1. A Day of Divine Wisdom at BCAS

We were deeply honored to welcome His Holiness Shri Kanchi Kamakoti Peetadhipati Jagadguru Pujyashri Shankara Vijayendra Saraswati Shankaracharya Swamiji to the BCAS Hall, Churchgate, on 9th April 2026

The atmosphere was one of profound serenity as Swamiji arrived, gracing us with his presence and a message of timeless wisdom. The event was attended by the Office Bearers, Past Presidents, members of the managing committee and BCAS Staff members.

BCAS recorded a podcast —”Samvaad with BCAS” with His Holiness on the topic: “Culture – Foundation for Strong India | Sanskriti – Majboot Bharat ki Neev” which was anchored by CA Mihir Sheth, Past President of BCAS.

During his visit, His Holiness appreciated the institution’s ongoing efforts in delivering meaningful services and contributing to societal development. He acknowledged the role of such initiatives in strengthening national values and outreach across communities.

BCAS is humbled to share the remarks penned by His Holiness Pujya Shri Shankara Vijayendra Saraswati Swamiji during his visit on 9th April 2026:

“Visit to this institution, which catalyses economic growth through useful audit & account services, has been revealing & highly satisfying. Your contribution to the sustained growth of the nation, reaching out the gains of democracy to all sections of society, even in deep hinterlands, is commendable. National policies cannot lose sight of the basic dharmic characteristics of our nation. You have been following that path towards Viksit Bharat. Blessings & Prayers for continued good work. Jaya Jaya Shankara. Hara Hara Shankara”.

BCAS was also honoured to support the DHARMAM CHARA event held at the BSE Convention Hall on 7th April 2026 under the auspicious presence of His Holiness. President of BCAS CA Zubin Billimoria, and Vice President, CA Kinjal Shah, were felicitated at the event.

We are grateful for His blessings and encouragement as we continue our journey of service and impact.

2. Finance, Corporate & Allied Laws Study Circle – Recent Developments in Labour Laws: An Auditor’s Perspective held on Friday, 03rd April, 2026 @ Virtual

In this virtual session Mr. Pankaj Savla deliberated on the evolving landscape of labour laws and their implications for auditors. The session covered key regulatory changes and their impact on compliance and audit procedures. Emphasis was laid on understanding the practical challenges faced while auditing labour law compliance.

The speaker highlighted critical areas requiring due diligence, including verification of statutory records and adherence to updated provisions. Insights were shared on identifying compliance gaps and mitigating associated risks. The session also addressed documentation and reporting considerations from an auditor’s standpoint. Participants gained clarity on the auditor’s role in ensuring compliance with applicable labour regulations. The discussion provided practical perspectives and enhanced awareness of recent developments in labour laws. A total of 39 participants attended the session via Zoom.

3. FEMA Study Circle -“Amended ECB Regulations, 2026,” held on 27th March 2026@ Virtual.

In this session, the participants discussed the revised ECB Framework announced for 2026, focusing on regulatory changes and compliance obligations. The session gave clarity on end-use restrictions, eligibility of borrowers and lenders, maturity period, pricing, reporting and various other critical aspects. The meeting was chaired by CA Natwar Thakrar and led by group leader CA Parth Panchal.

Overview of the session

The Chairman opened with an overview of the core and policy-level reforms. The group leader proceeded to explain the amendments in each segment of the new framework, offering a thorough analysis that mapped the amended text with the erstwhile framework, draft regulations circulated for public comments, and RBI clarifications. The deliberations focused on how these changes will reshape the ECB environment in India.

Key areas discussed

- Scope and Impact Area of the New Framework outlining the broad framework of the Borrowing and Lending regulations, the scope of the new framework and then discussing how it would impact the nature of transactions.

- End Use Restrictions dealing with widened permissible end uses and what continues to be restricted end-use in the new framework. It covered various nuances and practical scenarios having a critical impact.

- Eligible Borrowers and Lenders as to how their expanded base would impact the structuring choices.

- Pricing, Maturity, and Borrowing Limit emphasizing how pricing caps, maturity rules and borrowing limits would impact the industry, and the practical challenges over ECB pricing that would be faced in the amended framework. Key pricing norms, minimum average maturity thresholds, and borrowing limits were explained.

- Procedure and Reporting detailing the reporting obligations to the Reserve Bank of India and the Authorized Dealer banks, timelines for filing Form ECB and related returns.

- Other amendments in ECB regulations capturing the other amendments to ECB regulations, which would also need to be taken care of going forward.

The participants also analysed and focused on the changes on borrowing and lending transactions between resident and non-resident individuals, which are brought as part of the Borrowing and Lending Regulations. The meeting was interactive and detail-oriented, with participants raising specific scenarios seeking practical insights on implementing the 2026 ECB Framework.

4. Indirect Tax Laws Study Circle Meeting on “GST Issues in the Entertainment Industry” held on Tuesday, 24th March 2026 @ Virtual.

The session was led by CA. Mansi Shah (Group Leader) under the mentorship of CA. Rajiv Luthia (Mentor), and witnessed active participation from members across the fraternity.

The presentation covered the following aspects for a detailed discussion:

- Production Stage Complexities

Analysis of nature of supply and place of supply in multi-location shoots, including classification of temporary sets and renting of immovable property. - Input Tax Credit (ITC) Challenges

Detailed examination of ITC eligibility on items such as scrapped vehicles, aircraft hiring, and logistics arrangements—highlighting the nuances of blocked credits under Section 17(5). - Cross-Border Transactions

Taxability of overseas line producers, reverse charge implications, and valuation issues including treatment of reimbursements and “pure agent” conditions. - Post-Production Services

GST implications on international VFX and editing services, emphasizing place of supply provisions under Section 13 of the IGST Act. - OTT & Export of Services

Key insights on export qualification in OTT transactions, addressing concerns around permanent establishment and recipient determination - Movie Rights & Tax Treatment

Classification of permanent transfer of movie rights as goods, treatment of milestone-based payments, and timing of tax liability. - Industry-Specific Classification Issues

Discussion on printing services on PVC material and composite supplies in hospitality-linked entertainment events.

Around 73 participants from all over India benefited while taking an active part in the discussion. Participants appreciated the efforts of the group leader and the mentor.

5. Felicitation of Chartered Accountancy pass-outs of the January 2026 Batch held on Friday, 13th March 2026 at Sydenham College of Commerce & Economics, Churchgate, Mumbai.

The Seminar, Membership and Public Relations (SMPR) Committee hosted a felicitation ceremony to honour the newly qualified Chartered Accountants from the January 2026 batch. Over 180 enthusiastic newly qualified CAs participated in the event including CA Sidhh Furiya, who secured AIR 38. The guest and mentor for the event was CA Samit Saraf, Managing Committee member of BCAS. In his address, he reminisced about his post-qualification journey and shared with the attendees 10 cheat codes that helped him propel his career in the right direction and which could help them too. He also expressed gratitude for his association with BCAS and encouraged the new CAs to consider joining BCAS and its activities.

The ceremony served as a warm welcome for the newly qualified CAs into the wider professional fraternity.

6. Seminar on TDS & TCS – What It Is, What Changes, & How to Stay Compliance-Ready jointly with Goa Chamber of Commerce & Industry (GCCI) held on 13th March 2026@ Hybrid.

The Direct Tax Committee of BCAS, jointly with the Goa Chamber of Commerce and Industry, organised a full-day seminar at GCCI Hall, Goa and in virtual mode to cover the TDS provisions under the new Income Tax Act, 2025, the draft Rules, 2026 and the relevant new Forms. The objective was to familiarise participants with the practical new TDS sections, new Forms, revised due dates, etc.

CA Ronak A Rambhia, shared the new TDS provisions with respect to the threshold amount and the applicable rate of deduction under the Income Tax Act 1961 v/s the new Income Tax Act 2025, which were discussed in depth. The current applicable Forms and the due dates in the current provisions were discussed in comparison with the new applicable Forms and Rules. The practical difficulties on TDS on Payment to Partners u/s 194T of the Income Tax Act, 1961 were discussed in depth with practical scenarios. Further, CA Ravikant Kamath gave his in-depth knowledge on specific new provisions in the Income Tax Act, 2025 and the draft Income Tax Rules, specifically on the chapter of Salary perquisites. He discussed practical TDS controversies for various types of business assesses based on the court rulings, tax provisions, Circulars, etc., by giving his views on these controversies.

Mr. Purushottam from the TDS CPC, Ghaziabad, also presented his views on the new TDS portal 2.0. He gave a walk-through on the upcoming TDS portal, which will include features such as the demand outstanding, payments tab, litigation tab, etc. He also shared how the tax department is preparing for the new Income Tax Act 2025 in practical compliance.

The seminar received an encouraging response from the Goa participants in trade commerce, and also viewers from the online platform. The participants, both online and offline, were enlightened to be ready for the upcoming Tax year 2026-27 for the TDS compliances.

7. Indirect Tax Laws Study Circle Meeting on Issues in Construction Industry and Redevelopment held on Thursday, 05th March 2026 @ Virtual

The session was led by CA. Abhijit Dongaonkar (Group Leader) under the mentorship of CA. Naresh Sheth, and focused on complex, real-life scenarios impacting developers, landowners, and housing societies.

The presentation covered the following aspects for a detailed discussion:

Joint Development Agreements (JDA)

Examination of taxability of Transfer of Development Rights (TDR), revenue-sharing vs. area-sharing models, valuation complexities, and implications of minimum guaranteed consideration.

Time of Supply & Valuation Mechanisms

Insights into deferred tax liability for residential components, immediate taxability for commercial portions, and deemed valuation principles under relevant notifications.

Unsold Inventory & Cancellations

Treatment of unsold units at the time of completion certificate and tax implications of pre- and post-OC cancellations.

Developed Plots & Infrastructure Charges

Clarification on non-taxability of sale of land, taxability of amenities when charged separately, and implications for third-party buyers.

Redevelopment of Housing Societies

Analysis of TDR transactions between societies and developers, construction services to members, and taxability of corpus or hardship funds.

Slum Rehabilitation Projects (SRP)

Discussion on taxability of free rehabilitation flats, valuation of non-monetary consideration in the form of TDR/FSI, and applicability of exemptions.

Around 120 participants from all over India benefited while taking an active part in the discussion. Participants appreciated the efforts of the group leader and the mentor.

8. 14th Residential Study Course on IND AS held on Friday 27th February 2026 to Sunday 01st March 2026 @ The Orchid Hotel Pune.

The Accounting & Auditing Committee organised this Study Course on Ind AS in a residential learning format, enabling intensive technical deliberations and professional interaction. The three-day programme focused on advanced and contemporary Ind AS topics with a strong emphasis on practical application, case studies and current regulatory expectations relevant to preparers, auditors and advisors.

The course commenced with detailed sessions on Ind AS 103 and Ind AS 110, focusing on business combinations, mergers and demergers, covering structuring considerations, accounting complexities and interpretational challenges through case studies. An in-depth session on Related Party Transactions covered Ind AS requirements along with SEBI LODR, Companies Act and tax aspects, highlighting common compliance challenges, documentation expectations and practical issues.

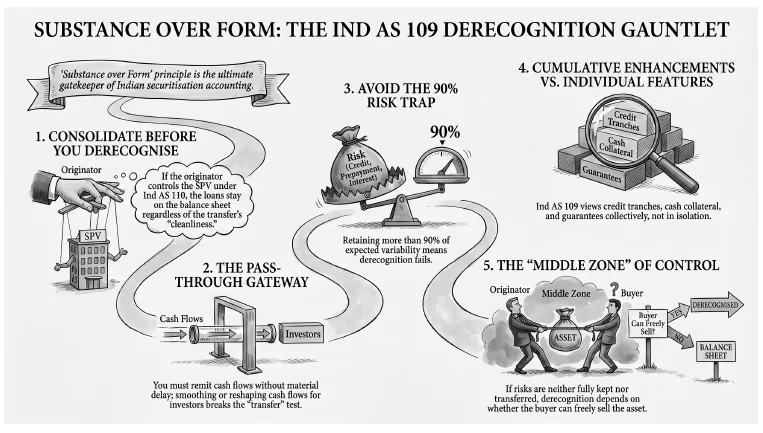

Complex financial instruments were discussed in detail with reference to Ind AS 109, Ind AS 113 and Ind AS 32, covering classification, measurement, valuation and disclosure challenges supported by illustrative case studies. A focused session on Presentation of Financial Statements under Ind AS addressed key presentation principles, disclosure requirements, recent amendments, including Ind AS 118 and emerging reporting practices.

The programme also featured an insightful panel discussion on NFRA findings and initiatives for improving audit quality, deliberating on inspection observations, audit documentation and strengthening audit processes. Another panel discussion on Sustainability Reporting covered preparer and assurance perspectives, addressing evolving sustainability reporting requirements, preparedness challenges and assurance considerations.

The Residential Study Course was well received by participants and provided a valuable platform for deep technical learning, exchange of practical experiences and professional networking. Over 94 participants attended the Course.

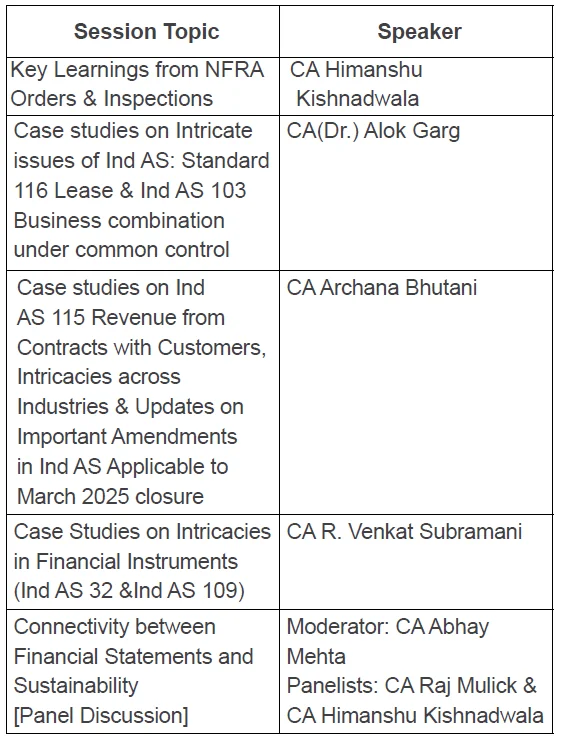

- Faculties for the Residential Study Course:

Dr. CA Anand Banka, CA MP Vijay Kumar, CA Himanshu Kishnadwala, CA Manan Lakhani

Panelists – CA Sudhir Soni CA Amit Mazmudar Moderator- CA Vijay Maniar

Panelists – CA Himanshu Kishnadwala CA Dr Alok Garg Moderator – CA Samit Saraf

9. ITF Study Circle meeting on “International Tax Aspects of Budget 2026 and ITA 2025” (Part 1 & 2) ” held on 10th & 24th February 2026@ Virtual.

The International Tax and Finance Study Circle organized this meeting to discuss amendments in the Budget 2026 on the International Tax aspects. The meeting was divided into 2 parts. Both meetings started with the Chairman of the session, CA Mayur Nayak outlining the amendments along with his comments.

CA Hansh Gangar (Group Leader) took up the various amendments on 10 February 2026. Some key discussion points were:

- Foreign assets of Small Taxpayers – Disclosure Scheme, wherein the group discussed the need and objectives of the amendment, along with the penalty matrix. Some key issues which were discussed were implications of receipt of foreign shares under ESOP, where the assessee was NR or NOR at the time of earning undisclosed income or acquiring undisclosed assets, but is now a resident, but failed to disclose the above, whether he will be covered under the scheme.

- The Group Leader also took us through other amendments, such as Relaxation of conditions relating to prosecution under the Black Money Act, amendments in IFSC, amendments in NDI rules, amendments in TCS rates, etc.

The Budget meeting continued on 24 February 2026, wherein CA Nemin Shah (Group Leader) discussed other amendments that were made in the Budget 2026. Some key discussion points were

- The session opened with introductory remarks from the chairman on his initial views on the determination of residential status.

- Amendment in buyback provisions wherein the Group leader took us through the various changes introduced in buyback taxation over the years. He discussed the meaning of promoter. He highlighted some issues that were discussed with the group at length – Whether the additional income tax will be eligible for treaty benefits, whether deduction under section 54F is available, and whether this provision will apply to foreign buyback.

- Other amendments, such as Exemption related to Data Centres, were also discussed in the group – some points which came up for discussion- the characterisation of the amount – royalty or FTS? Whether there could be an exposure to constitute a PE.

- Participants also discussed the Transfer pricing changes, safe harbour rules, etc.

10. “Mumbai Thane Express – Internal Audit 101” held on Saturday, 21st February 2026@ CKP Hall, Thane West.

This session was organised by BCAS jointly with the Thane Branch (WIRC) of ICAI. The keynote session explored the evolving role of Internal Audit in a dynamic regulatory and business environment, highlighting the advanced use of tools and technology in modern audit practices. Discussions emphasized the transition of Internal Audit from a compliance-focused function to a strategic risk advisory partner.

A detailed deep dive into the design, evaluation, and strengthening of internal control frameworks was conducted, with risks and controls explained through relatable day-to-day examples for better understanding. Practical insights were shared on identifying Key Risk Indicators (KRIs) and effectively linking risk assessment with audit planning. A comprehensive walkthrough of risks, controls, and audit procedures in the Procure-to-Pay (P2P) cycle was presented, supported by a clear and structured audit checklist. The checklist highlighted common control gaps in procurement, vendor management, and payment processes, along with practical mitigation strategies. Special emphasis was laid on drafting impactful, concise, and action-oriented audit reports, with a strong focus on stakeholder value creation. Techniques to transform audit observations into compelling narratives that drive management action were demonstrated through practical examples.

The event concluded with a multi-stakeholder panel discussion, offering perspectives on audit expectations from management, auditors, and governance bodies. The discussion also covered aligning Internal Audit outcomes with organizational objectives and enhancing stakeholder value creation.

Approximately 65 participants from Mumbai, Thane, and Pune attended the event.

Faculties: CA Murtuza Kachwala, CA Prajit Gandhi, CA Samit Saraf, CA Chetan Thakkar, CA Pooja Bhutra, CA Harshita Mulay – Dixit, CA Archana Moghe, CA Preeti Cherian.

11. BCAS Women’s RefresHER Course” held from 6th January 2026 to 19th February 2026@ Virtual.

BCAS launched its first-ever Women’s RefresHER Course – “Re-skill and Re-ignite Your Professional Journey”, creating a dedicated platform for women Chartered Accountants to reconnect with the profession.

The course comprised 14 online sessions, conducted on Tuesdays and Thursdays, covering a wide spectrum of topics including direct tax, GST, FEMA, litigation, succession planning, ESG, audits, valuations, start-ups, and corporate structuring. The sessions were curated to address both foundational concepts and contemporary developments, with a strong focus on practical insights.

A unique feature of the programme was that it was led entirely by women speakers, fostering an open, engaging and relatable learning environment for participants.

Designed for participants at beginner and intermediate levels, including those returning after a career break or looking to build or expand their practice, the course emphasized real-life applications, emerging opportunities and confidence-building.

The programme witnessed an encouraging response, with 85 participants from around 24 towns and cities, making it an interactive experience.

Scan to watch online at BCAS Academy

II. BCAS IN NEWS & MEDIA

- BCAS has been featured in several news and media platforms, showing our active involvement, professional contributions, and commitment to the field. This reflects the growing recognition of BCAS in the public and professional space.

Link: https://bcasonline.org/bcas-in-news/

QR Code: