designation structures and job descriptions to ensure they align with the new definitions.

Uniform definition of “wages” and the 50% rule

Perhaps the single most consequential reform is the adoption of a uniform definition of “wages” across all four Codes. While details differ slightly between Codes, the core construct is common: wages include basic pay and dearness allowance and specified components, while certain allowances and benefits are expressly excluded; however, if the aggregate value of such exclusions exceeds 50% of total remuneration, the excess is deemed to form part of wages.

This “50% rule” directly affects calculations for provident fund, gratuity, bonus, retrenchment compensation and other wage-linked benefits, substantially limiting the scope to depress contribution-bearing wage elements by inflating allowances. For many Indian CTC structures—traditionally built around a relatively low “basic + DA” portion with multiple allowances—this will translate into higher long-term social security costs, lower immediate take-home for employees, and a need for complete redesign of salary templates.

Inspector cum facilitator and digitisation

All four Codes envisage a shift from the conventional “Inspector Raj” to an inspector cum facilitator model, emphasising guidance and graded enforcement before prosecution in many situations. Inspection schemes are to be computerised and risk based, with provisions for web based scheduling, random selection and online submission of documents.

Digitisation is a central theme: electronic registers, e returns and online licences are encouraged or mandated, with the Shram Suvidha portal and linked systems expected to play a central role in unified filings. While larger enterprises may find this consistent with existing HRIS/ERP practices, smaller establishments will need to build digital competencies and address issues such as data accuracy, security and document retention.

Common licensing and single registration

The Codes introduce a move towards common licensing, particularly for contractors and staffing entities, and single registration for establishments covered by the OSH provisions. Instead of multiple location specific licences under different Acts (for example, separate contract labour licences for individual sites), a single licence may cover multiple establishments, subject to prescribed conditions.

Similarly, the OSH Code enables one registration for an establishment carrying on more than one activity that would previously have required distinct registrations (such as factory, motor transport and contract labour). This is intended to simplify compliance and make growth across locations easier, but also raises the bar for centralised compliance management within organisations.

3. THE CODE ON WAGES, 2019

Consolidation and coverage

The Code on Wages consolidates four key enactments: the Payment of Wages Act, the Minimum Wages Act, the Payment of Bonus Act and the Equal Remuneration Act. A significant change is that the Code applies to all employees across all sectors for its wage related provisions, moving away from the earlier concept of “scheduled employments” under the Minimum Wages Act.

This universalisation reduces fragmentation and makes it easier to understand wage obligations vis à vis different categories of employees; however, detailed state specific minimum wages and rules will still require careful attention by employers with multi state operations.

National floor wage and minimum wage

The Wage Code introduces a statutory national floor wage to be fixed by the Central Government, taking into account factors such as living standards and geographical differences. States will continue to fix minimum wages for different skill levels and industries, but cannot set them below the notified floor wage.

The distinction between the central floor wage and state minimum wages is important in advisory work, especially when analysing cross border wage disparities and potential relocations of labour intensive activities. The floor wage is intended to reduce extreme regional differentials while allowing states to respond to local cost of living conditions.

Wage definition, overtime and payment modes

Under the Wage Code, the uniform wage definition and 50% cap on exclusions determine the base for overtime, bonus and other wage linked entitlements. Overtime pay must be at least double the normal rate of wages, requiring payroll systems to correctly compute overtime on the statutory wage base, including any deemed additions under the 50% rule.

The Code also rationalises wage periods, prescribes time limits for payment, and clarifies permissible deductions, while facilitating digital payment modes and electronic record keeping. This aligns wage practice with broader financial inclusion and digitisation policies.

Impact on CTC structuring

From a practitioner’s standpoint, the 50% rule is the central driver of CTC impact under the Wage Code. Employers must map each pay component to either the “wage” or “exclusion” bucket, simulate the impact on provident fund, gratuity and other benefits, and consider re balancing fixed and variable pay.

In many cases, the employer’s cost of compliance will rise because contribution-bearing wages will effectively increase, even if the total CTC remains unchanged. Employees may initially perceive a reduction in take-home salary due to higher statutory deductions, but the long-term benefit accrual in PF and gratuity will be more robust. Transparent communication and change management will therefore be critical.

4. THE CODE ON SOCIAL SECURITY, 2020

Consolidation and scheme architecture

The Code on Social Security, 2020 consolidates nine central labour Acts into a single statute. Those Acts are:

- The Employees’ Compensation Act, 1923

- The Employees’ State Insurance Act, 1948

- The Employees’ Provident Funds and Miscellaneous Provisions Act, 1952

- The Employment Exchanges (Compulsory Notification of Vacancies) Act, 1959

- The Maternity Benefit Act, 1961

- The Payment of Gratuity Act, 1972

- The Cine Workers Welfare Fund Act, 1981

- The Building and Other Construction Workers’ Welfare Cess Act, 1996

- The Unorganised Workers’ Social Security Act, 2008

The Code enables the Central Government to frame schemes for different classes of persons, with institutions such as the National Social Security Board advising on schemes for unorganised, gig and platform workers. The effectiveness of this architecture will ultimately depend on how schemes are designed and funded, and on the capacity of implementing agencies.

Gig and platform workers – registration and aggregator contributions

A path-breaking feature is the explicit recognition of “gig workers” and “platform workers”, who are often engaged as independent contractors and were largely outside traditional social security statutes. The Code contemplates mandatory registration of unorganised, gig and platform workers on a designated portal, typically using Aadhaar-based identity, as a precondition to claim benefits under the relevant schemes.

Aggregators—such as ride-hailing companies, food delivery platforms and similar digital intermediaries—are required to contribute a notified percentage of their annual turnover, within a statutory band, subject to an overall cap as a proportion of the amounts payable to such workers. These contributions, along with government funding and worker co contributions where prescribed, will form the corpus for benefits like accident insurance, health cover and old age support. From a tax and advisory perspective, this will influence pricing, margin structures and the design of platform contracts.

Aadhaar linkage and unorganised sector schemes

The Code provides for Aadhaar based identification in accessing benefits, and in practice Aadhaar linkage is expected to be embedded in registration and claim processes. This can reduce duplication and leakages but may pose inclusion challenges for workers lacking robust documentation or digital literacy, especially in remote areas.

For the unorganised sector more generally, the Code contemplates schemes on health, maternity, disability, old age and other contingencies, to be implemented through existing and new institutions. The key compliance question for employers will be the extent to which they are treated as “aggregators” or “principal employers” under different schemes and rules, especially in complex supply chains.

Gratuity and fixed term employment

The Social Security Code introduces important changes in gratuity eligibility for fixed term employees, aligning it with their actual period of service rather than the earlier five year continuous service requirement. Fixed term employees will be entitled to gratuity on a pro rata basis if they complete one year of service, improving benefit equity compared to permanent workers.

This interacts with the IR Code’s formal recognition of fixed term employment and will influence contract structuring, costing and actuarial valuations. Employers will need to review their gratuity funding policies and consider the volatility introduced by larger numbers of shorter tenure employees becoming eligible for gratuity.

5. THE INDUSTRIAL RELATIONS CODE, 2020

Consolidation and recognition of trade unions

The Industrial Relations Code consolidates the Trade Unions Act, Industrial Employment (Standing Orders) Act and Industrial Disputes Act into a unified regime for trade union registration, standing orders and dispute resolution. One of its most significant changes is the formal recognition framework for negotiating unions.

Where a trade union has at least 51% of workers in an industrial establishment as members, it must be recognised as the sole negotiating union. If no union meets this threshold, a negotiating council is constituted comprising representatives of unions with at least 20% membership, ensuring that collective bargaining is channelled through a defined structure. This reduces multiplicity at the bargaining table but may intensify inter union competition to reach the 51% mark.

Thresholds for lay off, retrenchment and closure

The IR Code raises the threshold at which prior government permission is required for lay off, retrenchment and closure in certain industrial establishments from 100 to 300 workers. Establishments below this threshold may proceed without prior permission, subject to compliance with notice, compensation and other procedural safeguards.

The threshold for mandatory standing orders is also increased from 100 to 300 workers. These changes are aimed at providing mid sized enterprises and MSMEs with greater flexibility to respond to market conditions, but unions view them as weakening job security. In practice, states may exercise their power to further increase the threshold, leading to some jurisdictional variation.

Fixed term employment and unfair labour practices

The IR Code formally recognises fixed term employment, requiring that fixed term employees receive the same wages and benefits as permanent workers doing similar work, including eligibility for gratuity on a pro rata basis under the Social Security Code. This provides a lawful alternative to prolonged contractual arrangements with less clarity on rights and obligations.

The Code also consolidates and clarifies lists of unfair labour practices attributable to employers and workers, modernising the grounds for complaint and enforcement. This will be particularly relevant in adjudication and conciliation proceedings under the new regime.

Regulation of strikes and lock outs

A major change is the extension of the requirement of 14 days’ prior notice for strikes (and lock outs) from public utility services to all industrial establishments. Strikes and lock outs are also prohibited during conciliation proceedings and for prescribed cooling periods thereafter, and an expanded definition of “strike” can cover concerted mass casual leave above a set threshold.

From an employer’s standpoint, these provisions offer greater predictability and time to engage in negotiation or contingency planning. Unions argue that the combination of higher thresholds for retrenchment permissions and tighter strike conditions constrains collective bargaining leverage.

6. THE OCCUPATIONAL SAFETY, HEALTH AND WORKING CONDITIONS CODE, 2020 (OSH CODE, 2020)

Consolidation and applicability thresholds

The OSH Code consolidates 13 enactments relating to occupational safety, health and working conditions, including the Factories Act, Mines Act, Contract Labour Act and others. A key policy objective is to rationalise applicability thresholds, especially for smaller establishments, while maintaining safety oversight in higher-risk environments.

For factories, the threshold is raised to 20 workers where power is used and 40 workers where power is not used, compared with the earlier 10 and 20, respectively. For contract labour, the applicability threshold increases from 20 workers to 50 workers. These changes may relieve very small units from some regulatory burdens, but at the same time call for more robust self-regulation where statutory coverage does apply.

Single registration and duties of employers and workers

The OSH Code provides for single registration for an establishment, covering multiple activities which were previously subject to separate registrations. It also codifies duties of employers, employees and other persons, including obligations relating to safe premises, risk assessments, medical examinations, safety committees and reporting of accidents and dangerous occurrences.

Women are explicitly permitted to work in all establishments, including at night, subject to their consent and compliance with prescribed safety conditions and facilities. This aligns with broader gender equality policies but requires employers to plan carefully for transport, security and workplace design issues for night shift operations.

7. SELECTED COMPARATIVE TABLES

Old–new parameters

| Parameter |

Earlier framework (illustrative) |

Position under Codes |

| Wage definition |

Multiple definitions in EPF, ESI, MW, Bonus. |

Uniform definition with 50% cap on exclusions. |

| National floor wage |

No binding statutory floor; advisory concept. |

Statutory floor wage by Centre; States’ minima cannot go below. |

| Lay off/closure permission |

Prior permission from 100 workmen onwards. |

Threshold raised to 300 workmen; states may enhance. |

| Standing orders |

Applicable from 100 workmen. |

Applicable from 300 workers. |

| Contract labour applicability |

From 20 contract workers. |

From 50 contract workers under OSH Code. |

| Gig/platform workers |

Not recognised. |

Recognised with aggregator contribution obligations. |

| Limitations for wage claims |

Varied/long limitation periods. |

Harmonised (e.g., three years under the Wage Code). |

| Inspection model |

Inspector-driven, often discretionary. |

Risk-based inspector cum facilitator with e systems. |

ILLUSTRATIVE OSH APPLICABILITY THRESHOLDS

| Establishment type |

Earlier threshold |

OSH Code threshold |

| Factory (with power) |

10 or more workers. |

20 or more workers. |

| Factory (without power) |

20 or more workers. |

40 or more workers. |

| Contract labour |

20 or more contract workers. |

50 or more contract workers. |

8. IMPACT AND CRITICAL VIEWPOINTS

Employer and HR perspective

From an employer’s perspective, the Codes simultaneously offer simplification and introduce new cost and capability burdens. On the one hand, higher thresholds for lay off permissions and standing orders, common licensing and digital filings can materially improve ease of doing business, particularly for MSMEs and multi-location enterprises. On the other hand, the 50% wage rule, aggregator contributions for gig workers and expanded gratuity coverage will increase statutory outgo in many cases and demand significant changes to HR, payroll and compliance systems.

Administrative readiness is a further concern: employers will have to navigate overlapping regimes during transition, manage contractual amendments, and align internal policies with central and state rules that may not be perfectly harmonised at the outset. Early years of implementation can be expected to see interpretative disputes and litigation around definitions, thresholds and the interaction between central Codes and state rules.

WORKER AND UNION PERSPECTIVE

Trade unions have welcomed the promise of wider social security coverage but remain sceptical of higher thresholds for prior permission on retrenchment and closure, and of tighter strike notice and prohibition provisions. There is concern that flexibility on fixed term employment, coupled with reduced state control over closures in mid sized units, may encourage increased use of short term contracts and weaken job security.

For workers in the gig and unorganised sectors, the Codes create a statutory framework for social security where none existed earlier, but the real test will lie in the design and funding of schemes, ease of registration and claim processes, and the capacity of institutions to reach highly dispersed and mobile worker populations.

Administrative and system readiness

Regulators face their own readiness challenges: creating interoperable digital systems (such as upgraded Shram Suvidha type platforms), training inspector cum facilitators, issuing clear guidance circulars, and ensuring consistent interpretations across regions. The multilingual publication of rules and the development of user friendly interfaces for small employers and workers will be critical to genuine inclusiveness.

These factors, together with ongoing state level rule making, help explain why commencement has been calibrated and repeatedly deferred, and why a synchronised 1 April 2026 roll out is being projected as the current target.

9. CONCLUSION – READINESS ROADMAP FOR PROFESSIONALS

The four Labour Codes represent one of the most far reaching overhauls of India’s labour regulatory framework since independence, with the potential to simplify compliance, enhance formalisation and extend social security coverage. Whether this potential is realised will depend on the quality and timeliness of rule making, the robustness of digital infrastructure, and how employers, workers and regulators adapt in practice.

For professionals, the immediate action agendabefore the anticipated 1 April 2026 commencement includes:

- Conducting detailed impact assessments on CTC, PF and gratuity under the new wage definition.

- Reviewing contract labour, outsourcing and fixed term employment strategies in light of new thresholds and licensing norms.

- Upgrading HR, payroll and compliance systems for digital registers, returns and interaction with central and state portals.

- Tracking state wise rule making and tailoring advice and internal policies to jurisdiction specific requirements.

- Training HR, IR and finance teams on the substantive changes, especially around gig worker contributions, recognition of unions and OSH thresholds.

If these steps are taken proactively, the transition to the new regime can be managed with reduced disruption, allowing businesses to focus on core operations while supporting a more formal, secure and transparent labour market over the next decade.