BCAS President CA Zubin Billimoria’s Message for the Month of June 2026

My Dear BCAS Family,

As I begin to pen my thoughts, Mumbai and many parts of the country are experiencing unusual heat, with temperatures frequently breaching normal ranges. Further, by the time the issue reaches you, the monsoon season will also be underway in many parts of India. Recent reports by the Indian Meteorological Department indicate that the El Niño effect will reduce monsoon winds in 2026, raising the possibility of a below-normal monsoon in several areas. All this is part of the broader global phenomenon of climate change, which manifests in several other forms, such as retreating glaciers, melting snow, and rising sea levels.

Accordingly, climate change is no longer an environmental concern to be debated in scientific journals and conferences, but a defining economic, social, and governance challenge. Its implications extend far beyond rising temperatures and extreme weather events; it is fundamentally reshaping the way businesses operate, governments regulate, and professionals deliver value.

This has made me reflect on the theme of climate change and its impact on professionals and institutions like ours.

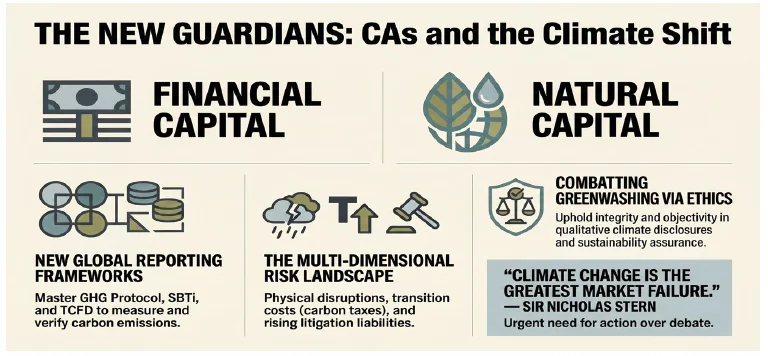

IMPACT ON PROFESSIONALS

As CAs, our domain expertise has traditionally been in financial reporting, coupled with ethics and integrity. Climate change has expanded our roles from guardians of financial capital to guardians of natural capital, which encompasses environmental, social, and governance (ESG) dimensions. This has broadened our roles and responsibilities in several areas as follows:

NEW REPORTING FRAMEWORKS

Several specialised global reporting frameworks, commonly referred to as Carbon Accounting Frameworks, that help measure, report, and verify greenhouse gas emissions have recently emerged, each dealing with specific aspects. A few of the commonly used frameworks are as follows:

- GHG Protocol, which deals with measuring and reporting of Scope 1, 2 and 3 emissions

- Science-Based Targets Initiative (SBTi) helps in quantifying how much CO2 the world can continue to emit to limit the global temperature increase to within 1.5 degrees centigrade and scientifically lays specific sector and company-level targets with respect to this.

- Task Force on Climate-Related Financial Disclosures (TCFD), which focuses on climate risk disclosures in the financial statements.

Closer home, SEBI’s BRSR framework also captures these and several other aspects. All this will require continuous upskilling and a deeper understanding of interdisciplinary domains such as environmental science, policy frameworks, and sustainability metrics, which would need disclosure and corresponding assurance from professionals.

Changing Risk Landscape and Consequential Reporting and Accounting Challenges

Climate change introduces a multi-dimensional risk framework that directly affects financial statements, assurance processes, and corporate disclosures. For professionals, the complexity lies not merely in identifying these risks but in translating them into measurable, reportable, and auditable financial impacts. The important risk categories and the consequential accounting and reporting challenges are briefly identified as follows:

Physical Risks:

These arise from acute and chronic climate events, such as extreme weather disrupting operations and supply chains, damage to property, plant, and equipment, and increased insurance costs. Consequently, these affect asset impairment, changes in the useful lives of fixed assets, increased provisions for restoration costs, and additional contingent liabilities.

Transition Risks:

These arise from a shift toward a low-carbon economy, with resultant regulatory changes such as carbon taxes and emission caps, technological obsolescence due to equipment changes to enable controlled emission generation, and market shifts in consumer preferences. These can result in accelerated depreciation, reassessment of investment viability and fair value adjustments.

Litigation Risks:

These arise from organisations facing increasing claims due to regulatory non-compliance with pollution and emissions norms, as well as claims related to environmental damage, resulting in higher provisioning, additional legal costs, and higher contingent liabilities.

IMPACT ON CORPORATE STRATEGY

Climate change has direct implications for professionals advising organisations on capital allocation decisions, as sustainability goals increasingly influence these. Also, the risk management framework must incorporate climate scenarios. Further, performance metrics are evolving to include non-financial indicators, and, finally, stakeholder expectations are shifting toward sustainable enterprises, as they perceive them as long-term value creators. As professionals, we will have to ensure that climate considerations are increasingly integrated into decision-making processes.

ETHICAL CONSIDERATIONS

Beyond technical competencies, climate change presents several ethical dimensions and challenges. As trusted advisors, we must uphold integrity in disclosures, objectivity in our assurance engagements, given the significant qualitative judgment involved, and a commitment to the public interest. Finally, we must guard against greenwashing claims.

BCAS’ ROLE

I see BCAS playing a pivotal role in the coming years to shape the profession’s response to climate change in several ways as follows:

- Education and Capacity Building: We will strive to introduce structured learning programmes through the BCAS Academy platform. These will be useful for practitioners at every stage of their careers.

- Technical Guidance: We will work towards developing appropriate publications to assist practitioners in navigating the complexities of BRSR assurance and related areas

- Thought Leadership and Advocacy: BCAS will endeavour to contribute to national policy conversations around sustainable finance and accounting standards. Our voice must be heard in shaping frameworks that are practical, credible, and appropriate.

- Green Operations: Being an ISO-compliant organisation, we will endeavour to examine our own organisational footprint in terms of energy usage, paper consumption, and travel, thereby setting an example in sustainable and responsible institutional behaviour.

TIME FOR ACTION OVER DEBATE

To conclude, I would like to refer to a quote by Sir Nicholas Stern in the magazine, The Stern Review on Economics of Climate Change, way back in 2006, which validates that climate change is no longer just an environmental issue but a defining economic and government challenge, which needs action rather than just debate.

“Climate change is the greatest market failure the world has ever seen”

A big thank you to one and all!