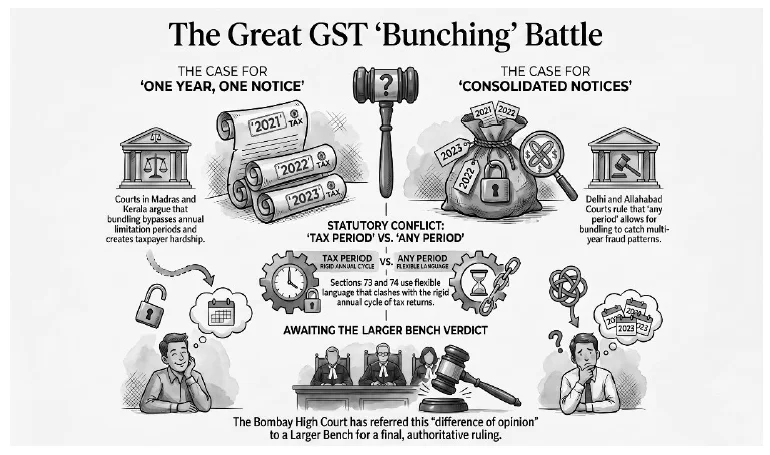

GST litigation is currently divided over whether authorities can issue single, consolidated Show Cause Notices (SCNs) for multiple financial years. High Courts in Madras, Kerala, and Bombay have quashed such notices, arguing the CGST Act treats each financial year as a separate unit with independent limitation periods. Conversely, the Delhi and Allahabad High Courts permit “bunching,” interpreting the phrase “any period” in Sections 73 and 74 as allowing flexible, issue-based adjudication. Due to these conflicting rulings and practical portal challenges, the Bombay High Court has referred the dispute to a Larger Bench.

INTRODUCTION

The question of whether the revenue authorities can issue a single, consolidated Show Cause Notice (SCN) covering multiple financial years or tax periods has emerged as a significant point of contention in Goods and Services Tax (GST) litigation. This issue has created a sharp “difference of opinion” among various High Courts across India. Recently, the Bombay High Court, in the case of M/s. Rollmet LLP vs. The Union of India1, took note of these conflicting precedents—specifically the discrepancy between its own earlier decision in Milroc Good Earth Developers2 and the views of the Delhi and Allahabad High Courts3 in Mathur Polymers, Ambika Traders and SA Aromatics Pvt. Ltd’s case respectively — and referred the matter to a Larger Bench for authoritative determination. This article examines the dispute in detail.

At the heart of the dispute is whether the adjudication machinery provided under Sections 73 and 74 of the Central Goods and Services Tax (CGST) Act, 2017, is restricted by the concept of a “financial year” as a unit of assessment, or whether the phrase “any period” employed in the statute allows for the bunching of multiple years into a single proceeding.

1 [2026] 185 taxmann.com 599 (Bombay) 2 [2025] 179 taxmann.com 465 (Bombay) 3 [2025] 177 taxmann.com 860 (Delhi) ; [2025] 177 taxmann.com 134/101 GSTL 64 (Delhi) & [2026] 183 taxmann.com 437 (Allahabad)

HISTORICAL CONTEXT

To comprehend the depth of this conflict, one must recognize that the CGST Act is a legislative synthesis of two fundamentally distinct historical tax philosophies. Under the erstwhile Central Excise and Service Tax laws, adjudication was driven by an “issue-based” adjudication process (i.e. started with identified issues rather than tax periods). Multiple year tax demands were routinely clubbed into a single notice, and at the same time, it was not uncommon to have multiple show cause notices for the same period dealing with distinct issues. The law lacked a concept of a comprehensive annualised assessment of records.

Conversely, State Value Added Tax (VAT) and Sales Tax laws operated on a “period-based” cycle. Assessment was inextricably tied to a specific financial year, providing a terminal point for the Revenue’s power to assess the taxpayer’s liability. The assessment process started from year-wise self-assessed records and tax demands raised for each year separately. More importantly, all the issues for a particular period were comprehensively dealt with in a single order.

The CGST Act attempts to imbibe both “return-based compliance” mechanisms of VAT and the “issue-based adjudication machinery” of Excise. This structural duality is the root cause of the current interpretational friction. The dispute gets amplified on two counts: firstly, the divergent administrative practice in the State and Central tax GST formations while performing assessments/ adjudications and secondly, the portal architecture for uploading of notices and orders and tracking demands and payments.

STATUTORY FRAMEWORK

Sections 73 and 74 are placed in Chapter XV, captioned “Demands and Recovery.” The relevant provisions are reproduced below for ready reference:

Section 73(1): Where it appears to the proper officer that any tax has not been paid or short paid or erroneously refunded, or ITC has been wrongly availed or utilised ……,” he shall serve notice… requiring the person to show cause.

Section 73(3): “Where a notice has been issued for any period under sub-section (1), the proper officer may serve a statement… for such periods other than those covered under sub-section (1).”

Section 73(4): “The service of such statement shall be deemed to be service of notice… subject to the condition that the grounds relied upon for such tax periods other than those covered under sub-section (1) are the same as mentioned in the earlier notice.”

Section 73(10): “The proper officer shall issue the order under sub-section (9) within three years from the due date for furnishing of annual return for the financial year to which the tax not paid or short paid or input tax credit wrongly availed or utilised relates to…”

Section 74 mirrors this structure with a five-year limitation in fraud cases. Sub-section (4) of Section 74 additionally provides that a statement under Section 74(3) for periods other than those in the notice shall be deemed a notice under Section 73(1) — i.e., a non-fraud notice — unless the ground of fraud is separately established for those additional periods. The meaning attributable to the phrase “any period” and “such periods” in the above provisions is at the core of the dispute.

Interestingly, sub-section (12) was inserted in both the above referred sections to specify that the provisions shall be applicable for determination of tax pertaining to the period up to Financial Year 2023-24. Thereafter, a new consolidated Section 74A was introduced to deal with demands pertaining to Financial Year 2024-25 onwards.

Judicial Interpretation requiring different SCNs for different financial years:

The Madras High Court in Titan Company Ltd. v. Joint Commissioner of GST & Central Excise4 examined the bunching of show cause notices for five assessment years from 2017-18 to 2021-22. The Court held that Section 73(10) of the Act specifically provides a time limit of three years from the due date for furnishing the annual return for the financial year to which the tax due relates. The limitation period is separately applicable for every assessment year, and it varies from one year to another. Relying on the Supreme Court’s decision in State of Jammu and Kashmir v. Caltex (India) Ltd5, the Court concluded that issuing bundled notices is an indirect attempt to circumvent the independent limitation periods, rendering the practice impermissible and liable to be quashed.

This reasoning was expanded by the Madras High Court in Ms RA And Co v. The Additional Commissioner of Central Taxes6. The Court undertook a conjoint reading of the definitions of “tax period” and “return”. It concluded that the GST Act treats each and every financial year as a separate unit. The Court held that “any period” in Section 73(3)/74(3) means a “tax period” (either monthly or yearly) and cannot extend beyond one financial year. The Court observed that bunching forces taxpayers into hardship, preventing them from availing amnesty schemes or compounding offenses for individual years without paying the aggregate demand for all years.

The Kerala High Court adopted a similar stance in M/s. Tharayil Medicals v. The Deputy Commissioner and Joint Commissioner v. M/s. Lakshmi Mobile Accessories7. The Division Bench in Tharayil Medicals emphasized that sub-sections (9) and (10) of Section 74 presuppose independent notices. The Court observed that an assessee is entitled to raise distinct and independent defences for different assessment years. Furthermore, the Court highlighted a critical prejudice: an assessing authority might club a period where the three-year limitation under Section 73 has expired into a consolidated notice under Section 74, bypassing mandatory limitations under the guise of a composite notice.

Following this trajectory, a Division Bench of the Bombay High Court in M/s. Milroc Good Earth Developers (supra) quashed consolidated show cause notices. The Court held that the GST scheme involves a definite tax period based on the filing of the return, and there is no scope for consolidating various financial years. This decision was subsequently applied by the Bombay High Court to quash several notices in cases like Rite Water Solutions and Bhawana Steel8. The Courts explicitly rejected the revenue’s defence that allegations of fraud permit consolidation, noting that fraud extends limitation to five years but does not authorize the clubbing of tax periods. The Andhra Pradesh High Court in S.J. Constructions9 concurred, holding that a single composite assessment order cannot be passed in relation to more than one financial year.

4. [2024] 159 taxmann.com 162 (Madras) 5 AIR 1966 SC 1350 6 [2025] 176 taxmann.com 731 (Madras) 7 [2025] 173 taxmann.com 867 (Kerala) & [2025] 170 taxmann.com 874/108 GST 762 respectively 8 [2026] 183 taxmann.com 627 (Bombay), [2026] 185 taxmann.com 22 (Bombay) 9 [2025] 178 taxmann.com 570 (AP)

CONFLICTING VIEWS PERMITTING CONSOLIDATED SCN FOR MULTIPLE YEARS

Conversely, an equally robust line of decisions has upheld the validity of consolidated notices, characterizing GST adjudication as a dispute-centric process rather than a periodic assessment.

The Delhi High Court addressed the issue in M/s. Mathur Polymers and Ambika Traders (supra). In Ambika Traders, dealing with an alleged fraudulent availment of Input Tax Credit (ITC) exceeding Rs. 83 crores between 2017 and 2021, the Court observed that the nature of ITC fraud requires analysing transactions spread across several years to establish the illegal modality. A solitary availment in one year may not establish the pattern. The Court focused on the legislative use of the phrases “for any period” and “for such periods” in Sections 73 and 74, distinguishing them from the term “financial year” used in the limitation clauses. It concluded that the statute does not prevent the issuance of a consolidated notice. Significantly, the Supreme Court dismissed the Special Leave Petition against the Mathur Polymers10 decision via a speaking order, observing that there was “no good ground and reason to interfere with the impugned judgment/order”.

10 [2026] 182 taxmann.com 215 (SC)

The Allahabad High Court provided a detailed analysis in M/s. S.A. Aromatics Pvt. Ltd’s case. The Court drew a sharp distinction between the return-based “assessment” procedures (found in Chapter XII) and the dispute-based “adjudication” procedures (found in Chapter XV). While assessments test the correctness of returns for a specific tax period, adjudication under Sections 73 and 74 focuses on specific disputes regarding tax short-paid or ITC wrongly availed. The Court noted that the legislature deliberately avoided conditioning Sections 73 and 74 within the limits of a “tax period”. Consequently, introducing the concept of a “unit of assessment” into adjudication proceedings would result in an artificial restriction not grounded in legislative language. The Court clarified that Section 73(10) and 74(10) refer only to time limitation; they do not govern the subject matter or scope of the notice itself.

The Karnataka High Court Division Bench in Chimney Hills Education Society11 recently overruled several Single Judge decisions of its own court that had previously prohibited consolidation. The Division Bench held that when the legislature consciously used the expression “any period” in Sections 73 and 74, it would be impermissible to read it restrictively as a single financial year. The Court addressed the argument regarding Form GST DRC-01, noting that while the form contains columns for “tax period”, the appended notes explicitly state that these columns are not mandatory, thereby negating the claim that the format confines the notice to a financial year.

Addressing the issue of prejudice and limitation, the Karnataka High Court ruled that a consolidated notice does not dilute the protection of limitation available under sub-section (10). Each financial year covered within the composite notice must independently satisfy the test of limitation. If the period for an earlier year is time-barred, that portion of the demand is liable to be dropped, but the consolidation itself does not enlarge the limitation or invalidate the entire notice. The High Court of Jammu & Kashmir in New Gee Enn & Sons12 also affirmed that bunching is permissible provided there is year-wise quantification, the allegations are not vague, and each period is within limitation.

11 2026 (5) TMI 125- KARNATAKA HIGH COURT 12 [2025] 181 taxmann.com 1

REFERENCE TO THE LARGER BENCH

Faced with these irreconcilable interpretations, the Division Bench of the Bombay High Court in M/s. Rollmet LLP’s case (supra) recognized the necessity of an authoritative resolution. While acknowledging that it would ordinarily be bound by the coordinate bench decision in Milroc Good Earth Developers, the Court expressed grave doubts regarding the legal correctness of that decision.

The Court in Rollmet LLP’s case observed that the legislative intent in providing sub-section (1) of Sections 73 and 74 was not to confine the proper officer’s authority to a single financial year. On a plain reading, sub-section (3) explicitly permits the issuance of a statement for a period other than the period covered under sub-section (1), indicating flexibility. The Court stated that interpreting sub-section (10)—which merely prescribes limitation for passing an order—as an embargo on the issuance of a consolidated show cause notice would amount to rewriting the provision. A limitation to pass an order is conceptually distinct from a limitation on the issuance of a notice.

Furthermore, the Court noted that the Central Board of Indirect Taxes and Customs (CBIC) issued a policy document on September 16, 2025, clarifying that the issuance of a consolidated notice is a procedural mechanism that does not extend the statutory timeline. Each year stands on its own footing for the purpose of calculating limitations. Recognizing the magnitude of the conflict, the Bombay High Court referred specific questions of law to a Larger Bench, including whether Section 73(10)/74(10) per se prohibits consolidation, and what legal position is brought about by the Supreme Court’s speaking order in Mathur Polymers.

ANALYSIS

“Tax Period” v/s “Any Period” – The first and primary concept which is undisputed is that the self-assessment scheme under the GST regime is for a “tax period”. Section 2(106) of the CGST Act defines “tax period” as “the period for which the return is required to be furnished.” Under Chapter IX, returns are furnished for each “calendar month” under Section 39(1), and for each financial year under Section 44 (Annual Return). Section 59 mandates self-assessment and return filing “for each tax period as specified under Section 39”. Limitation provisions in the assessment chapter — such as Section 62 for non-filers — are pegged to “the financial year to which the tax not paid relates.” Section 36 requires retention of books for 72 months from the due date of the annual return for that year. Section 16(4) also ties ITC entitlement to a specific financial year.

It is based on this concept the taxpayer argues that the provisions of S. 73/74 should be aligned with. Use of the phrase “any period” in the said section is statutorily tied to the monthly/ annual return which is self-assessed by the taxpayer. The scrutiny assessment and audit provisions which are a precursor to demand provisions are also performed on the tax period/ financial year wises basis.

In R A and Co’s case, Court viewed the return-based assessment scheme to be determinative of the demand provisions and held that show cause notice could be issued for “monthly” or “annual” return for the entire financial year or part thereof. If any return were to be filed for more than one financial year, then, based on the said returns, single show cause notice could be issued. However, under the GST Law, there is no requirement for filing any returns other than monthly and yearly returns. Hence, no show cause notice could be issued for more than one financial year. In addition, the phrase “such tax periods” mentioned in 73(4) would have an overbearing effect on the phrase “any periods” in the preceding provisions and hence to be interpreted as a financial year or part thereof. This view was also followed in Milroc’s case where court additionally noted that this synchronisation has been maintained during the insertion of S.74A which was applicable from financial year 2024-25 onwards rather than a specific date. Had the intention been otherwise, the provisions of section 74A would have been made effective for all show cause notices / orders passed after 01-11-2024 (being the effective date). This definitive action to demarcate operation of two demand provisions (73/74 v/s 74A) on a financial year basis establishes that the phrase “period” should be considered as a financial year or part thereof. In S J Constructions, taking cognizance of the dissenting opinion of Delhi Court (infra), the Court stated that any other view would adversely impact the right of the taxpayer to file appeals on a financial year basis or even claim amnesty u/s 128A for specific financial years.

The revenue countered this view and stated that the “period” referred in the said sections should be construed literally without additional words. The statute at multiple instances uses the phrase “tax periods” and “periods” distinctively. Where the intent of the law was to view the issue based on returns the phrase “tax period” has been used but where a general time frame was being fixed the phrase “period” has been used. Accordingly, “any period” under section 73/74 should not be narrowly understood to be limited to a financial year. Further, the said demand provisions bear their parentage from the central excise/ service tax law which spanned across financial years despite the returns being filed on a periodic basis. Assessment provisions which involve scrutiny of returns are to be viewed distinctly from adjudication provisions. Further, Audit provisions preceding adjudication provisions permit audit reports over multiple periods and hence corresponding demand notices should be aligned with such audit reports. In so far as the argument of separate provisions for amnesty are concerned, revenue argued that such schemes do not deter the taxpayer from claiming amnesty for the financial years covered under the scheme and hence their periodicity has no bearing in interpreting the adjudication provisions.

In S A Aromatics’s case, after taking into consideration all the earlier decisions, the Court affirmed revenue’s contention that the GST enactment is not direct extension of the assessment scheme envisaged under the Sales Tax era. While the self-assessment or re-assessment scheme may be assessment unit driven, adjudication provisions stand on different footing. Akin to the central excise system, sections 73 and 74 appear after Chapter XIII (pertaining to Audits) and Chapter XIV (pertaining to Inspection, Search, Seizure and Arrest). They are part of Chapter XV pertaining to Demand of Recovery. Yet, they deliberately do not begin with any word, phrase or sentence indicating that they are subject to assessment of tax liability for any specific tax period. The demand provisions refer to a dispute of a “specific tax amount” and NOT of a “specific tax period”. By very nature, the legislature has avoided conditioning adjudication proceedings within the limits of a ‘period’ or ‘tax period’ or to one Financial Year. Therefore, restricting the application to a singular financial based on annual return filing periods was unwarranted. It would be incorrect to apply assessment procedures and its concepts, to adjudication proceedings and distinction of issue-based procedures from return-based procedures permits the latter to span across financial years. Recently, the Karnataka High Court in Chimney Education society (supra) examined the entire audit/ special audit scheme which enabled multi-financial year frequency as a precursor to adjudication proceedings. The section 74A argument was negated by this Court that use of the financial year 2024-25 as a reference point does not change the statutory impact of section 74A(1) which continues to be issue-specific and also 74A(3) which is driven by the phrase “any period”.

TIME LIMITATION CONTROVERSY

Intricately tied to the controversy of clubbing of notices is the issue of determination of limitation period, since the said period is tied to a financial year. The time limitation to pass orders is the centre point for determination of issuance of a show cause notice. That being the case, the phrase “period” should be understood with reference to the limitation to pass orders for tax demands. This point was the primary reason for the Madras High Court in Titan Company to hold that bunching of show cause notices conflicted with the adjudication provisions. Reliance was placed on a Constitution Bench decision in Caltex (India) Ltd.’s case which held that sales tax being a transaction-based levy could be assessed even for a split period for which tax is leviable. Applying this principle the High Court stated that each and every assessment period would have a separate and independent period of limitation and could be split-up for assessment. Assuming a single limitation period for the entire block of 5 years would do injustice to the taxpayer. The taxpayer would be forced to be made answerable to an adjudication which would otherwise have independently been subjected to a longer time frame. For example, in view of an expiring time frame for 2017-18, a consolidated show cause notice would force the taxpayer to participate in an adjudication of 2021-22 which would otherwise expire much later. Thus, the taxpayer would be denied the opportunity to be adjudicated on year-by-year basis leading to compounded tax demands and pre-deposits (especially on recurring issues). Advancing this point further, in RA and Co case, the Court specifically noted section 128/ 138 provide for dispute resolution on a year-wise basis. Bunching show cause notice would prohibit a taxpayer to choose the years for dispute resolution and compel it to pay the taxes even for years where the demand is clearly unsustainable.

In Lakshmi Mobile Accessories, the Court claimed that consolidated show cause notices covering multiple financial/assessment years can be issued only in circumstances where the statutory provision provides for a “common period for initiation” and completion of the adjudication. Unlike the erstwhile Customs/Central Excise Act, the end termini for adjudication is pegged to annual return. The proximate expiry of the limitation period of one of the six financial/assessment years forces upon the taxpayer to argue all the financial years, and shortened time frame to adduce evidence. The statutory period available for an assessee to put forth its contentions against the show cause notice in an effective manner cannot be curtailed on premise of administrative efficiency.

The Kerala High Court in Tharayil Medicals’s case stated that in case of consolidated adjudication proceedings the taxpayer could be prejudiced w.r.t. application of provisions w.r.t fraud, suppression. The taxpayer may not be entitled to claim exclusion of those years/ issues were the elements of section 74 are admittedly absent. For example, suppression of sales turnover in Year-1 would be clubbed with simple GSTR-2A/3B difference in ITC in Year-1. Revenue would have the advantage of a larger time limitation u/s 74 for even the latter issue. Consequently, issuance of composite show cause notice covering multiple financial years making composite demand for multiple years without separate adjudication per year frustrate the limitation scheme

The revenue provided an equally emphatic counter to the above perspective. It was argued that consolidation of show cause notices does not amount to breaching the outer time limits under the said section. The earliest of the tax periods would be tested for determination of time limits. The protection available to taxpayers in terms of 75(2) r/w 73(10) would continue to be available for non-fraud cases even if the proceedings are initiated against it under section 74. Consolidation of financial years does not imply similar treatment to each financial year for assessment of fraud, etc. Though the limitation provisions are financial year driven, the notice issuing provisions are specifically delinked from the limits of a financial year. The Court in SA Aromatics’ case also examined taxpayer’s argument that if adjudication orders are guided by financial years, the notice provisions should necessarily be co-terminus or a smaller unit of assessment. Yet it affirmed revenue’s arguments and disregarded the strong argument that one show cause notice cannot result in two adjudication orders. With equally balanced substantive arguments, the machinery provision could provide some guidance in resolving such procedural controversy.

INTERPRETING “ANY PERIOD” THROUGH FORMS

Courts also had the occasion to examine the tax recovery forms (in DRC-01/03/07, etc) for understanding the scope of adjudication with reference to the “tax periods”. Proper officers record the tax period wise liability in DRC-01 and in DRC-07. These forms are designed to report the liability on a month-on-month which aggregate into a financial year total. Tax-payers are also reporting the tax payments in DRC-03 on a month-wise basis within a particular financial year. On linking Rule 142 with its parentage, it seems that the phrase “period” or “tax period” should be interpreted in a manner which aggregates into each financial year.

THE PORTAL DIMENSION: –

A dimension that the case law has not adequately engaged with — but which practitioners face daily — is the GST portal architecture and its treatment of demands, recoveries, and appeals. Form GST DRC-01 — the summary of show cause notice — contains a “Tax Period” field with a “From–To” date range alongside a “Financial Year” identifier, technically designed on a financial year basis. The portal uploads a DRC-01 for one financial year at a time, even where the underlying proceeding purports to cover multiple years. The DRC-03 framed under recovery provisions require tax period year-wise reporting which are aggregated to each financial year.

The Electronic Liability Register (in PMT) on the GST portal tracks demands period-wise, generating distinct annual return references, limitation markers, and demand tracking entries for each financial year. Taxpayers faced the challenge of filing separate appeals for even consolidated Order-in-Original. The administrative practice of a single OIO created the hurdle of uploading multiple DRC-07 for each financial year on the portal. The taxpayers were faced with a dilemma over whether a single appeal should be filed (basis the OIO) or separate appeals in APL-01 should be filed (basis year-wise DRC-07). Technical design prohibited the proper officer from issuing a consolidated DRC-07. This probably is indicative of the legal scheme of a financial year. It is only now that the GST portal has been redesigned permitting DRC-01/07 or APLs on a multi-year basis with year-wise breakup within each of the forms. The past proceedings continue to face the dichotomy of tax periods vis-à-vis any period controversy.

WAY FORWARD

The stake holders currently await the Larger Bench’s decision, which will likely serve as a springboard for definitive Supreme Court resolution. Even if the High Court rules against the consolidation of multiple financial years in single show cause notice, on a long-term basis, it may be difficult to prevent the revenue from pursuing a legitimate tax dispute and allow the taxpayer to sneak out through a technical argument. The GST council would certainly step in and regularise the earlier notices through a legislative amendment.

In the meantime, the GST council’s current position is that consolidated notices are legally permissible. Nevertheless, the genuine practical grievances raised by the tax-payers cannot be ignored. To harmonize administrative efficiency with natural justice, the executive must ensure that composite SCNs are meticulously bifurcated and quantify the demand on a strict “tax period basis”. The adjudicating authorities must rigorously sever time-barred components during the final hearing, and the GSTN portal’s architecture needs to be aligned for a year-wise severance of aggregated demands for the purposes of appeals and amnesties.