A. NOTIFICATIONS

i) Notification No.7/2025-Central Tax dated 23rd January, 2025

By above notification the amendments are made in CGST Rules regarding grant of temporary identification number.

ii) Notification No.8/2025-Central Tax dated 23rd January, 2025

By above notification waiver for late fees for GSTR-9 is provided.

iii) Notification No.9/2025-Central Tax dated 11th February, 2025

By above notification, date of coming into force of rules 2, 8, 24, 27, 32, 37, 38 of the CGST (Amendment) Rules, 2024 is specified.

B. CIRCULARS

(i) Clarification on regularising payment of GST on co-insurance premium — Circular no.244/01/2025-GST dated 28th January, 2025.

By above circular the clarification is given regarding regularizing payment of GST on co-insurance premium apportioned by the lead insurer to the co-insurer and on ceding / re-insurance commission deducted from the reinsurance premium paid by the insurer to the reinsurer.

(ii) Clarification on applicability of GST on certain services — Circular no.245/02/2025-GST dated 28th January, 2025.

By above circular, clarifications regarding applicability of GST on certain services are given.

(iii) Clarification on late fees — Circular no.246/03/2025-GST dated 30th January, 2025.

By above circular, clarification is given about applicability of late fee for delay in furnishing of FORM GSTR-9C.

C. INSTRUCTIONS

(i) The CBIC has issued instruction No.2/2025-GST dated 7th February, 2025 by which instruction is given about procedure to be followed in department appeal filed against interest and/or penalty only, with relation to Section 128A of the CGST Act, 2017.

D. ADVANCE RULINGS

Classification – Instant Mix Flour

Ramdev Food Products Pvt. Ltd. (AAR Order No. GUJ/GAAAR/APPEAL/2025/01 (IN APPLICATION NO. Advance Ruling/SGST&CGST/2021/AR/17) Dated: 22nd January, 2025)(GUJ)

The present appeal was filed against the Advance Ruling No. GUJ/GAAR/R/29/2021 dated 19th July, 2021, passed by the Gujarat Authority for Advance Ruling [GAAR].

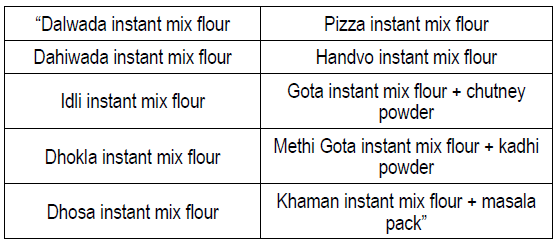

The appellant is engaged in the business of manufacture and supply of the below mentioned ten instant mix flours viz.

The process undertaken for manufacturing & selling the above products was explained as under:

“(a) that they purchase food grains and pulses from vendors.

(b) that such food grains/pulses are fumigated and cleaned for removal of wastage.

(c) that food grains/pulses are then grinded and converted into flour.

(d) that flour is sieved for removal of impurities.

(e) that flour is then mixed with other ancillary ingredients such as salt, spices, etc. The proportion of flour in most of the instant mixes is ranging from 70% to 90%.

(f) that flour mix is then subjected to quality inspection and testing.

(g) that flour mix is thereafter packaged and stored for dispatch.”

The table showing constituent components of instant mix flour was also submitted. The constituents included dried Leguminous Vegetable Flours, Rice & Wheat Flours, Additives, Spices etc.

The appellant’s submission was that the instant flour mix retains its identity as flour and therefore they are classifiable under heading 1101, 1102 or 1106, as the case may be, based on the dominant flour component.

With above information, appellant has sought ruling about classification of above products.

The ld. AAR has ruled that above products merits classification at HSN 2106 90 attracting 18 per cent GST as per Sl. No. 23 of Schedule III to the Notification No.01/2017-Central Tax (Rate) dated 28th June, 2017.

The instant appeal was against the above ruling. The appellant reiterated its contentions about products being covered by heading 1101, 1102 or 1106 and liable to tax @ 5 per cent.

The appellant supported its contentions mainly on ground that the instant mix are mixture of flours like Black Gram (Urad Dal) and / or Rice and / or Refined Wheat flour and / or Bengal Gram (Chana Dal) and / or Green Gram (Moong Dal) with addition of very small amount of additives like iodised Salt and / or Sugar and/or Acidity regulator (Citric acid INS 330) and / or Raising agent (Sodium bicarbonate INS 500(ii)) and that it does not contain any spices and hence should be covered as flours under Chapter 11 and liable to GST @ 5 per cent;

The ld. AAAR referred to heading 1101, 1102 and 1106 and also Explanatory notes to HSN in respect of heading 1101 and 1102.

After referring to headings in detail, the ld. AAAR observed that the classification of the product is required to be determined in accordance with the terms of the headings. As per chapter heading 1106, it covers Flour, Meal and Powder of the dried leguminous vegetables of Chapter Heading 07.13 and other specified products. The ld. AAAR further observed that as the products of the appellant contain other ingredients like Iodised salt, Acidity regulator (INS 330), Raising agent (INS 500(ii)) in different proportions, which are not mentioned in the chapter heading 1106 or the relevant explanatory notes of HSN, the said products are not covered under Chapter Heading 1106.

The contention about classification under chapter heading 1101 and 1102 also rejected by the ld. AAAR observing that even if flour improved by adding of small quantity of specified substance remains under such heading the same will not be correct when substances (other than specified substances) are added to the flours with a view to use as ‘food preparations’, and said flour gets excluded from chapter heading 1101 or 1102.

The reliance of appellant on VAT determination order also held not applicable in view of change in classification entries.

Finally, the ld. AAAR approved the classification done by ld. AAR and rejected the appeal.

Exemption – Services to Panchayat / Municipality /State Government

Data Processing Forms P. Ltd. (AAR Order No. GUJ/GAAAR/APPEAL/2025/03 (IN APPLICATION NO. Advance Ruling/SGST&CGST/2022/AR/10) Dated: 22nd January, 2025)(GUJ)

The present appeal was filed against the Advance Ruling No. GUJ/GAAR/R/2022/43 dated 28th September, 2022.

The appellant is engaged in the manufacturing of computer forms, cut sheets, printed forms & is also engaged in trading of printers, cartridges, laptops, barcode stickers, OMR Sheet and educational booklets etc.

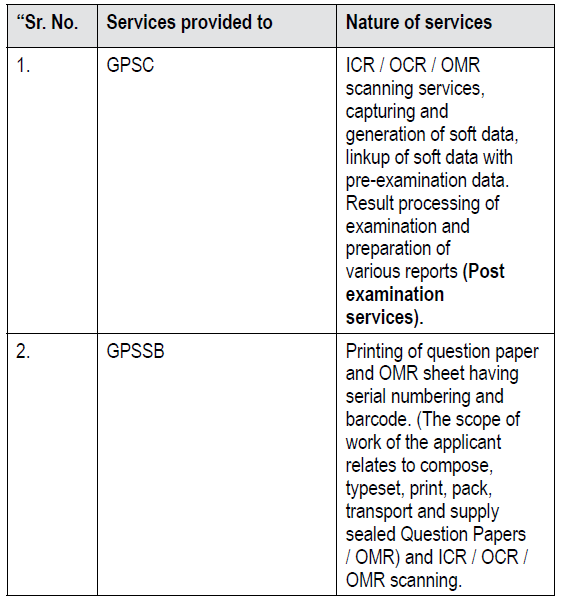

The appellant provides below-mentioned services to Gujarat Public Service Commission (GPSC) and Gujarat Panchayat Service Selection Board (GPSSB);

The appellant was of the view that the aforementioned services provided to GPSC and GPSSB are exempt in terms of entries 3 and 3 A of the Notification 12/2017-CT (R) and sought ruling from the ld. AAR. The ld. AAR passed ruling that the appellant is not eligible to the exemption under entry No. 3 and 3A of notification No. 12/2017-CT (R) dated 28th June, 2017 as amended, for supply of service to the Gujarat Panchayat Service Selection Board or to GPSC.

This appeal was against the above ruling of AAR. The main argument of the appellant was that GPSSB is an integral part of Panchayat system & therefore a local authority and it is covered under the provisions of article 243G and entitled for the benefit of entries 3 & 3A of the notification.

Similarly, in respect of GPSC the argument of appellant was that, it is a constitutional body having its own identity and 100% controlled, financed & managed by the State Government and therefore it is ‘State Government’ attracting above entries 3 and 3A.

The ld. AAAR noted that in terms of the entry 3 of notification No. 12/2017-CT (R), as amended, pure services [excluding works contract services or other composite services involving supply of any goods], provided to a Central Government, State Government, Union territory or local authority by way of any activity in relation to any function entrusted to a Panchayat under article 243G or to a Municipality under article 243W of the Constitution of India, are exempt. Similarly, in terms of entry 3A of notification, composite supply of goods and services, in which the value of supply of goods constitutes not more than 25 per cent of the value of the said composite supply provided to the Central Government, State Government or Union territory or local authority by way of any activity in relation to any function entrusted to Panchayat under article 243G or to Municipality under article 243W of the Constitution, are exempt.

The ld. AAAR also noted principle of interpretation that the exemption Notification is required to be interpreted strictly.

The ld. AAAR noted that appellant has relied on the definition of ‘local authority’ u/s 3(31) of the General Clauses Act. The ld. AAAR noted that since the supply to GPSSB is composite supply, it is required to be covered by entry 3A. The ld. AAAR observed that the GPSSB is neither a Central / State Government nor a Union territory. The ld. AAAR also held that it is not local authority as defined u/s.2(69) of the CGST Act. The ld. AAAR held that since the primary condition of the composite services having been provided to a Central Government, State Government, Union territory or local authority is not getting satisfied, the appellant is not eligible for the benefit of the notification and confirmed ruling of AAR about GPSSB.

In respect of GPSC, the ld. AAAR noted the contention of the appellant that GPSC is a constitutional body having its own identity and 100 per cent controlled, financed & managed by the State Government which amounts to ‘State Government’.

In this respect the ld. AAAR referred to definition of term ‘State Government’ under the General Clauses Act, 1897, which reads as under:

“(60) “State Government”, –

(a) as respects anything done before the commencement of the Constitution, shall mean, in a Part A State, the Provincial Government of the corresponding Province, in a Part B State, the authority or person authorised at the relevant date to exercise executive government in the corresponding Acceding State, and in a Part C State, the Central Government;

(b) as respects anything done [after the commencement of the Constitution and before the commencement of the Constitution (Seventh Amendment) Act, 1956], shall mean, in a Part A State, the Governor, in a Part B State, the Rajpramukh, and in a Part C State, the Central Government;

[(c) as respects anything done or to be done after the commencement of the Constitution (Seventh Amendment) Act, 1956, shall mean, in a State, the Governor, and in a Union territory, the Central Government;

and shall, in relation to functions entrusted under article 258A of the Constitution to the Government of India, include the Central Government acting within the scope of the authority given to it under that article];”

The ld. AAAR observed that in view of the above definition, GPSC is not State Government and confirmed ruling of AAR. The judgments cited by the appellant were distinguished. The ld. AAAR rejected the appeal confirming the ruling of ld. AAR.

Classification — “Nonwoven Coated Fabrics”

Om Vinyls Pvt. Ltd. (AAR Order No. GUJ/GAAAR/APPEAL/2024/21 (IN APPLICATION NO. Advance Ruling/SGST&CGST/2023/AR/22) Dated: 6th September, 2024)(Guj)

The applicant explained the nature of the product with manufacturing process as under:

“Nonwoven fabric is manufactured from PVC films, adhesive gum and nonwoven in their factory;

* that manufactured film is ready for further process called lamination / thermoforming;

* that cellular leather cloth/thermoforming is used widely for auto tops [canopy], sports shoe upper by laminating a thin PVC film with another layer of calendered sheeting containing blowing agent with textile backing; that this combination can be expanded in a separate stenter / foaming oven;

* a drum heated to about 180o C is driven & provided with a rubber coloured pressure roller to press the layers together & eliminate trapped air;

* the laminated combination is made to travel inside the heated chambers where the blowing agent is activated & controlled expansion is initiated in the middle calendered film;

* the process matches the standard approved by BIS; that the product is used mainly in outdoor application where the weather condition is uncertain.”

It is informed that components like, PVC resin, DOP / DIN, CPS 52 per cent, CA CO3, Stabilisers, Anti-oxidants, Pigment & Poly propylene are used in the process.

The uses of non-woven fabrics were also mentioned like use as table cover, TV cover, Sofa cover, fridge cover etc.

The appellant has raised following questions.

“1. Whether ‘nonwoven coated fabrics- coated, laminated or impregnated with PVC falls under HSN 56031400?

2. If ‘nonwoven coated fabrics- coated, laminated or impregnated with PVC’

does not fall under HSN 56031400 then it will fall under which heading of chapter 50?

3. If ‘nonwoven coated fabrics -coated, laminated or impregnated with PVC’

does not fall under HSN 56031400 then it will fall under which heading of chapter 39?”

In personal hearing the applicant explained composition of product as under:

“PVC film 55% Rs.12.60

Gum 29% Rs. 6.40

Nonwoven 16% Rs. 3.00

— ———-

Total 100% Rs. 20”

The ld. AAR referred to relevant material under Customs Tariff Act,1975, HSN, Circular etc. and reproduced same in AR.

Upon conjoint reading of the manufacturing process, the section notes, chapter notes, etc., the ld. AAR observed that the nonwoven coated fabrics — coated, laminated or impregnated with PVC, will not fall under chapter 56.

On going through the HSN explanatory notes of chapter 50, the ld. AAR observed that generally speaking chapter 50 covers silk, including mixed textile materials classified as silk, at its various stages of manufacture, from the raw materials to the woven fabrics and it also includes silk worm gut. The ld. AAR also observed that the applicant’s product nonwoven coated fabrics — coated, laminated or impregnated with PVC, is a combination of nonwoven fabrics, adhesive coat and PVC sheet, thereby not meeting the primary requirement for falling under chapter 50. In view of the foregoing, the ld. AAR held that the product of the applicant would not fall within the ambit of chapter 50 also.

After going through the information, the ld. AAR held that since the product of the applicant is a mixture of various constituents, the product is to be classified as if they consisted of the material or component which gives them their essential character. Observing that the major constituent is PVC sheet which is 120 GSM out of the total 240 GSM, the ld. AAR held that the goods of the applicant viz nonwoven coated fabrics — coated, laminated or impregnated with PVC would fall under chapter 39.

About bags, ld. AAR followed circular no. 80/54/2018-GST dated 31st December, 2018 and held that Non-Woven Bags laminated with BOPP would be classifiable as plastic bags under tariff item 3923 and would attract 18 per cent GST.

Accordingly, the ld. AAR passed ruling that the product, nonwoven coated fabrics -coated, laminated or impregnated with PVC will fall under chapter heading 39 and the products [a] table cover, [b] television cover [c] washing machine cover would fall within the ambit of tariff item 392690 and would attract 18 per cent GST, while bags would be classifiable under tariff item 3923 and would attract 18 per cent GST.

CLASSIFICATION – “SLACK ADJUSTERS”

Madras Engineering Industries Pvt. Ltd. (AR Order No. Advance Ruling No.27/ARA/2024 Dated: 5th December, 2024)(TN)

The facts are that M/s. Madras Engineering Industries Private Limited manufactures ‘Slack Adjusters’ and supplies the same to Truck, Bus and Trailer axle manufacturers in India. They supply these slack adjusters for the replacement market through their vast and well spread distribution arrangement.

The applicant further informed that Slack Adjusters under HSN code 87089900 are charged at 28 per cent as they are used for Trucks & Bus applications for both OE fitment and in the aftermarket. It was further informed that Slack Adjusters developed exclusively for trailer axle fitments are classified under HSN Code 87169010 and charged at 18 per cent for both OE fitment and for aftermarket requirements.

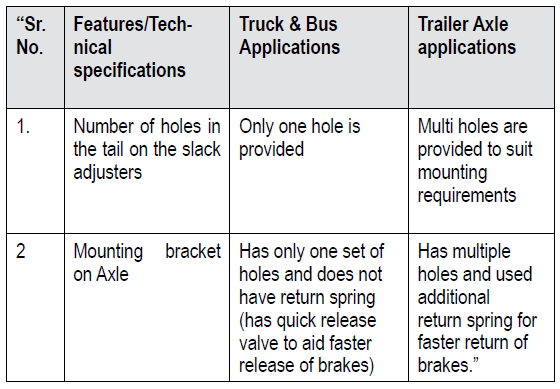

The difference between two products was explained as under:

Based on the above background, the applicant asked whether the HSN code followed and whether the GST rate applied for stack adjusters used in the truck and trailer applications is proper or not?

The ld. AAR referred to nature and use of product as under:

“7.1. The applicant is in the business of manufacturing and supplying ‘Slack Adjusters’ used in the braking system of Buses, Trucks and Trailers. Slack Adjuster is a part of a vehicle braking system and hence is an essential safety critical part of the vehicle. Slack adjusters are connected to the brake chamber push rod and Scam Shaft to convert lateral movement of brake chamber pushrod to rotational movement and rotate the S-cam shaft while brakes are applied. This is used to release and bring back the S-cam shaft to its original position when the brakes are applied. These slack adjusters are normally used in heavy vehicles namely, buses and trucks. It is also used in the trailers where the load carried is substantial. The specification of the slack adjusters used in ‘Buses & Trucks’ and in ‘Trailers’ are distinguishable as explained by the applicant.”

In order to arrive at an appropriate classification of the item used in the motor vehicle, the ld. AAR referred to the tariff classification as issued by the CBIC read with its schedules, guided by interpretative rules, section notes, Chapter Notes supported by the Explanatory Notes to the HSN.

In respect of Slack Adjuster for trailer, the ld. AAR referred to the entries for trailer. The ld. AAR observed that, a trailer is a wheeled vehicle attached to another powered vehicle for movement of goods and cargo. HSN 8716 exclusively deals with Trailers, Semi-trailers and other vehicles not mechanically propelled. As the HSN provides for a separate classification for trailers, semi-trailers and other such vehicles, the slack adjusters used exclusively in the braking system of trailers are rightly classified as ‘Parts and accessories of trailers’ under HSN 87169010. Accordingly, the ld. AAR approved classification made by applicant.

Regarding Slack adjusters used in the braking system of Buses and Trucks supplied to both, OEMs and aftermarket Sales, as ‘Parts and accessories of motor vehicles under HSN 87089900, the ld. AAR approved GST rate of 28 per cent.

Thus the ld. AAR upheld slack adjusters used in the braking system of a Trailer supplied to OEMs and aftermarket Sales as ‘Parts and accessories of trailers’ under HSN 87169010 and its GST rate of 18 per cent.

The ld. AAR mentioned that the applicant should ensure to adopt correct classification of the product as the slack adjusters supplied are different for both ‘buses & trucks’ and ‘trailer’ and accordingly allowed AR in favour of applicant.

SALE FROM FTWZ AND REVERSAL OF ITC

Haworth India Pvt. Ltd. (AR Order No. Advance Ruling No.26/ARA/2024 Dated: 5th December, 2024)(TN)

The applicant, M/s. Haworth India Private Ltd. had sought Advance Ruling on the following questions:

“1. In the facts and circumstances of the case, whether the transfer of title of goods by the Applicant to its customers or multiple transfers within the FTWZ would result in bonded warehouse transaction covered under Schedule III of the CGST Act, 2017 r/w CGST Amendment Act, 2018?

2. Whether the Integrated Tax (IGST) Circular No. 3/1/2018 dated 25th May, 2018 is applicable to the present factual situation?”

The questions were earlier decided vide AR dated 20th June, 2023 but the ld. AAAR remanded matter back vide appeal order dated 20th December, 2023 and hence this fresh proceeding. In fresh proceeding, following questions are considered:

“1. Whether in the facts and circumstances the activities and transactions would fall under paragraph 8(a) or 8(b) of Schedule III of CGST Act and remain non-taxable?

2. Whether irrespective of the activities and transactions falling under paragraph 8(a) or 8(b) as aforesaid input tax credit would be available without any reversals since no prescription has been notified for purpose of Explanation (ii) below Section 17(3) of CGST Act?”

The applicant is engaged in manufacture and sale of office furniture under the brand name ‘Haworth’. The applicant imports certain finished goods from its group entities. Applicant sales such imported goods.

The applicant contemplated to operate the import and re-sale transactions from a Free Trade Warehousing Zone (hereinafter referred to as ‘FTWZ’) for operational convenience involving less documentation and swift clearance process so as to expedite project execution. Applicant explained the process of such transaction.

The Applicant secures space in the FTWZ for a fee to store the imported goods from a unit holder. The Applicant executes required lease agreement with the FTWZ unit holder and deposits the goods from the port by filing Bill of Entry (BOE). FTWZ, owned and operated by independent third party, merely clears and warehouses the goods imported. The FTWZ collects warehousing charges from the Applicant.

No import duty is paid on clearance from the port.

The Applicant transfers the title of goods to customer under the cover of an invoice. The customer either clears goods from the FTWZ or may make further transfer of such goods to other customers. The goods continue to remain in FTWZ unit holder till the final customer files BOE and clears goods from FTWZ. The applicant reiterated that multiple transfers are made while goods are lying in FTWZ.

The final customer clears the goods from the FTWZ for home consumption and at this juncture, goods are removed from the warehouse and is taken to the premises of the Customer.

The applicant was of opinion that since FTWZ is equivalent to bonded warehouse, transfers within FTWZ before clearance shall fall under Schedule III of the CGST Act, 2017, thereby not attracting levy under GST.

The applicant was of further opinion that in case of goods deposited in a warehouse, only the person who is ultimately clearing the goods for home consumption is liable to tax and the transferor is not liable to tax on such transfer of warehoused goods.

The applicant also placed reliance on the advance rulings pronounced by Tamil Nadu Advance Ruling Authority in the case of The Bank of Nova Scotia – Order No. 23/AAR/2018 dated 31st December, 2018 -2019-VIL-29-AAR and

Sadesa Commercial Offshore De Macau Limited – Order No. 24/AAR/2018 dated 31st December, 2018 – 2019-VIL-28-AAR.

The ld. AAR examined scheme of ‘warehoused’ goods with reference to provision of GST Act.

After scrutiny of various aspects, in respect of question (1), the ld. AAR observed as under:

“7.23 Under these circumstances, we are of the opinion that a ‘Free Trade

Warehousing Zone’, as the name suggests, is a bonded premises providing warehousing facility, much in parity with the bonded warehouse under the Customs Act. Further, when the goods are imported and brought into a FTWZ unit, they are basically warehoused first and then traded or subjected to other authorized operations as the case may be. We notice that the applicant’s queries for advance ruling in the instant case is restricted to the first stage, i.e., when the imported goods are supplied to any person before they are cleared for home consumption, while they still remain warehoused. Accordingly, we are of the considered opinion that the provisions of 8(a) of Schedule III of the CGST Act, 2017, viz., “Supply of warehoused goods to any person before clearance for home consumption” applies to the instant case.”

Regarding question (2), the ld. AAR examined the provision of Section 17(2) and 17(3) which talks about apportionment of credit in such situations when a taxable person effects taxable supplies as well as exempted supplies. After examining the legal position, the ld. AAR observed as under:

“7.28 Under the facts and circumstances of the case, we are of the considered opinion that reversal of proportionate input tax credit of common inputs/input services/Capital goods is not warranted at the hands of the Applicant in terms of the amended Section 17(3) of the CGST Act, 2017 read with Explanation 3 of Rule 43 of the CGST Rules, 2017, even when the activity/transaction in question is covered under paragraph 8(a) of Schedule III of the CGST Act, 2017, as long as it does not relate to supplies from ‘Duty Free Shops’ at arrival terminal in international airports to the incoming passengers.”

Accordingly, the ld. AAR passed the ruling in favour of applicant.