1. Finance, Corporate & Allied Law Study Circle – REIT n InvIT as Investment avenues held on Thursday, 13th February, 2025 @ Zoom.

CA Harry Parikh explained the concepts of REIT and InvIT, their features, structural overview, eligibility criteria, investment conditions, etc. He highlighted that REIT or InvIT are investment products and not a tax-saving product. He dealt with the decision-making criteria for investing in REIT or InvIT vis-a-vis traditional investment with the help of examples of REITs. He also enlightened on the key differences between Equity vs. Mutual Fund vs. REIT vs. InvIT, and tax implications thereof. He also shared his insights on factors to be considered for investing in REIT.

More than 70 participants enriched out of the masterly analysis of REIT, InvIT as investment avenues.

Youtube Link: https://www.youtube.com/watch?v=GxO-5VpL-xk

2. Public Lecture Meeting on “Union Budget 25 — Indirect Tax Proposals” held on Wednesday, 12th February 2025 @ Zoom.

The lecture meeting on the Union Budget 2025 and its Indirect Tax Proposals, held on 12th February 2025, featured CA Sunil Gabhawalla discussing various amendments in the Finance Bill 2025. He focused primarily on GST provisions while briefly touching upon customs, excise, and service tax amendments.

He began by explaining the concept of ‘input service distributor,’ detailing its position in the pre-GST regime, GST regime until 31st March 2025, and the post-2025 scenario. He highlighted differences in the definition of ‘Input Service Distributor’ (ISD) between the existing and proposed regimes, emphasising the potential for varied interpretations and possible litigations. Using the draft circular issued by the CBIC and other relevant jurisprudence, he illustrated cases falling under the ISD and Cross Charge Mechanisms.

He also examined the impact of retrospective amendments in the GST law, referencing the Hon’ble Supreme Court’s decision in the Safari Retreat’s case and highlighting open issues post-amendment. Further, he discussed issues arising from the amendment that incorporates additional conditions for self-adjustment of taxes based on credit notes. He provided guidance on addressing these issues, especially in light of the mandatory Invoice Management System (IMS) introduced by GSTIN in October 2024. He cited practical examples to highlight various aspects taxpayers should consider when dealing with the IMS mechanism. Additionally, he explained how the proposed track and trace mechanism would complement E-way Bill provisions. The meeting emphasised the government’s intent to gather maximum data and use artificial intelligence to curb tax evasion, leading to increased compliance and affecting the ease of doing business.

Finally, he covered miscellaneous amendments related to ‘local authorities,’ ‘vouchers,’ amendments in Schedule III concerning supplies by SEZ / FTWZ units, and the rationalisation of pre-deposits required under appellate proceedings in disputed orders imposing penalties.

The lecture was attended by approximately 325 participants online.

BCAS Lecture Meetings are high-quality professional development sessions which are open to all to attend and participate. The readers can view the lecture meeting at the below-mentioned link:

Youtube Link: https://www.youtube.com/watch?v=yAzBv4CAHNw

3. Public Lecture Meeting on Direct Tax Provisions of Finance Bill, 2025 held on Thursday 6th February, 2025 @ Yogi Sabhagruh Auditorium Dadar East

The public lecture on Direct Tax Provisions under the Finance Bill 2025 was a comprehensive discussion led by noted tax expert CA Shri Pinakin Desai. The session emphasised the significant changes in income tax slab rates and corresponding rebate provisions, which were perceived positively. The lecture highlighted that this year’s budget prioritises stimulating consumption over infrastructure investment, marking a substantial increase in tax-free slab rates compared to previous years. Notably, there was a significant shift anticipated as taxpayers may transition from the old tax regime to the new one, leading to increased discretionary spending and ultimately contributing to GDP growth.

Shri Pinakin Desai provided insights into several key provisions of the Finance Bill, 2025 analysing changes to tax rates, corporate taxation, TDS rationalisation, and the taxation of charitable trusts. The lecture also discussed new provisions concerning Tax Collection at Source (TCS) and implications for companies undergoing amalgamations. Shri Pinakinbhai’s thorough analysis offered clarity on how these changes would affect various stakeholders and emphasised the need for careful navigation of the new tax landscape.

KEY INSIGHTS

- Increased Tax-Free Income Thresholds: The new regime allows individuals to earn up to ₹12.75 lakhs without incurring tax, significantly benefiting middle-income taxpayers. This change is expected to uplift the overall spending capacity of households, resulting in higher consumption rates and positively influencing economic growth.

- Charitable Trust Registration Validity: The extension of the registration period for small charitable trusts from five to ten years represents a significant reduction in administrative burdens for these entities, encouraging more charitable initiatives and financial stability among smaller trusts.

- Tax Deductions for Rent Payments: The amendment reducing the threshold for tax withholding on rent from ₹2.4 lakhs annually to ₹50,000 monthly for companies is a notable change.

- Implications of Changes in applicability of Rebate: The decision to disallow rebates for special rate incomes under capital gains could reduce tax relief for many taxpayers, necessitating careful consideration of investment strategies to optimise tax liabilities.

- Restrictions on Loss Migration: The amendment aims to curb the indefinite extension of loss carry-forwards through repeated amalgamations, ensuring a fair and consistent tax treatment. Previously, amalgamated companies could extend the carry-forward period indefinitely, effectively resetting the 8-year limit with each new amalgamation. The amendment aims to prevent this perpetual “evergreening” of losses. Shri Pinakinbhai explained the impact of this amendment through various illustrations.

- Non-Resident Tax Incentives: The concessional tax rates for foreign entities providing technology and services to specified manufacturing industries reflect India’s strategy to foster foreign investment in critical sectors such as electronics, enhancing competitive advantages and technological development. A new presumptive taxation scheme introduced for non-residents providing services or technology to Indian companies engaged in the manufacture of electronic goods. Shri Pinakinbhai also highlighted possibility of a drafting error in the proposed legislation, mistakenly suggesting that both payment and receipt of 100 rupees result in a taxable consideration of 200 rupees which should be corrected to align with sections 44B and 44BB, of the Income-tax Act.

- Extension of time limit for passing Penalty Orders: The time limit for completing penalty orders related to assessment has been changed from 6 months from the month of receiving the order from the tribunal to 6 months from the end of the quarter of receiving the order.

- Transfer Pricing Assessment: Instead of annual assessments, a block of 3 years for determining the Arm’s Length Price (ALP) is introduced. Once the methodology is settled in the first year, it remains binding for the next two years. Taxpayers can opt for this block assessment, either during or after the Transfer Pricing (TP) assessment. He also mentioned that the effectiveness of these new measures shall depend upon the rules to be prescribed in this regard.

- Updated Return Filing: The provision now allows updated returns to be filed up to the end of the third or fourth year, with additional taxes of 60 per cent and 70 per cent, respectively. This provision aims to promote compliance by offering a structured approach for taxpayers to rectify errors or omissions, albeit with significant additional tax implications for later filings.

In summary, the lecture delivered by Shri Pinakin Desai provided a detailed analysis of the Finance Bill 2025, shedding light on various changes that will impact individual taxpayers, businesses, and charitable organisations alike. The meeting was attended in person by 450 plus participants and encouraging response of over 26,000+ viewers online.

The readers can view the lecture meeting at the below-mentioned link:

Youtube Link: https://www.youtube.com/watch?v=ncVT3ejAtPA

4. Felicitation of Chartered Accountancy pass-outs of the November 2024 Batch held on Friday, 31st January, 2025 @ IMC.

Milestone 2.0 — Felicitation of newly qualified CAs of the November 2024 batch.

A felicitation event for the newly qualified chartered accountants of the November 2024 batch was held on 31st January, 2025, at the Walchand Hirachand Hall of the Indian Merchant Chambers building at Churchgate by the SMPR Committee. The event was highly successful and close to 400 candidates attended the event. The theme for the event was Milestone 2.0, and the guest and mentor for the event was Past President CA Naushad Panjwani. He guided the participants by taking them through the Japanese concept of Ikigai and drawing parallels to their phase in life where they should aim to find their Ikigai, which would lead them to success and happiness. The participants diligently listened and also provided their perspectives on the matter. Rankers were felicitated first, and they addressed the audience subsequently and shared their experience throughout the journey of becoming a CA. A celebratory cake was cut and then all the successful newly passed CAs were felicitated. The excitement on everyone’s faces was visible, and that is testimony to the success of the event.

5. Indirect Tax Laws Study Circle Meeting held on Friday, 31st January, 2025 @ Zoom.

Group leaders CA G. Sujatha & CA Archana Jain prepared and presented various case studies on Government Supplies and explained the concepts of Central Government, Government Authority, State Government, etc.

The presentation covered the following aspects for detailed discussion:

1. Concept of Supplies by Central Government, State Government, Local Authority.

2. Supplies liable to tax or part of sovereign function.

3. Taxability of charges paid to the Ministry of Corporate Affairs at the time of registration & subsequently do both enjoy the exemption.

4. Detailed discussion on mining rights and other rights associated with land and fees paid for getting rights.

Around 60 participants from all over India benefitted by taking an active part in the discussion. Participants appreciated the efforts of the group leader & group mentor.

6. ITF Study Circle Meeting held on Thursday, 30th January, 2025 @ Zoom.

Group Leaders – CA Nemin Shah and CA Dipika Agarwal

Guidance for Application of Principal Purpose Test under India’s treaties vide CBDT Circular 1/2025 dated 21st January, 2025 (Circular) — Group Leader CA Nemin Shah.

During the session, CA Nemin Shah discussed the context relating to the Principal Purpose Test (PPT). For this, he extensively discussed the basics of MLI and PPT. Another perspective which was discussed was whether PPT was for general anti-avoidance or a specific anti-avoidance. The Group Leader went on to discuss the key points of the Circular, such as the application of PPT is based on an objective assessment of the relevant facts and circumstances, its applicability in cases where the PPT has been incorporated through bilateral negotiations or through MLI, the scope of grandfathering provisions under the treaties which will remain outside the purview of PPT. He went on to discuss the various issues that could arise, such as its applicability to the India-Mauritius tax treaty, which MLI does not cover.

SC Lowy P.I. (Lux) S.A.R.L, Luxembourg v. ACIT [2024] 170 taxmann.com 475 (Del-Tribunal) – Group Leader CA Dipika Agarwal

CA Dipika explained the facts and the arguments of the assessee and revenue. She discussed the Tribunal’s findings. One of the key focus points of the discussion was that it appeared from the Tribunal’s order that PPT was not invoked at the assessment level, but discussed only at the Appellate level. Further,

there was no discussion in the Tribunal’s order for choosing Luxembourg over the Cayman Islands for making investments. The group discussed the implications of the same. The Group Leader went on to discuss the Tribunal’s findings in relation to Tax Residencey Certificate (TRC) and Limitation of Benefits (LOB). With respect to the PPT clause, the assessee’s incorporation in Luxembourg was not for the principal purpose of obtaining tax treaty benefits, as it had substantial investments, which it continues to hold.

7. 22nd Residential Leadership Retreat — Living in Harmony held on Friday, 24th January, 2025 and Saturday, 25th January, 2025 @ Rambhau Mhalgi Prabodhini Keshav Srushti Bhayander (West)

The 22nd Leadership Retreat was held on the theme of `Living in Harmony’ under the guidance and training of Mr M. K. Ramanujam and Mr R Gurumurthy. 27 participants including 6 couples attended, of which, more than 15 participants were attending the Leadership Retreat for the first time.

The key learnings are summarised as follows:

- Harmony is unity in diversity which brings joy, peace, happiness, satisfaction and fulfilment.

- One has to focus from zoom in to zoom out. i.e. look at the wider picture from a broad perspective for a higher purpose over a long span and come out of small and micro views. Zooming out is like a compass of values to find the right meaning in life.

To identify challenges, zoom in and use an emotional filter to zoom out.

- P R E M A: The acronym represented Positive Emotions, Relationship, Engagement.

- (Karma Yoga), Meaningful Life and Achievement – selfless service for a noble cause. This could be the guiding light.

- Listen vis-a-vis Silent. Listen with empathy and compassion. Words “Silent” and “Listen” are complementing. So, engage in listening to be silent within and establish connect outside.

- R A S (Reticular Access Syndrome) explains that whatever one focuses on, expands in the mind. We see the world as we are. So, one can use this to reinforce the attention to important things in life.

- Nature operates on contrast. Sattva, Rajas and Tamas are like an interplay of darkness and light. The contrast of bright and dark, light and dark, day and night, white and black, happiness and sadness, joy and gloom. Contrast is natural. Negative things help us to appreciate the value of positives. Pain is a warning signal to pause. Self-acceptance guides us to Harmony. Therefore, one can transform from fear to faith, anger to care and work to relax.

- Practice Harmony by observing without being judgemental.

- Understand the basic needs, physical, social, spiritual, personal, interpersonal. The needs are distinct from wants. Needs are expressed through feelings. Listen to the feelings. One can understand that anger moves us away, whereas Love and compassion bring us closer to Harmony. Human pursuit (Purushartha) is for Kama, Artha, Dharma & Moksha. The purpose of human life is Moksha, for which doing Kama or pursuing Artha should be based on Dharma, respecting the highest universal values and principles.

- Like a peel on the surface of a juicy fruit, the outer layer may have an unpleasant taste, but with faith and conviction, one can have the taste of juice and nectar within.

- Bring inner transformation by working from Gratitude with Empathy & compassion.

In the penultimate session, discussion was on the film Peaceful Warrior and the inspiring message coming out from the film’s dialogues.

In the concluding session, the participants shared the key points of learning from the camp.

8. Fireside Chat on “Return of Trump – What does it mean for America, India and the World” held on Monday, 27th January, 2025 @ BCAS

Speaker: Shri Natwar Gandhi

Moderator: Shri Rashmin Sanghvi

Widespread fear about various executive orders signed by Mr Trump is misplaced as most of them have been challenged and will have to pass the test of constitutional validity.

America has a strong democracy and deep-rooted institutions. No president can make fundamental changes at his will. Even with a majority in Congress and Senate, constitutional changes are not going to be possible in his four-year term.

One can expect him to use tariffs as a negotiating tool to gain trade favours. However, in the long term, it will hurt the US as well as the country on which high tariff is levied because it will lead to higher costs and consumer resistance. That will not augur well for the USA.

The USA will continue to be a dominant world power as long as the majority of trade uses USD as currency for settlement.

Tall claims about taking over some territories should be discounted as election rhetoric.

The US economy, despite popular perception, is doing well, with average household income (even in the most backward area) still much above par with the rest of the world. With the new administration, one can expect business-friendly policies and a return to manufacturing.

It will be difficult to reduce bureaucracy as all policies require ground-level staff to implement. The USA, with its large size and federal structure, will make such reduction only ornamental.

A large deficit close to USD 35 trillion will not curtail any growth initiatives as the world still uses America as its investment and wealth destination.

Despite threats, it will neither be possible nor practicable to deport almost 10 million illegal immigrants out of the US due to procedural and logistic challenges. By rough estimate, the cost and time of that purge will be 1 trillion USD and will take more than 10 years for the current number.

White supremacy lobby will continue to flourish, and borders will see very strong protection to prevent illegal immigrants from entering the USA. Despite that America is likely to become a Hispanic state with so many migrants from Latin America.

Skilled labour will be there to stay as the big business will not be able to operate without them. Hence, despite all the shouting about work visas, they will stay.

9. Webinar on Recent Important Decisions under Income Tax held on Friday, 24th January, 2025 @ Virtual

The Taxation Committee of the Bombay Chartered Accountants’ Society organised a Webinar on Recent Important Decisions under Income Tax.

Adv. Devendra Jain delivered an in-depth presentation on reassessment proceedings. He explained the evolving judicial perspective on reassessment, especially in light of recent amendments and rulings by the Supreme Court and the High Courts. His session provided clarity on the crucial points to be considered while representing matters on reassessment cases.

Adv. Ajay Singh began the session by providing a detailed analysis of key judicial decisions that have significant implications for the interpretation and application of Income tax laws. He highlighted the judgments relating to capital gains, gift tax under section 56(2)(x), reduction of share capital, Condonation of delay in filing forms, interest on IT refund, penalty provisions and share transactions, focusing on their impact on taxpayers and professionals alike. He emphasised the importance of understanding these rulings to develop better compliance and advisory strategies.

The session provided participants with a comprehensive understanding of recent developments in Income tax law and practical insights to navigate legal complexities.

Youtube Link: https://www.youtube.com/watch?v=FlL13OSdCOw

10. 25th Silver Jubilee Course on Double Taxation Avoidance Agreements held from Monday, 2nd December, 2024, to Tuesday, 21st January, 2025 @ Zoom.

The Society successfully conducted its 25th Silver Jubilee Study Course on ‘Double Taxation Avoidance Agreement’ via an online platform spanning from 2nd December, 2024 to 21st January, 2025.

Based on participants’ feedback and consultation with seniors in the Committee, for this 25th Silver Jubilee Course on Double Taxation Avoidance Agreements, BCAS has come up with a unique concept of sharing the recordings of the 24th DTAA Course undertaken in December 2023 as an option to the participants followed by multiple panel discussions. One introductory session on “Overview of International Taxation & DTAAs” and ten panel discussion sessions were planned to take forward the learnings by discussing the intricate and practical issues on the topics of International Taxation, making the course more interactive. Participants were also provided an option to share the queries or issues to the panellists by way of Google form before the respective panel discussion. Eminent tax professionals of the country were the panellists as well as moderators for the series of panel discussions.

All sessions of the course, including last year’s recorded sessions, covered all articles of DTAA, an overview of FEMA / BEPS / MLI / GAAR, Transfer Pricing, Source Rules under the Income Tax Act, 1961, TDS under section 195, Substance v/s Form, and other relevant provisions. The course included complex topics such as Taxation of Specific Structures (e.g., Partnership, Triangular Cases, AOP, etc.) and Selection of Structures.

More than 200 Participants from 15 states spread over 30 cities attended the course which was well-received and appreciated by the participants.

11. Revolutionising CA Practice with Generative AI: Practical Use Cases for Efficiency and Growth held on Thursday, 9th January, 2025 @ Virtual

CA Rahul Bajaj recently led an insightful 2-hour webinar, “Revolutionising CA Practice with Generative AI: Practical Use Cases for Efficiency and Growth,” showcasing how AI can transform Chartered Accountancy practice. The session delved into real-life applications of Generative AI, highlighting its potential to enhance productivity, streamline operations, and improve client servicing. Participants learned how AI can be used to draft professional emails, generate legal documents, automate data entry in Tally, and prepare financial forecasts, all while saving time and reducing errors.

Key takeaways included using AI to create checklists, templates, and peer review documentation like Engagement and Appointment Letters. AI also supports the generation of client training materials, social media content, and even notices, helping firms stay engaged with clients while improving efficiency. By automating repetitive tasks such as bank statement analysis, CAs can focus more on strategic activities, boosting overall productivity.

The session concluded with CA Rahul Bajaj emphasising the importance of integrating AI into CA practices for long-term growth. With tools that enhance accuracy and decision-making, AI is positioning itself as a game-changer, enabling Chartered Accountants to provide higher-value services and streamline their operations for greater success in an increasingly digital world.

The excellent response that the webinar got in terms of enrolment from across various cities of India and from persons of various age groups, as well as the feedback received at the end of the webinar, is testimony to the growing importance and popularity of AI in the CA fraternity.

12. BCAS Turf Cricket Tournament 2025 held on Sunday, 5th January, 2025 @ Andheri Sports Complex, Azad Nagar, Andheri West

The BCAS Turf Cricket Tournament 2025 held on 5th January 2025 at Andheri Sports Complex, was a resounding success, hosting 12 men’s and 2 women’s teams in a thrilling display of sportsmanship and camaraderie.

The tournament was exclusively for CA Members, Students, and BCAS Staff was well received with overwhelming participation.

The format in Men’s category was of four groups of three teams each, which formed the league stages followed by knockout rounds of Quarter-finals (8 teams), Semi-finals (4 teams) and the Finals. The 12 Men’s teams that competed in the Tournament were Bansi Jain Warriors, Bathiya Bravehearts, BYA Titans, CNK Super Strikers, G&S Gladiators, Kirtane & Pandit Maestros, KNAV Smashers, MAS Mavericks, MCS Super Kings, MGB Yoddhas, NPV Challengers and TeaMPC whereas the 2 Women’s teams were NPV Thunderbirds and BCAS Queens.

The tournament was filled with exciting matches, impressive individual performances, fun-filled live commentary and enthusiastic support from the spectators. The 8 teams that qualified for the Men’s quarterfinals were MAS Mavericks, Kirtane & Pandit Maestros, CNK Super Strikers, MGB Yoddhas, G&S Gladiators, NPV Challengers, KNAV Smashers and Bathiya Bravehearts. The Semi Finals were then played between the 4 teams viz. Kirtane & Pandit Maestros vs. NPV Challengers and CNK Super Strikers vs Bathiya Bravehearts.

The day culminated in a nail-biting Men’s final between Bathiya Bravehearts vs Kirtane & Pandit Maestros, with the former emerging victorious whereas BCAS Queens emerged as winners in the Women’s category.

The tournament left a lasting impression on all participants and thus setting the stage for future editions of this exciting event.

13. BCAS Nxt Learning and Development Bootcamp on Idea to IPO: A Beginner’s Guide held on Saturday, 4th January, 2025 in hybrid mode

The Human Resource Development Committee of BCAS organised a BCAS NXT Learning & Development Bootcamp on “Idea to IPO: A Beginner’s Guide” on Saturday, 4th January, 2025. The session was led by Mr Aditya Rathod, a CA Final student, who delivered a comprehensive presentation on the fundamentals and key regulations governing IPO in India. His presentation covered a wide range of topics, including essential definitions, various IPO methods, and an overview of the IPO process and its approach. He also shared practical experiences to help beginner article students navigate the complexities of the IPO Listing Process.

CA Rimple Dedhia, the mentor for the session, provided valuable insights and guidance throughout, offering expert interventions as needed. The boot camp was held in person at the Mehta Chokshi & Shah LLP office and streamed online, with active participation from students across India.

Youtube Link: https://www.youtube.com/watch?v=-WYuPDeOJus&t

14. Series of Sessions on Standards on Auditing and Key Learnings from NFRA Orders held on Friday, 13th December, 2024 to Friday, 3rd January, 2025 @ Zoom

BCAS has always been a pioneer in equipping its members, in particular and other stakeholders at large with the knowledge in the arena of Accounting Standards, Ind AS and Standards on Auditing. The challenge of the auditor is to address the risks posed while providing assurance services within the regulatory framework of ICAI and NFRA. Compliance with Auditing Standards is of utmost importance while carrying out audits.

Considering these challenges that the auditor has to address while performing duties, the Accounting & Auditing Committee organised a well-designed series of virtual sessions covering Auditing standards and Key Learnings from NFRA orders, which should be kept in focus while executing audit assignments along with practical guidance. The Sessions were held on Fridays for 2 hours each, totalling 8 hours.

The main objective of designing this series of sessions was to delve deeply into the subjects affecting the audit fraternity and to provide a platform for the Members in Practice to come together and get the opportunity to have deep insights into the practical challenges which crop up while implementing the complicated standards.

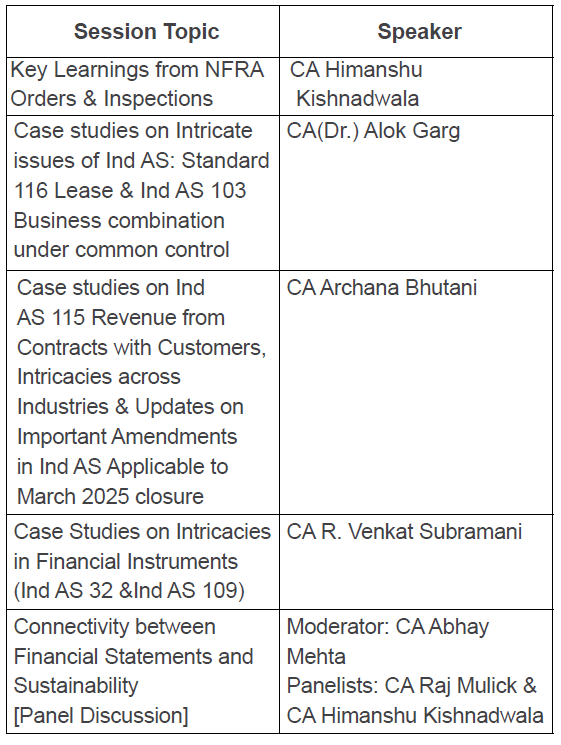

Course Segments: 4 sessions of 2 hours each

| Session Topic |

Speaker |

| Learnings from recent NFRA Orders |

Ms Vidhi Sood Secretary, NFRA |

| Audit Documentation (SA 230) |

CA Amit Majmudar |

| SA 600 – Using the work of another auditor (along with the NFRA Circular dated October 03, 2024, regarding responsibilities of the Principal Auditor and Other Auditors in Group Audits |

CA Pankaj Tiwari |

| Planning risk assessment and related matters (SA 300, 315, 320 & 330) |

CA Murtuza Vajihi |

The sessions were designed to give practical and case study-based insights to the participants on various topics.

The course was inaugurated with the opening remarks from the Chairman of the Accounting and Auditing Committee CA Abhay Mehta and the President of BCAS, CA Anand Bathiya, both underline the importance of knowledge sharing and the role of the BCAS in conducting such programs. To make the course effective, faculties with specialised knowledge and relevant experience were engaged to give participants practical insights and wholesome experiences.

The course started with the session of Ms Vidhi Sood Secretary, NFRA, where she updated the participants on various NFRA orders, practical examples and issues and learnings from the same.

The session of Audit Documentation SA 230 by CA Amit Majmudar broadly covered the areas pertaining to the Assembly of Audit Files, Key Audit Workpapers and guidance on ICAI Audit Documentation

The Session on SA 600 — Using the work of another auditor by CA Pankaj Tiwari mainly covered existing SA 600 & procedures adopted by the Auditor, various lapses highlighted by NFRA in the audit of CFS, Key elements of Circular issued by NFRA & potential challenges in implementation of the Circular.

The session on Planning Risk Assessment and Related Matters by CA Murtuza Vajihi broadly covered the scope, objective, and documentation of the standard along with practical examples of the standards and also reference to NFRA and QRB learnings on these standards.

The above sessions generated a lot of interactions between the participants and the respective faculties. The course commenced on 13th December, 2024, and ended on 3rd January, 2025. 111 participants attended the Course, and was well received with the overall feedback from the participants was very encouraging.

REPRESENTATIONS AND SOCIAL MEDIA

1. NFRA Representation: Addressing Duplication in Fraud Reporting for Statutory Auditors

BCAS has submitted a representation to the National Financial Reporting Authority (NFRA) regarding the fraud reporting requirements for statutory auditors of regulated entities. The representation highlights the need to eliminate the duplication of reporting to various authorities, aiming to streamline the process and simplify the regulatory framework for entities such as banks, insurance companies, and NBFCs. By reducing redundant reporting, the proposal seeks to create a more efficient and effective regulatory environment.

Readers can read the entire representation by link: https://bit.ly/NFRA-Representation

2. Union Budget 2025: 8th Consecutive Budget by FM Nirmala Sitharaman — BCAS’s Pre-Budget Memorandum Available Online.

As Finance Minister Nirmala Sitharaman presents her 8th consecutive Union Budget, BCAS continues its proactive role in representing the views of its members and the wider community. We are pleased to announce that BCAS has submitted the Pre-Budget Memorandum for the Finance Act 2025-26 to the Union Minister of Finance and the Ministry of Finance, Government of India.

Readers can read the entire representation by link: https://bit.ly/Pre-Budget-Memorandum-2025-26

3. BCAS Reimagine Conference: Exclusive Videos Now on YouTube, with Thousands of Views!

BCAS hosted the ReImagine Conference, a three-day event in January 2024 that explored progressive topics crucial to the professional landscape. With an overwhelming response, the discussions held the potential to shape the future trajectory of our profession.

In line with BCAS’s mission of knowledge dissemination for professional development, the event videos are now available on YouTube, completely free of charge. Featuring a wide range of topics presented by industry experts and professional stalwarts, these videos offer valuable insights for professionals at all levels.

Playlist Titles:

1. Reimagine India – Keynote Address by Padma Bhushan Shri Kumar Mangalam Birla

2. Digital Infrastructure – A Game Changer

3. Reimagine the new age professional firms

4. CFO Round Table – Technology, Innovation and Sustainability

5. Use of AI / Tech-Data as Evidence in Tax Cases – Direct Tax and Indirect Tax

6. Reimagine India’s Capital Market Landscape

7. Changing Corporate Landscape – Professional opportunities

8. The Victorious – A Model for Leadership

9. New Age Wars – Future of the World – Role of Professional

10. One World – One tax – VasudhaivaKutumbakam

11. Ride the Capital Market – Take the Bull by its Horns

12. The Future of Audit Profession

13. One Giant Leap – Start-ups – Importance of Professionals in Start up Journey

14. Interchanging Roles – Practice to CFO, CFO to Practice, CA to Nation Building

15. Reimagine – Closing Ceremony & Vote of Thanks

YouTube link: https://bit.ly/Reimagine-Conference

4. BCAS YouTube Channel Hits 1 Million Views

The BCAS YouTube channel has reached a significant milestone, surpassing 1 million views. Over the years, it has evolved into a valuable resource, offering a wealth of professional content and knowledge. With an expanding collection of open-for-all sessions, the channel continues to serve as a hub for valuable learning. Members who have not yet subscribed are encouraged to do so and stay updated with the latest content.

Youtube Link: https://www.youtube.com/channel/UC3cxrmOi8hRA31LxBEXGpUQ

5. Interactive meeting of managing Committee Members with Dr Harish Mehta and Mr Rajiv Vaishnav

Dr Harish Mehta and Mr Rajiv Vaishnav were invited to interact and share their experience of building and successfully running the NPO with the BCAS Managing Committee members on 8th January, 2025.

Dr Harish Mehta is a founder member and former Chairman of NASSCOM and Rajiv Vaishnav is former President of NASSCOM. They shared experience in building brands, nurturing teams, and growing organizations. During the interaction, Dr. Harish Mehta and Mr. Rajiv Vaishnav appreciated the work done by BCAS and emphasised the importance of valuing volunteers, building trust, and promoting unity, especially during challenging times. They also advised that before making representations to government authorities, it’s essential to gather collective opinions from members.

Dr Mehta autographed copies of his book, “Maverick Effect: The Inside Story of India’s IT Revolution”, for the committee members.

BCAS IN NEWS

Link: https://bcasonline.org/bcas-in-news/