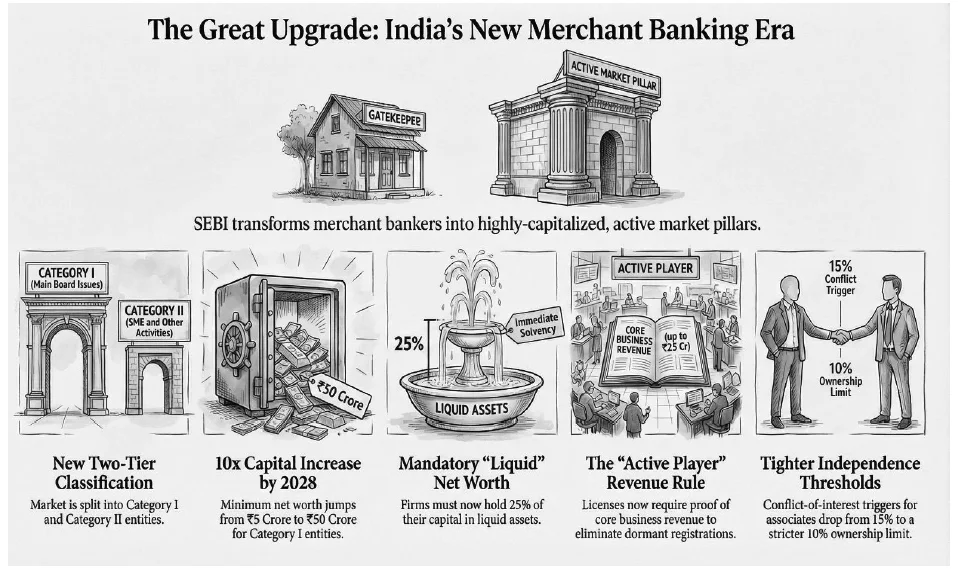

The SEBI (Merchant Bankers) (Amendment) Regulations, 2025, modernize India’s capital markets by replacing the 1992 framework. Key reforms include a tiered categorization (Category I and II) with significantly higher net worth requirements, reaching ₹50 crore for Category I by 2028. A new liquid net worth mandate and a cap on underwriting commitments (20x liquid net worth) mitigate systemic risk. To ensure active participation, minimum revenue thresholds are introduced. Furthermore, non-core activities must be managed through Separate Business Units (SBUs), shifting oversight toward substance-based supervision.

I. INTRODUCTION

Merchant bankers occupy a pivotal and institutionally sensitive position within the architecture of the modern capital market and function as the principal intermediaries and gatekeepers between issuers seeking access to capital and investors deploying risk capital.

In the Indian context, merchant bankers have historically played a foundational role in the development and expansion of the country’s primary securities market. The Securities and Exchange Board of India (Merchant Bankers) Regulations, 1992 (“erstwhile Regulations”), were formulated at a time when India’s equity markets were still in their formative phase. Issue sizes were relatively small, institutional participation was limited, and regulatory priorities were centred on market creation rather than systemic risk containment.

As we deep dive into the Indian Market Scenario in the last few decades, the scale, pace, and complexity of India’s capital markets today bear little resemblance to the conditions that prevailed when the 1992 regulatory framework was introduced.

There are more than 230 registered merchant bankers; however, only a smaller set of Book Running Lead Managers are actively managing Initial Public Offerings (IPOs). The companies planning IPOs in the upcoming Year 2026 number more than 190, of which 84 have received SEBI approval and 108 are awaiting approval. This shall set a new fundraising potential to more than ₹2.5 Lakh Crore from more than 190 issuers1.

Further, there has been a steep rise in the Draft Red Herring Prospectus (DRHP) Filings, with 19 startups and more than 24 companies preparing IPO documentation. In the month of February 2026 alone;

DRHP’s filed on SME Exchanges – 6 companies

DRHP filed on Mainboard – 2 Companies

SME IPO Listings – 14 Companies

Mainboard IPO Listings -3 Companies2.

The sharp increase in public issue sizes, the rapid expansion of the SME IPO segment and heightened retail investor participation have explicitly highlighted the limitations of the erstwhile Regulations. Acknowledging this structural disconnect, the Securities and Exchange Board of India, through the Securities and Exchange Board of India (Merchant Bankers) (Amendment) Regulations, 2025 (‘’Amended Regulations’’), has undertaken the first comprehensive amendment of the merchant banking framework in over three decades.

1 https://timesofindia.indiatimes.com/business/india-business/ipo-market-2026- over-190-companies-line-up-for-debut-over-rs-2-5-lakh-crore-fundraisingtargetted/ articleshow/126172612.cms 2 https://www.ipoplatform.com

II. REGULATORY RATIONALE FOR REFORM:

The capital adequacy framework under the Securities and Exchange Board of India (Merchant Bankers) Regulations, 1992, anchored to a uniform net worth requirement for merchant bankers of ₹five crore, had ceased to be proportionate to the scale and complexity of contemporary capital market transactions, thereby requiring increasing minimum net worth requirements in a phased manner from ₹25 Crores in 2027 to ₹50 Crores in 2028 for existing Category I regulated intermediaries, i.e. merchant bankers.

Effective from January 1, 2026, these amendments reflect a clear shift towards a prudential, risk-focused, and activity-based regulatory approach, aimed at strengthening market integrity while aligning Indian standards with evolving international regulatory benchmarks.

This regulatory transition was preceded by a structured consultative process initiated through SEBI’s consultation paper issued in August 2024, which systematically identified key gaps in the existing regime, including inadequate capital thresholds, an open-ended scope of activities, underwriting risk concentration, and the persistence of dormant registrations. This process underscores SEBI’s move towards evidence-based and participatory rulemaking in the regulation of market intermediaries.

III. KEY AMENDMENTS:

a) Capital Re Architecture: Tiered Categorisation and the advent of Liquid Net Worth

The Securities and Exchange Board of India (Merchant Bankers) (Amendment) Regulations, 2025, introduce a tiered classification of merchant bankers, creating Category I and Category II intermediaries. Category I merchant bankers are authorised to undertake all permitted activities under Regulation 13A of the Amended Regulations, including lead management of main board public issues, whereas Category II merchant bankers may undertake all other permitted activities except main board public issues. This bifurcation aligns regulatory obligations with market scale, ensuring that high-risk main board mandates are undertaken by well-capitalised entities. The revised norms shall apply to existing MBs in a phased manner as under:

| Category | Current Requirement (As per 1992 Regulations) | Phase 1 (on or before January 2, 2027) | Phase 2 (on or before January 2, 2028) |

| Category I | ₹5 crore | ₹25 crore & Liquid Net worth – 6.25 Cr. | ₹50 crore & Liquid Net worth – 12.5 Cr. |

| Category II | ₹5 crore | ₹7.5 crore & Liquid Net worth – 1.875 Cr. | ₹10 crore & Liquid Net worth – 2.5 Cr. |

*Please note all new applicants shall adhere to the revised Net worth Requirements.

b) Compliances of minimum revenue from permitted activities

It has been observed that several Merchant Bankers are engaged only in activities other than core issue management and its related activities, utilising SEBI registration primarily as a reputational asset rather than as an operational mandate. Accordingly, Merchant Bankers shall now be required to generate minimum revenue on a cumulative basis over the three immediately preceding financial years as ₹Twenty-Five Crores for Category I & ₹Five Crore for Category II. The first assessment with respect to minimum revenue from permitted activities will be carried out w.e.f. 1st April 2029. This will allow only serious and credible market players to sustain in the merchant banking business. However, professionals auditing merchant banking companies, as a matter of practice, reconcile revenue reported in Half-yearly reports to SEBI with minimum revenue from permitted activities reflected in the statement of Profit & Loss to ensure ongoing compliances.

c) Compliances in respect of underwriting obligations

The rapid growth of the SME IPO segment further exposed deficiencies in due diligence standards, underwriting discipline, and conflict management, especially among smaller and thinly capitalised intermediaries. Regulation 22B(2) of the amended regulations caps total underwriting commitments at twenty times a merchant banker’s liquid net worth, replacing the earlier regime that permitted disproportionate exposure based on notional net worth. This reform materially mitigates systemic risk and ensures that underwriting obligations are backed by financial strengths.

d) Threshold for Determining Merchant Banker Association with Issue of Securities

A merchant banker, being a promoter or an associate of either the issuer of the securities or of a person making an offer to sell or purchase securities in terms of any of the regulations made by the Board, shall not lead manage any issue or be associated with any activity undertaken under any of the regulations made by the Board by such issuer or person. The threshold for determining the association of a merchant banker, either by control directly or indirectly through its subsidiary or holding company, has been reduced from fifteen percent to ten percent.

Merchant bankers are prohibited from lead-managing public issues where their key managerial personnel or relatives hold, in aggregate, more than 0.1% of the paid-up share capital or shares whose nominal value is more than Ten Lakh rupees, whichever is lower. These measures reinforce independence, objectivity, and fiduciary accountability across merchant banking operations.

e) Professional Accountability and Institutional Governance

The amended framework also elevates professional standards within merchant banking entities. Principal officers must possess a minimum of five years’ experience in financial markets. Compliance oversight has been strengthened under Regulation 28A through mandatory NISM Series-IX and Series-IIIA certifications, reinforcing regulatory adherence and investor protection. Transitional provisions allow existing compliance officers to continue subject to experience thresholds and timely certification, balancing continuity with enhanced competence.

f) Redefining the Scope of Merchant Banking and the Separate Business Unit (SBU) Framework

The Amendment Regulations explicitly recognise that SBUs are not separate legal entities; the focus is on in substance segregation, operational independence, independent reporting lines, and the maintenance of robust Chinese walls to prevent risk contagion. Under the amended Regulation 13, merchant bankers are expressly permitted to undertake activities directly connected to the securities market lifecycle, including;

(i) managing of public issues, qualified institutions placements, rights issues of securities and advisory or consulting services incidental to such issues;

(ii) managing of:

a. acquisitions and takeovers under the Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011;

b. buy-back under the Securities and Exchange Board of India (Buy Back of Securities) Regulations, 2018;

c. delisting under the Securities and Exchange Board of India (Delisting of Equity Shares) Regulations, 2021;

d. compliances as may be required under the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 in respect of any scheme of arrangement;

e. implementation of a scheme under the Securities and Exchange Board of India (Share Based Employee Benefits and Sweat Equity) Regulations, 2021; and

f. advisory or consulting services incidental to the activities specified in clauses (a) to (e);

(iii) underwriting activities as specified by the Board from time to time; private placement of listed or proposed to be listed securities on a stock exchange recognised by the Board and activities incidental thereto.

(iv) advisory or consulting services incidental to the activities specified in clauses (a) to (e);

For the purpose of this clause, ‘securities’ shall be treated as ‘proposed to be listed’ from the date of approval of the board resolution of the issuer, for the issuance of such securities to be listed on a stock exchange recognised by the Board;

(v) managing the international offering of securities and advisory or consulting services incidental to such offering;

(vi) filing of placement memorandum of an alternative investment fund;

(vii) issuance of a fairness opinion;

(viii) managing of secondary market transactions of securities listed on a stock exchange recognized by the Board and activities incidental thereto;

(ix) market making in accordance with the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018;

(x) and any other activity as may be specified by the Board from time to time.

Activities outside the core list are no longer permissible as part of merchant banking and must, if undertaken, be conducted through Separate Business Units (SBUs), thereby ensuring a clear distinction between core merchant banking and other financial services activities. To ensure a smooth transition, existing merchant bankers are required to restructure non-core activities into SBUs within six months from the effective date of January 1, 2026.

Key Differences in Erstwhile Regulations and Amended Regulations

| Feature | 1992 Regulations (Erstwhile Regulations) | 2025 Amendments (Amended Regulations) | Strategic Shift |

| Categorization | Unitary framework (Category I dominant) | Two-tier framework (Category I and Category II) | Recognition of market bifurcation between Main Board and SME platforms |

| Minimum Net Worth | ₹5 Crores | ₹50 Crores (Category I) / ₹10 Crores (Category II) | Increase to ensure financial resilience and institutional strength |

| Liquidity Requirement | No specific liquidity requirement | Mandatory Liquid Net Worth (minimum 25%) | Shift from book solvency to immediate solvency |

| Underwriting Exposure | No explicit cap on underwriting | Underwriting capped at 20× Liquid Net Worth | Risk-taking capacity strictly linked to liquid capital |

| Valuation Activity | In-house valuation permitted | Valuation prohibited; mandatory use of Registered Valuer | Removal of conflict of interest between deal execution and valuation |

| Data Localization | No data localization requirement | Mandatory data storage within India | Data sovereignty and assured regulatory access |

| Record Retention Period | 5 years | 8 years | Alignment with tax, enforcement, and other investigation statutes |

| Activity / Revenue Requirement | No minimum revenue requirement | Minimum revenue thresholds: ₹25 Cr (Category I) / ₹5 Cr (Category II) | “Active player” doctrine to eliminate dormant registrations |

VI. Way Forward: Towards a Resilient, Credible and Globally Aligned Merchant Banking Ecosystem

The regulatory overhaul of the merchant banking framework marks a transformative step in the evolution of India’s merchant banking landscape, establishing a regulatory directive that carefully balances prudential discipline with operational flexibility. The Amended Regulations enable market participants to adapt to heightened standards without disrupting market continuity or capital formation.

Some of the key takeaways are:

- Merchant banking regulation in India has decisively moved from form-based registration to substance-based supervision, commensurate with the evolving and growing capital market activities.

- Capital adequacy is operationally enforced through tiered net worth thresholds, liquid asset requirements, and underwriting exposure limits.

- The positive list framework defines the boundaries and permissible merchant banking activities.

- Licence continuity is now tied to demonstrable market participation, reinforcing the principle that merchant banking is an active institutional responsibility rather than a passive regulatory entitlement.

Collectively, these measures position India’s merchant banking industry to operate with greater credibility, resilience, and strategic alignment with international standards, ensuring that the primary markets function efficiently and securely while supporting long-term capital formation objectives.