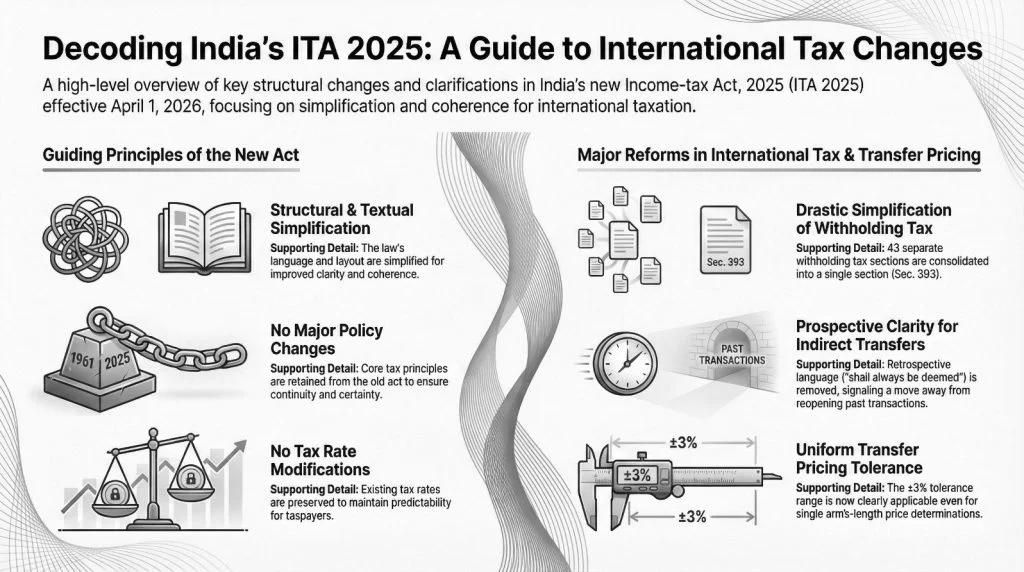

The Income Tax Act, 2025 (effective 1 April 2026) restructures the taxation of charitable and religious organisations while largely retaining the substantive framework of the 1961 Act. The concept of “trusts” is replaced by “registered non-profit organisations” (NPOs), with detailed eligibility and registration requirements under section 332. Provisions earlier treated as exemptions are now computation provisions, classifying income into regular, specified, and residual categories, with differential tax treatment. Anonymous donations, impermissible investments, and violations in commercial activity attract strict tax consequences, including 30% levy and possible cancellation of registration. Key exemptions, such as corpus donations and reinvested capital gains, remain, while accumulations are permitted for up to five years. Compliance obligations relating to books, audit, returns, and investments are tightened, with harsher penalties for violations. The exit tax on accreted income and donation approval rules under section 133 also continue. Despite restructuring, complexity persists, raising risks of litigation

The Income Tax Act 2025 (“new Act”), which comes into force from 1st April 2026, has by and large retained the substance of the manner of taxation of charitable and religious organisations as existed in the Income Tax Act, 1961 (“existing Act”), but has significantly changed the structure of the provisions relating to taxation of charitable and religious organisations.

At the stage of the draft Bill, there had been a few major changes suggested in the provisions – withdrawal of the exemption for reinvestment of capital gains [current s.11(1A)] and of the option to spend the income in the subsequent year [current explanation to s.11(1)], extending the taxability of anonymous donations to all charitable-cum-religious trusts are some of the proposals. Fortunately, at the time of passing the Revised Bill, these proposals were withdrawn, and the existing exemptions broadly continue to operate.

In this article, an attempt is being made to analyse how the new provisions need to be read, and some of the changes that may apply on account of the changed structure of the law or changes in the language of the new law. While all major aspects are sought to be covered, it may not be possible to cover all the provisions, which run into 21 pages of the new Act, besides the items contained in the Schedules.

The new provisions are contained in part B of Chapter XVII, which consists of 7 sub-parts – registration, Income of regd NPO, commercial activities by regd NPOs, compliances, violations, approval for purposes of section 133, and interpretation.

1. SIGNIFICANT CHANGES

The significant changes to the structure are analysed below:

1. The concept of a trust or institution holding property in trust for charitable or religious purposes has been replaced by a concept of registered non-profit organisation (“regd NPO”). A list of types of entities which can apply for registration as a regd NPO is laid down in s.332(1), which was not present in the current ITA. These are:

(a) A public trust;

(b) A society registered under Societies Registration Act, 1860 or under any law in force in India;

(c) A company registered under s.8 of Companies Act 2013 or under s.25 of Companies Act 1956 and deemed to have been registered under s.465(2)(g) of Companies Act 2013;

(d) A University established by law or any other educational institution affiliated thereto or recognized by the Government;

(e)An institution financed wholly or in part by the Government or a local authority;

(f) Investor Protection Funds set up by recognized stock exchanges, commodity exchanges or depositories, notified bodies administering any activity for the benefit of the general public, Prime Minister’s National Relief Fund, PM CARES Fund, Chief Minister’s Relief Fund, Swachh Bharat Kosh, Clean Ganga Fund, university/educational institutions and hospitals/medical institutions wholly or substantially financed by the Government or with annual receipts of less than Rs 5 crore, and notified bodies set up under a Central/State Act for dealing with housing accommodation, planning, development or improvement of cities, towns and villages, regulating or regulating and developing any activity for the benefit of the general public or regulating any matter for the benefit of the general public;

(g) Any other person notified by the CBDT.

Section 332(2) provides that such a person shall be eligible for registration if:

(a) It is constituted, registered or incorporated in India for carrying out one or more charitable purposes, or one or more public religious purposes, and

(b) The properties of such person are held for the benefit of the general public under an irrevocable trust –

i. Wholly for charitable or religious purposes in India; or

ii. Partly for charitable or religious purposes in India, if such person was constituted, registered or incorporated prior to 1.4.1962.

Therefore, a trust created after 1.4.1962 cannot apply for registration as a regd NPO if it is not constituted, registered or incorporated in India or any of its objects are for the benefit of the public or any persons outside India. This requirement is not contained in the current Act. This also seems to contradict the provisions of section 338 (analysed later), where income can be applied outside India with the prior approval of the CBDT. One fails to understand how an NPO can apply income outside India, if it does not have such an object permitting application outside India, in which case it would not be eligible for registration.

Further, in case of an NPO set up after 1.4.1962, it can only be wholly for charitable and religious purposes, as is the case under the existing law.

2. The earlier provisions of exemption contained in sections 10 and sections 11 to 13 were contained in Chapter III – Incomes which do not Form Part of Total Income. These were therefore exemption provisions. Under the new Act, the provisions are contained in sections 332 to 355, which are contained in Part B – Special Provisions for Registered Non-Profit Organisations of Chapter XVII – Special Provisions Relating to Certain Persons. These are now therefore computation provisions, and not exemption provisions. Certain specific provisions, such as those contained in clauses (iiiab), (iiiac), (iiiad) and (iiiae) of section 10(23C) continue as complete exemptions, being part of Schedule III, read with section 11 of the new Act, which deals with incomes not to be included in total income.

The switchover from a scheme of exemption to a scheme of computation may not have any significant impact, given that:

(a) the provisions of section 14 (current section 14A) relating to disallowance of expenditure incurred for earning exempt income apply for the purposes of computing income under Chapter IV (i.e. under the heads of income) and not under Chapter XVII-B; and

(b) the provisions of Alternate Minimum Tax under section 206 specifically provide for reduction of “regular income” of a regd NPO referred to in section 355 from the profits as per profit and loss account, in the definition of “book profit” in section 206(1)(c).

3. The exemption provisions contained for some specific types of important institutions, educational and medical institutions in clauses (iv), (v), (vi) and (via) of section 10(23C) have been merged with the general computation provisions for regd NPOs. Therefore, there is now only one regime of computation for regd NPOs under the new Act, as opposed to two exemption regimes under the current Act. A beginning for the merger of the two regimes had been made earlier under the current Act, by providing that with effect from 1.10.2024, no application for renewal of s.10(23C) approval would be made under that section, but would have to be made under section 12A, and by bringing the two exemption regimes almost on par with each other. Section 355(g) of the new Act provides that an approval under section 10(23C) would be a registration for the purposes of the new Act, and therefore an entity approved under section 10(23C) would be a regd NPO under the new Act.

4. Instead of all income from property held under trust, including donations, being considered for computation of exemption, and with loss of exemption for certain incomes under sections 11(3), 13 or section 115BBC, incomes of a trust would now be categorised into 3 categories – regular income (85% of which is required to be applied), specified income (which is taxable at a flat rate of 30%) and residual income.

“Regular income” is defined in section 335 as:

(a) Income from any charitable or religious activity for which the NPO is registered, carried out by it in such tax year;

(b) Income derived from any property, deposit or investment held wholly for charitable or religious purposes by such regd NPO in such tax year;

(c) Income derived from any property, deposit or investment held in part for religious and charitable purposes by NPOs set up prior to 1.4.1962;

(d) Voluntary contributions received by such regd NPO in such tax year; and

(e) Gains of any permitted commercial activity carried out by such regd NPO in such tax year.

In the draft Bill, the word “receipts” had been used in place of the word “income” in items (a), (b) and (c), and in (b), the term used was “receipts, whether capital or revenue”. Fortunately, the language in the new Act has been rectified, with the term used now being “income”.

“Specified income” consists of anonymous donations and income which was so far taxable under section 115BBI, and includes the following:

(a) Taxable anonymous donations;

(b) Income applied for the benefit of specified persons;

(c) Income applied outside India without CBDT approval;

(d) Investment made in contravention of permitted investment pattern;

(e)Accumulated income, applied to purposes other than purposes of accumulation, or ceasing to be accumulated or set apart, or not applied within the period of accumulation, or credited or paid to another regd NPO;

(f) Income applied to purposes other than purposes for which it is registered;

(g) Business income determined by the AO in excess of income shown in books of account of the business undertaking.

Here too, in the draft Bill, the scope of anonymous donations had been proposed to include all anonymous donations received by a charitable-cum-religious trust. The new Act finally covers only anonymous donations received for a university/educational institution or hospital/medical/institution by such religious-cum-charitable trusts, besides all anonymous donations received by a charitable trust, as is the position under the current Act. Anonymous donations received by religious trusts continue to remain outside the purview of taxation as anonymous donations.

“Residual Income” is defined in section 355(j) to mean the total income without giving effect to the provisions of Part B of Chapter XVII, as reduced by regular income and specified income. Incidentally, the term “total income” is not defined in this Chapter. Section 2(108) defines total income as the total amount of income referred to in section 5, computed in the manner as laid down under this Act. Given that the headwise computation provisions would not apply (as discussed below), this would probably mean the sum total of all the incomes as computed after deductions and exclusions under Part B of Chapter XVII.

2. REGISTRATION

The provisions for registration of an NPO are contained in section 332(3), and are identical to those currently applicable under section 12A(1)(ac). Section 332(3) has a table listing out the 7 types of cases [currently found in clauses (i) to (vi)(A) and (B) of current section 12A(1)(ac)], giving the time limit for furnishing the application, time limit for passing the order by the CIT, and the period of validity of registration. The enhanced period of registration of 10 years for small NPOs having gross income of less than ₹5 crores in each of the preceding two years, introduced by the Finance Act 2025, has also been provided for in section 332(5).

As under the current Act, the CIT has been empowered to condone delay in making of the application if he finds that it was for a reasonable cause. There is now a specific provision in section 332(6) to the effect that if an application for registration is not made within the specified time and the delay in filing such application is not condoned, the NPO shall be liable to pay tax on accreted income under section 352.

The provisions of current section 11(7), which prohibit claim of exemption under section 10 except certain specific sub-sections, and which provide a regime for one-time switchover from section 10(23C) to section 11, are continued in section 333.

3. CANCELLATION OF REGISTRATION

Section 12AB(4) of the current Act lists out the “specified violations” on the noticing of which, the CIT can cancel the registration of a trust, and the procedures for the same. Section 12AB(5) provides the time limit within which such order of cancellation, or refusal of cancellation, has to be passed.

Section 351 of the new Act now contains these provisions relating to specified violations, the procedure to be followed for cancellation and the time limits for passing of order by the CIT.

The list of specified violations is identical, except that it now covers violation of section 346. Section 346 deals with commercial activity by GPU trusts, and prohibits such activity unless carried out in course of GPU objects, aggregate receipts from such activity do not exceed 20% of total receipts of the regd NPO and separate books of account are maintained for such commercial activity. Therefore, if the receipts from commercial activity of a GPU trust exceed 20% of the aggregate receipts, this can result in cancellation of registration, which was not the position under the current Act.

4. COMPUTATION OF INCOME AND TAX LIABILITY

Section 334 provides that the tax payable by a regd NPO on its total income for a tax year shall be the aggregate of tax calculated at 30% of the specified income and calculated at the applicable rate for taxable regular income and residual income for the tax year.

As per section 334(2), the provisions of Chapter XVII would override all other provisions of the new Act, except the clubbing provisions contained in sections 96 to 98 of the new Act. Therefore, the computation provisions contained under the respective heads of income would not apply to a regd NPO. This is similar to the position prevailing under the current Act, where the CBDT had clarified vide its Circular No. 5-P (LXX-6) dated 19th June, 1968, that the income, for the purpose of computation of exemption, has to be taken on a commercial basis (as per books of account). One area of difference from the current Act would be in a situation where the entire income of the regd NPO is not exempt from tax, the income would be computed and taxed under this Chapter. Under the current Act, in some Tribunal decisions, a view had been taken that income which was not exempt was to be computed under the respective heads of income.

This would also mean that the tax computation contained in section 334 would apply irrespective of the nature of income. For instance, the tax on long term capital gains would be as per the provisions of section 334, and not at the rate of 12.5% prescribed under section 197 (section 112 of the current Act). Section 334 refers to the rate applicable on taxable regular income and any residual income. This rate is not spelt out in the new Act – it would probably be prescribed under the Finance Act each year. But, in case the regd NPO is a company, it will not be eligible for the concessional rate of tax for companies under section 200 (section 115BAA of the current Act).

A. Taxable Regular Income

Section 336 defines taxable regular income. Taxable regular income is nil, where 85% or more of the regular income has been applied or accumulated for charitable or religious purposes. Where less than 85% of the regular income has been applied or accumulated, the taxable regular income would be 85% of the regular income, less income applied for charitable or religious purposes or accumulated.

Voluntary contributions received by a regd NPO are included in the definition of income under section 2(49)(c).

B. Deemed Accumulated Income

This 15% of regular income (or unspent amount up to 15% where more than 85% of the regular income is spent), is treated as deemed accumulated income [section 343(1)]. As per the draft Bill, such deemed accumulated income was to be invested in modes permitted under section 350. This could have created difficulty, as such amount may not necessarily be available with the regd NPO (e.g. if 100 is donated to another regd NPO, 85% is treated as application and balance 15% may fall under deemed accumulation, but would not be available for investment, having already been donated). Fortunately, in the new Act, the provision is that if invested, it has to be invested in modes permitted under section 350 [current section 11(5)]. In other words, such investment is not mandatory, but only the modes of investment are mandatory. It is specifically provided in section 343(2) that deemed accumulated income is different from accumulated income under section 342 [current section 11(2)].

C. Exclusions from Regular Income

Section 338 provides that certain incomes shall not be included in the regular income. These are:

(a) Income applied outside India where the CBDT has directed that such income shall not be included in the total income (i.e. income applied outside India with the approval of the CBDT). This approval can be granted for an NPO created before 1st April 1952 for charitable or religious purposes, or for an NPO created on or after 1st April 1952 for charitable purposes where such application of income outside India tend to promote international welfare in which India is interested.

(b) Corpus donations received by the regd NPO.

The language of the new Act in effect settles the controversy existing under the current Act as to whether, to claim exemption, the application has to be in India or charitable purposes has to be in India. The current Act uses the phrase “applied to such purposes in India”, which gave rise to this controversy. The Delhi High Court in National Association of Software & Services Companies, 345 ITR 362, had held that the application had to be in India, while the Karnataka High Court in Ohio University Christ College, 408 ITR 352, had held that the exemption was available if the purposes was in India. Since the new Act uses the term “income applied outside India”, where any application of income is to be made outside India, it would be excluded from income only if prior CBDT approval is obtained for such expenditure.

The exclusion of such income applied outside India (with CBDT approval) and corpus donations, implies that such incomes would not be considered for computing the deemed accumulated income of 15% (i.e. for computing 85% of regular income) in determining the taxable regular income.

D. Corpus Donations

“Corpus donation” is defined in section 339 to mean any donation made with a specific direction that it shall form part of the corpus of the regd NPO, provided that such donation is invested or deposited in one of the modes permitted under section 350 maintained specifically for such corpus. This is similar to the current section 11(1)(d), which requires investment of corpus donations in permitted modes and earmarking of investments.

E. Application of Income

What is considered as allowable application of income is contained in section 341. Sums applied for charitable or religious purposes in India for which the NPO is registered and paid during the year, are allowable as application of income. In case of donations paid to another regd NPO, 85% of the donations are allowable. If such donations are towards the corpus of the other regd NPO, the donation will not be allowable as application of income. As under the current Act, adjustments are required to be made for payments made out of corpus or out of loans or borrowings (not to be considered in the year of payment), and reinvestment back in corpus investments or repayment of such loan or borrowing (to be considered as application in the year of reinvestment or repayment). Cash payments exceeding ₹10,000 and amounts on which TDS which was deductible, but are not deducted, are not allowable as application of income. Similarly, deficit of earlier years is also not allowable as an application of income.

F. Deemed Application of Income- Option to Spend and Capital Gains

The option to spend income in subsequent year (or the year of receipt of income), currently contained in the explanation to section 11(1), which was proposed to be done away with in the draft Bill, has been finally retained in the new Act. This is contained in section 341(5), and is deemed to be an application of income. Similarly, the exemption for capital gains, currently in section 11(1A) of the current Act, which was also sought to be removed in the draft Bill, has been retained in the new Act. It will now be treated as a deemed application under section 341(9). Interestingly, while sub-section (8) of section 341 provides that application under sub-section (1) shall include deemed application where option is exercised under sub-section (5), similar provision is absent in respect of deemed application under sub-section (9) in respect of capital gains. However, the absence of such specific provision should not impact the allowability of capital gains as a deduction in computing taxable regular income.

G. Accumulated Income

As under the current Act, under the new Act also, a regd NPO has the option to accumulate its regular income for a period of up to 5 years. Here also, a form has to be filed stating the purpose and period of accumulation. The amount of accumulation has also to be invested in the modes permitted under section 350, as under the current Act.

Under the current Act, there has been a controversy raging for the last 34 years as to what can be stated to be the purposes of accumulation – whether some or all of the objects of the trust can be stated to be the purposes of accumulation has been a matter of litigation. Unfortunately, this controversy may continue even under the new law, given that it also does not bring about clarity on the issue.

On the contrary, a new issue could arise as to whether the accumulation can only be for a single purpose or whether it can be for multiple purposes, as permitted under the current law. This issue is on account of the use of the word in singular “purpose” in the new Act and not the plural “purposes” as in the current Act. It appears that the intention is not to restrict it to a single purpose, as the objective of the new Act is merely to use simpler language and not to bring about policy changes.

In the new Act also, change in purpose is permissible with the approval of the Assessing Officer (“AO”). Besides, the amount of accumulation cannot be utilized by donating to another regd NPO as under the current Act. Similarly, as under the current Act, on dissolution of the regd NPO, an application can be made to the AO to donate the amount of application to another regd NPO.

As mentioned earlier, the unspent accumulation or accumulation ceasing to be kept apart or that is donated to another regd NPO would be taxable as specified income.

5. COMMERCIAL ACTIVITY

Section 11(4) of the current Act applies to a business undertaking held in trust, and provides that the term “property held under trust” includes a business undertaking so held. Courts have taken the view that section 11(4) applied to a situation where the business itself was held in trust, while section 11(4A) applied in other cases where business was carried on. Therefore, the requirements of section 11(4A) of incidental business and separate books of account did not apply to cases covered by section 11(4). Section 344 of the new Act corresponds to section 11(4). It provides that where the property held by a regd NPO includes a business undertaking, and if a claim is made for benefits under these provisions, then the AO has the power to determine the income of such business undertaking as per the provisions of the new Act. The definition of “specified income” includes the addition made by the AO to the book income of such business undertaking – only the book income would qualify as regular income, eligible for deduction of application, deemed application and accumulation of income.

Under the current Act, the proviso to section 2(15) used the term “activity in the nature of trade, commerce or business or activity of rendering any service in relation to trade, commerce or business”. This applied only to trusts engaged in the object of advancement of general public utility (GPU trusts). Section 11(4A) used the term “business”. Section 11(4A) applies to both GPU trusts as well as non-GPU trusts. There was accordingly a distinction between the proviso to section 2(15), which uses broader terminology, and section 11(4A), which uses the term “business”. The new Act uses the term “commercial activity” in the context of both of these, and does not distinguish between these.

The term “commercial activity” has been defined in section 355(e) as means any activity in the nature of trade, commerce or business, or any activity of rendering any service in relation to trade, commerce or business, for a cess or fee or any other consideration, irrespective of the nature of use or application or retention of the income from such activity. This is identical to the language of the current proviso to section 2(15), which was interpreted by the Supreme Court in the case of ACIT(E) vs. Ahmedabad Urban Development Authority [2022] 449 ITR 1 (SC). In that case, the Supreme Court held that any activity in furtherance of GPU objects where there was substantial mark up over cost would be regarded as in the nature of trade, commerce or business.

Two sections apply to trusts carrying on commercial activity – section 346 deals with GPU trusts, and section 345 deals with non-GPU trusts. In case of GPU trusts, the position under section 346 is the same as was earlier prevalent under the proviso to section 2(15). It provides that a regd NPO, carrying on advancement of any other object of general public utility, shall not carry out any commercial activity unless:

(a) Such commercial activity is undertaken in the course of actual carrying out of advancement of any object of general public utility;

(b) The aggregate receipts from such commercial activity/activities do not exceed 20% of the total receipts of such regd NPO of the relevant tax year; and

(c) Separate books of account are maintained by such regd NPO for such activities.

Section 345, applicable to non-GPU trusts or activities, provides that a regd NPO (other than that referred to in section 346) shall not carry out any commercial activity, unless:

(a) Such commercial activity is incidental to the attainment of the objectives of the regd NPO; and

(b) Separate books of account are maintained for such activities.

Section 345 was meant to be the equivalent of section 11(4A), with the difference that section 11(4A) as applicable to GPU trusts has been incorporated in section 346. However, section 11(4A) used the term “business”, as opposed to the term “activity in the nature of trade, commerce or business or activity of rendering any service in relation to any trade, commerce or business”, which is a much broader term. Given that the same definition of “commercial activity” would apply to both section 346 (GPU trusts) as well as section 345 (non-GPU trusts), which definition is identical to that contained in the current proviso to section 2(15), it appears that the same meaning which earlier applied only to GPU trusts would now apply to non-GPU trusts as well. The interpretation of the Supreme Court in the case of Ahmedabad Urban Development Authority (supra) may now apply not only to GPU trusts, but also to non-GPU trusts. Therefore, some activities of non-GPU trusts, which resulted in surplus but were not considered as business for the purposes of section 11(4A), may now be covered by section 345. This would require maintenance of separate books of account for such activities.

What are the consequences of violation of sections 345 or 346? Violation of either of these provisions is regarded as a “specified violation” under section 351(1)(b), which can result in cancellation of registration of the NPO. Under the current Act, while violation of section 11(4A) is a “specified violation”, which can attract cancellation of registration, applicability of the proviso to section 2(15) is not such a specified violation and does not result in cancellation of registration. Therefore, under the new Act, if a regd NPO carries on a GPU activity which results in substantial surplus, and the gross receipts from such activity exceeds 20% of the total receipts of the NPO, its registration can be cancelled, with consequent applicability of tax on accreted income. This is a drastic change from the current position, where there is only a loss of exemption for the year. This seems to be an unintended consequence of merger of the proviso to section 2(15) with section 11(4A) in so far as GPU NPOs are concerned.

Besides, currently, section 13(8) read with section 13(10) provides that in case the proviso to section 2(15) is attracted, while exemption would not be available, only the net income of the trust would be taxable. Section 353(1), corresponding to current section 13(10), provides for taxation of net income of a GPU trust which has violated section 346. However, there is no similar provision for violation of section 345 by a non-GPU trust, which may suffer tax on its gross income.

6. COMPLIANCES

A. Books of Account

Currently, the exemption under sections 11 and 12 is subject to the requirements of section 12A. Clause (b)(i) of section 12A requires the maintenance of books and other documents in the form and manner and at the place, as may be prescribed, where the income exceeds the maximum amount not chargeable to tax. Violation of this condition can result in loss of tax exemption for the relevant year.

Under the new Act, section 347 contains the requirement to maintain the books of accounts and other documents in prescribed form and manner and at the prescribed place. Section 353 provides that the consequence of failure to maintain books of account under section 347 shall be that the regular income as reduced by the expenditure referred to in section 353(3) shall be the taxable regular income, i.e. in other words, the benefit of accumulation, deemed accumulation, deduction for capital expenditure, corpus donations and donations to other NPOs shall not be available. It may be noted that the consequence is only for failure to maintain books of account, and not failure to maintain other documents.

B. Audit

Similarly, current section 12A(b) requires accounts to be audited if the income is above the income exemption threshold limit and the audit report to be filed, in order to get the benefit of exemption. This requirement of audit is now contained in section 348, with the consequences of failure to get books of account audited contained in section 353(1) being taxation of net income without certain deductions, similar to the consequences

of failure to maintain books of account. Here also, section 353(1) is attracted only for failure to get the books of account audited, and not for failure to furnish audit report.

C. Return of Income

Under the current Act, under section 139(4A), a charitable or religious trust claiming exemption under section 11 is required to file a return of income, if its income (before exemption under sections 11 & 12) exceeds the threshold exemption limit. This obligation is now contained in section 263(1)(iii) of the new Act, which requires a person other than a company or a firm to file its return of income if its income (before giving effect to provisions of Chapter XVII-B) exceeds the maximum amount not chargeable to tax (“threshold limit”). Current section 139(4C)(e) also requires institutions claiming exemption under clauses (iiiab), (iiiac), (iiiad), (iiiae), (iv), (v), (vi) and (via) of section 10(23C) to file their returns of income. Educational and medical institutions falling under the current clauses (iiiab), (iiiac), (iiiad), and (iiiae) of section 10(23C) would fall within the definition of “specified entity” under the new section 263(1)(iv) and will also be subject to the same obligation. There are no separate exemptions under the new Act corresponding to clauses (iv), (v), (vi) and (via) of the current Act, and these would therefore fall within the general exemption for regd NPOs, also covered by section 263(1)(iii).

Section 349 of the new Act provides that where the total income of a regd NPO exceeds the threshold limit, it has to furnish the return of income as per the provisions of section 263(1)(a)(iii) and (2), within the time limit allowed under section 263(1)(c). This time limit continues to be 31st October for persons whose accounts are required to be audited. Under the current Act, trusts are permitted to file returns within the time limits specified in sub-sections (1) and (4) of section 139 – i.e. even belated returns are permitted.

Section 353 provides that where any regd NPO fails to furnish its return under section 349, its taxable regular income shall be the net income without certain deductions (the same as in cases of failure to maintain books of account or failure to get books of account audited). Would this cover only cases of failure to file the return of income, or even delay in filing the return of income? While section 353 refers only to failure to file a return under section 349, section 349 requires the return to be filed within the time allowed under section 263(1)(c). Therefore, even cases of delay may invite applicability of these provisions, unlike under the current law where filing of a belated return of income within the time limit under section 139(4) does not attract such consequence.

D. Permitted Modes of Investment

Section 350(1) of the new Act provides that the modes of investing or depositing the money under Chapter XVII-B shall be those specified in Schedule XVI. Section 350(2) further permits notification by the Central Government of other modes of investing or depositing money.

Schedule XVI lists out all the modes currently listed in section 11(5), including immovable property.

It even includes the other modes notified for the purposes of section 11(5) under rule 17C, such as units of mutual funds, equity shares of a depository, equity shares of an incubatee by an incubator, units of Powergrid Infrastructure Investment Trust, etc.

The permissible investments/deposits list in this Schedule also contains the exceptions which are currently listed under section 13(1)(d) and under clause (b) of the third proviso to section 10 (23C), such as:

(a) Assets held as part of the corpus as at 1st June 1973;

(b) Equity shares of a public company held by a university/educational institution/hospital/ medical institution as part of the corpus as of 1st June 1998;

(c) Bonus shares allotted on such shares held as corpus;

(d) Donations received and maintained in the form of jewellery, furniture or any other notified article;

(e) Any asset, other than those permitted under other clauses of this Schedule, if not held beyond one year from the end of the year in which the asset was acquired;

(f) Funds representing profits and gains of business.

Schedule XVI also has an interpretation clause, where various terms used in the Schedule are defined.

The consequences of violation of the provisions of section 350 are contained in S.No.4 of the table of specified income in section 337. It provides that any investment or deposit made in contravention of the provisions of section 350 out of any income, accumulated income, deemed accumulated income, corpus, deemed corpus or any other fund would be taxable as specified income in the year in which such investment or deposit is made.

Under the current provisions of section 13(1)(d), while exemption was lost on account of the impermissible investment to the extent of the impermissible investment, such loss of exemption could only be to the extent of income for the year. Therefore, if the gross income of the trust for the year was Rs 10 lakh, and an impermissible investment of Rs 1 crore was made out of the corpus or past accumulation, the income that could be taxed so far was only Rs 10 lakh (income for that year which suffered loss of exemption). Under the new Act, the entire Rs 1 crore would be treated as specified income and taxed at 30%. The consequences under the new Act are therefore far more stringent.

7. TAX ON ACCRETED INCOME

The provisions for tax on accreted income, a form of exit tax, currently contained in Chapter XII-EB, sections 115TD to 115TF, are now also part of Chapter XVII-B, being contained in section 352. The computation of accreted income is set out in the form of a formula in section 352(2). Section 352(4) contains a table specifying the cases attracting tax on accreted income, the specified date on which accreted income is to be computed, and the due date for payment of tax on accreted income in each case.

Delay in filing an application for renewal of registration continues to attract tax on accreted income, as under the current Act.

8. APPROVAL FOR PURPOSES OF SECTION 133 (CURRENT SECTION 80G)

The provisions for approval for purposes of section 133 (corresponding to section 80G of the current Act) is also contained in Chapter XVII-B in section 354. The conditions for such registration under the new section 354 are the same as those contained in section 80G(5), except that the condition contained in clause (i) that the income is not liable to income tax by virtue of section 11 and 12 or section 10(23C) is omitted.

Section 354(2) contains a table, stating the types of cases, time limits for furnishing application, time limit for passing the order and validity of approval in each case. These are the same as those contained in the current Act.

The requirement of filing a statement of donations and for furnishing a certificate to the donor in respect of such donations continues under the new Act.

9. PENALTY & FEES

The existing penalty and fees applicable to religious and charitable trusts continue under the new Act – penalty for provision of benefit to related persons (current section 271AAE, new section 445), penalty for failure to deliver statement of donations or furnish certificate to donors (current section 271K, new section 464), and fees for failure to deliver statement of donations or certificate to donors within time (current section 234G, new section 429).

CONCLUSION

All in all, while the general provisions relating to charitable and religious organisations have remained broadly the same, the manner in which some of the changes have been carried out could possibly cause difficulty in some cases. One hopes that these are just drafting mistakes, which will be corrected in the forthcoming Budget.

However, the complexity of the provisions and procedures relating to regd NPOs still continues, with harsh consequences for even minor mistakes. Under such circumstances, unless the provisions are really simplified and made more reasonable, the large scale litigation in this area of income tax is likely to continue.