This article is part of the ongoing series of articles dealing with Income-tax and FEMA issues related to NRIs. This is the second part of the two-part article on the interplay of Income-tax and FEMA issues for Emigrating Residents and Returning NRIs. Part-I of this article was published in the June 2024 edition of the BCAS Journal. It dealt with concepts and controversies related to migrating residents and change of citizenship. One can refer to Paragraphs 1 to 4 at the start of Part-I for introductory points in relation to movement from one country to another. Part-II — this part — is in continuation to Part-I and covers issues related to Returning NRIs. At the end of this article certain considerations which are common to both sets of people — migrating residents and returning NRIs — are also dealt with in Para C.

B. Returning NRIs

A recent survey highlights that at least 60 per cent of NRIs in the US, UK, Canada, Australia, and Singapore are considering returning to India after retirement1 . Apart from retirement, there are several other reasons due to which NRIs return to settle back in India — to stay with family members in India; due to their or their family members’ health reasons; citizenship issues in the foreign country; political instability in the foreign country; etc. In our experience, some of them are also returning for new and better business opportunities which are available in India now.

Under FEMA, there are different and overlapping classifications for non-residents like Non-resident Indian (NRI), Persons of Indian Origin (PIO), and Overseas Citizen of India (OCI) cardholders. This article covers all such people and collectively refers to all non-residents of India who come to India and become Indian residents as “Returning NRIs.” Such persons, if they are foreign citizens, should also refer to Para 11 to 16 in Part-I of this Article2 , which covers issues pertaining to change of citizenship.

1. https://retirement.outlookindia.com/plan/news/60-of-nris-consider-returning-to-india-after-retirement-sbnri-survey

2. Refer June 2024 issue of the BCAJ – 56 (2024) 251 BCAJ

The Income-tax and FEMA issues pertaining to Returning NRIs are explained in detail below:

B.1 Income-tax issues of Returning NRIs

17.13 Residential status

If a Returning NRI is determined to be Resident & Ordinarily Resident (ROR), their global incomes are taxable in India. Further, such a person needs to disclose all their foreign assets (including those which were acquired when the person was non-resident) and foreign incomes in their tax return. Any non-compliance exposes the person not only to interest and penalties under the Income-tax Act, but also the penal provisions under the Black Money Act4 for non-disclosure of foreign incomes and assets. Therefore, the first and foremost step under the Income-tax Act is to ascertain the residential status of the individual. Section 6, sub-sections (1), (1A) and (6), are relevant to determine the residential status of individuals.

3. The paragraph references continue from Part-I of this article

4. Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015

17.2 In the case of Returning NRIs, the individual is coming back for good. He is not coming on a visit to India. Hence, the relief pertaining to “being outside India and coming on a visit to India” provided under Explanation 2 to Section 6(1)(c) of the Income-tax Act (ITA) is not available. Consequently, the relief of staying up to 181 days in India is not available to them. In other words, the basic “60 + 365 days test”5 applies to Returning NRIs, and if it is met, the individual becomes a resident u/s. 6(1) of the ITA. A couple of nuances pertaining to this were dealt with in detail in the December edition of the BCAS Journal. For completeness’s sake, they are briefly touched upon below:

a. Benefit of visit not allowed:

A person returned to India after resigning from her employment in China. The Authority for Advance Rulings (AAR) held6 that relief under Expl. 2 to S. 6(1)(c) of the ITA will not be available to her since the facts and circumstances show that the reason for coming to India is not just a visit. Hence, the “60 + 365 days test” test will apply.

b. Is hair-splitting between visit and permanent stay allowed during the same year?

Karnataka High Court has held7 that when the individual – being outside India, was on a visit to India – such stay should be tested against the 182-day test and not considered for the “60 + 365 days test.” Later, during the year, if the person returns to India, only the stay after such return needs to be considered for the “60 + 365 days test.” However, in the decision by AAR referred to herein above in sub-para (a), the hair-splitting between a visit and a permanent stay in India was not allowed. Hence, hair-splitting of a person’s stay between ‘visit’ and ‘permanent stay’ during the same year is litigious.

5. “60 + 365 days test” means that the individual has stayed in India for 60 days or more during the relevant previous year and for 365 days or

more during the four preceding years

6. Mrs. Smita Anand, China [2014] 42 taxmann.com 366 (AAR - New Delhi)

7. Director of Income-Tax, International Tax, Bangalore vs. Manoj Kumar Reddy Nare [2011] 12 taxmann.com 326 (Karnataka)

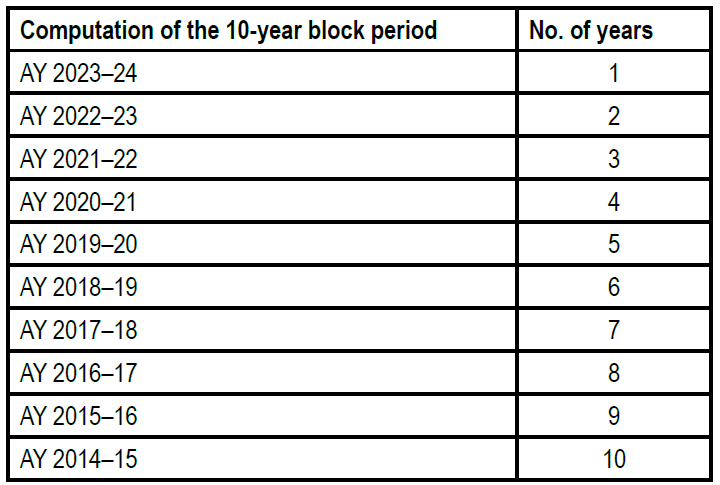

17.3 If the person was a non-resident of India in 9 out of the preceding 10 previous years; or if his or her stay in India in the preceding 7 years was less than 729 days, such an individual would be Resident but Not Ordinarily Resident (“RNOR”). These provisions of Section 6(6)(a) of the ITA have been explained in detail in the December 2023 edition of the BCAJ. In general, before the amendments by the Finance Act 2020, a returning Indian could claim RNOR status for 2 or even 3 years if one of the above tests of Section 6(6)(a) is met. The amendments by the Finance Act 2020 have diluted the RNOR status for Returning NRIs. This is explained in detail below.

17.4 If an individual does not become a resident, u/s. 6(1), one should also consider the provisions of Section 6(1A) wherein an Indian Citizen is considered a resident under specific circumstances8, where he is not liable to tax in any other country by reason of residence, domicile, or any other criteria of similar nature. If an individual becomes a resident by virtue of Section 6(1A), he is always considered as RNOR as per Section 6(6)(d).

8. Where his or her income from sources within India exceeds ₹15 lakhs in that year(s).

Individuals who are covered u/s. 6(1A) become deemed RNORs. Even if they do not visit India for a single day, they are residents but not ordinarily residents under the ITA. This has an impact when they return to India for good. Let us say, an Indian citizen, Mr Kumar has been employed and staying in Oman since 2010. Mr Kumar came on visits to India totalling a period of 65 days every year with clarity that he would remain a non-resident of India due to relief available of a visit to India as per clause (b) to Explanation 1 to Section 6(1)(c). On 1st April, 2024, he retired and came back to India for good. In the absence of Section 6(1A), he would have been a non-resident since 2010. Hence, after returning to India, he would have been RNOR for at least the first two years.

However, Oman does not tax individuals. Post Finance Act 2020, as per Section 6(1A), such an Indian citizen would be RNOR and not NR for the PYs 2020-21, 2022-23, 2023-24. This means he does not meet the first test u/s. 6(6)(a) of being NR for at least 9 years out of the last 10 years. The relief u/s. 6(6)(a) has thus been diluted due to Section 6(1A). In simple words, he will be ROR from PY 2024-25 and will be liable to Indian tax on his global income. Similar would be the situation for an Indian citizen or person of Indian origin9 who visits India for 120 days or more during each year, and his stay in the preceding 4 years is 365 days or more. Such a person gets covered by the amended portion of clause (b) of Explanation 1 to Section 6(1)(c) and consequently would be RNOR as per Section 6(6)(c)10.

9. A person shall be deemed to be of Indian origin if he, or either of his parents or any of his grand-parents, was born in undivided India – Explanation to clause (e) of Section 115C of ITA.

10. Where his or her income from sources within India exceeds ₹15 lakhs in that year(s).

17.5 Normally, a Returning NRI would be considered as RNOR if he had not spent more than 728 days during the preceding 7 years. This should be the case generally for 2 or even 3 years after a person returns to India. But for persons like Mr Kumar, who visits India every year and then settles in India, they may not meet the test of stay in India of less than 729 days during the preceding 7 years after the first year of returning to India. Hence, those individuals who stay abroad and are planning to settle in India need to be aware of the dilution of their RNOR status due to the provisions of Section 6 as amended vide Finance Act 2020.

18 Disclosure and source of foreign assets

Since AY 2012-13, Indian residents (ROR) are required to disclose their assets located outside India in their Income-tax return form. This is required even if such a resident is otherwise not required to file a tax return. Returning NRIs would, in most cases, have savings, assets, and investments abroad when they come back. On becoming ROR, all such foreign assets need to be disclosed in the tax return. The person would have acquired these assets when he was staying abroad and was a non-resident. The source of funds for acquiring these assets is not required to be explained or disclosed in the tax return. However, practically, things are quite different.

There is 360-degree profiling by the regulators these days. The CBDT has formed Foreign Asset Investigation Units (FAIUs) in all the 14 investigation directorates across India. Their job is to analyse the plethora of information received by India from foreign jurisdictions under Automatic Exchange of Information (AEoI) agreements, CRS, DTAAs, etc. If they come across any red flags, they issue a notice asking for detailed information pertaining to each and every foreign asset held by the person since its acquisition. The red flags could be a variance between the data received by them vis-à-vis the foreign assets disclosed in the tax return by the assessee; or foreign assets disproportionate to the transactions or profile of the assessee, etc. They even ask for decades-old data and documents supporting such data. Hence, maintaining documents becomes particularly important.

In such cases, until and unless it is proven through documentary evidence that a foreign asset was acquired from bonafide sources, the matter is not closed. This becomes a big hassle. There are cases where the assessees did not retain their old bank statements and other documents. In fact, foreign banks and brokers do not provide old statements easily and they also charge heftily for obtaining old statements. Further, foreign banks and financial institutions do not retain records beyond a certain number of years, in which case, it becomes almost impossible to provide the documents to the officer. Hence, Indians who are staying abroad, whether they plan to return to India someday or not, should keep proper and complete data of all their assets. If and when they return to India, such a record would become important. Further, they need to maintain documents to justify their increase in net worth by their sources of incomes during the years when they were non-resident. If there is any violation in the disclosure of foreign assets; or if the officer is not satisfied with the explanation or documents, proceedings can be initiated under Section 10 of the Black Money Act11 (BMA) and the harsh penal provisions of the BMA are also invoked in certain cases. This has happened in even bona fide cases where innocent errors are made in disclosing foreign assets.

11. Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015

19 Other Disclosures in ITR Form

Apart from foreign assets and incomes, other disclosures are also required to be made in the Income-tax return form, which are tabulated below:

| Particulars |

ROR |

NOR |

NR |

| Unlisted equity shares |

To be disclosed of all companies. |

To be disclosed only of Indian companies. |

| Directorships |

To be disclosed in all companies across the globe. |

To be disclosed in all Indian companies & only in such foreign companies which have income accruing or deemed to be accruing in India. |

| Schedule AL |

Global assets. |

Only Indian assets. |

| Schedule FSI |

Foreign-sourced incomes are included in the Total Income (largely relevant only for RORs.) |

| Schedule EI |

Incomes exempt under the Income-tax Act or DTAA. |

20 Treaty relief

Similar to migrating Indians, even for Returning NRIs, there can be an overlapping period wherein the person is a resident of India as well as of the country he is returning from. This leads to dual residency, for which tie-breaker tests are prescribed under Article 4(2) of the Double Tax Avoidance Agreement (DTAA). There could also be a possibility of the concept of split residency being applicable. Accordingly, the provisions of the DTAA can be applied. These provisions have been explained in detail in the second article of this series (January 2024 edition of the BCAJ). In essence, there could be benefits vide the DTAA in the foreign jurisdiction as well as in India. The credit of tax paid in a foreign jurisdiction as per the DTAA can be availed against the tax payable in India. Necessary forms will be required to be filed along with supporting documents to claim credit.

21 Continuing foreign employment or business

Many people continue their employment or business abroad after returning to India. This has become easier in today’s globalised technology-driven era. In fact, the Covid lockdown saw many Indians stuck in India

or coming back to India and continuing their foreign business or employment from India. However, it is pertinent to note that the economic activity is being done from India. It should be checked whether any income directly accrues in India on account of such activity due to specific provisions which can get triggered in such a case, of which the most common ones are explained below:

21.1 Salary: Section 9(1)(ii) deems the salary proportionate to the period when the employment was exercised from India to be accruing in India. Hence, even if a person is NR or NOR, the amount of salary proportionate to the days he exercises employment from India is deemed to accrue in India. This provision applies not only to Returning NRIs, but to everyone. Prima facie, the proportionate salary is taxable under ITA, and one should go under the applicable DTAA to claim relief, if any.

21.2 Place of Effective Management: A foreign company is considered as resident of India if its Place of Effective Management is, in substance, in India, during that year12. The CBDT has prescribed detailed guidelines through Circulars 6, 8 and 25 of 2017. It should be noted that this provision applies only to companies having a turnover of more than INR 50 crores during the financial year.

21.3 Business Connection and Permanent Establishment: When an individual works in India for a foreign entity, he may constitute a “Business Connection” of the foreign entity in India. In that case, the income pertaining to the activities carried out through such Business Connection is deemed to accrue in India13 . Further, if there is a DTAA between India and the country where the entity is resident, generally, the business profits of the foreign entity would be taxable in India only if the foreign entity has a Permanent Establishment (PE) in India. Every DTAA has different criteria for determining whether there is a PE. Hence, it needs to be checked whether the individual constitutes a Business Connection of such entity in India, and if yes, whether he constitutes a PE of such entity in India as per the applicable DTAA. This can be possible in cases where the foreign company is run almost exclusively by the Returning NRI.

12. Section 6(2) of ITA

13. Section 9(1)(i) of ITA

B.2 FEMA issues regarding Returning NRIs

22 Residential status

The provisions pertaining to residential status under FEMA were dealt with in detail in the March 2024 edition of BCAJ. In essence, as per Section 2(1)(v) of FEMA, when a person comes to India for or on taking up employment in India; or for carrying on business or vocation in India; or under circumstances which indicate his intention to stay in India for an uncertain period — he becomes an Indian resident under FEMA. Hence, when a person comes to settle down in India for good, he or she becomes a resident under FEMA from the date of their return to India. This is because the person is coming to India in such circumstances, which indicates his intention to stay in India for an uncertain period. Hence, from the day a person returns to settle in India or for the purposes mentioned above, all provisions under FEMA meant for residents become applicable to such person.

23 Scope of FEMA as applicable to Returning NRIs

Apart from the assets and transactions covered u/s. 6(4) of FEMA and the balances in RFC accounts (explained in detail below), all other transactions outside India (whether in foreign currency or INR); all Indian transactions in foreign currency and all transactions with non-residents (whether in or outside India) come under the purview of FEMA. This can impact Indian transactions of the Returning NRI with other non-resident family members. As non-residents, they would have had the liberty to transfer funds between their NRO accounts. However, there will be several restrictions on transactions between a Returning NRI (who is now a resident individual) and a non-resident. Thus, gifts, loans and even payments made to or on behalf of non-residents can have implications under FEMA. Thus, a change of residence requires a change in mindset, as otherwise, Returning NRIs may end up committing violations under FEMA.

24 Holding foreign assets abroad

24.1 Background of FERA: Under FERA, as it was enacted, when a person became an Indian resident, he was required to liquidate all his foreign assets and bring the foreign exchange into India unless approval was obtained from RBI. This was liberalised in July 1992 when the Government of India issued six notifications granting exemptions from several different provisions of FERA to the returning Indians. These notifications were covered with a press note and a circular issued by RBI in Sept. 1992 — ADMA Circular No. 51 dated 22nd September, 1992. It explained the notifications. A summary of all the provisions is that on return to India, the Returning NRI retain all his assets abroad — provided that the assets were not acquired in violation of FERA and that the person was a non-resident for at least one year before becoming resident. There was no need to make any declaration under FERA. He could change his assets in the sense that he could sell one asset and buy another. He could retain dividends / interest / rent and other incomes earned on the assets. He could reinvest these incomes or spend the same. He was at liberty to bring the assets to India or to retain them abroad. He could gift these assets to anyone. On death, his foreign assets would pass to his heirs without any restrictions. If the Returning NRI held shares in any company, the shares would be considered as his investments. The company could continue business abroad. One could say that FERA did not apply to such wealth of the person and the incomes generated on such wealth. The person was free to do anything with the same.

24.2 Provisions under FEMA: Under FEMA, unfortunately, such liberalisation has been provided in a very brief manner through Section 6(4), which is reproduced below:

“(4) A person resident in India may hold, own, transfer or invest in foreign currency, foreign security or any immovable property situated outside India if such currency, security or property was acquired, held or owned by such person when he was resident outside India or inherited from a person who was resident outside India.”

It is provided that any foreign currency, foreign security, and immovable property situated outside India which were acquired when the person was a non-resident, can be continued to be held or owned after becoming a resident.

24.3 Section 6(4) of FEMA does not clearly specify the transactions which are allowed as was quite apparent as per the circulars issued under FERA. On making a representation, RBI issued A.P. Dir Circular No. 90 dated 9th January, 2014, which prescribes the transactions covered u/s. 6(4). Those are as follows:

a. Foreign currency accounts opened and maintained by the Returning NRI when he or she was resident outside India.

b. Income earned through employment or business or vocation outside India taken up or commenced while such person was resident outside India, or from investments made while such person was resident outside India, or from gift or inheritance received while such a person was resident outside India.

c. Foreign exchange, including any income arising therefrom, and conversion or replacement or accrual to the same, held outside India by a person resident in India acquired by way of inheritance from a person resident outside India.

d. Returning NRIs may freely utilise all their eligible assets abroad as well as income on such assets or sale proceeds thereof received after their return to India for making any payments or to make any fresh investments abroad without approval of the Reserve Bank, provided the cost of such investments and / or any subsequent payments received therefor are met exclusively out of funds forming part of eligible assets held by them and the transaction is

not in contravention to extant FEMA provisions.

Thus, such assets can be sold, and proceeds may even be reinvested abroad. There is no requirement to repatriate the income earned on these assets or sale proceeds thereof into India.

24.4 One can consider that broadly, the restrictions under FEMA do not apply to assets covered u/s. 6(4) of FEMA. One of the important clarifications in this regard pertains to overseas investments by resident individuals, which are allowed under the Overseas Investment Rules14 (OI Rules) of FEMA only if specific conditions are met. However, when it comes to foreign assets covered u/s. 6(4), Rule 4(b)(iii) of the OI Rules clearly provides that the OI Rules do not apply to any overseas investment covered u/s. 6(4). It would thus also cover any asset or investment which a resident may otherwise either not be permitted to invest in; or permitted only within a certain limit; or only after fulfilling attendant conditions — under the OI Rules. For instance, resident individuals are not allowed to make Overseas Direct Investment in a foreign entity which is engaged in financial services activity. However, if a non-resident had invested in such a company abroad and later on, he or she becomes an Indian resident, such person can continue holding shares of the foreign company. The income thereon and the sale proceeds thereof can be retained abroad. If the individual wants to make any further investment in the foreign entity engaged in financial services activities out of funds lying in his Resident bank account in India, he or she will not be generally permitted to do so15.

14. Foreign Exchange Management (Overseas Investment) Rules, 2022 – Notification No. G.S.R. 646(E) issued on 22nd August 2022.

15. Refer Rule 13 of the OI Rules read with paragraph 1 of Schedule III to OI Rules.

24.5 Other assets not specified u/s. 6(4) of FEMA: Section 6(4) specifies only three assets. Further, the circular also does not provide complete clarity. A person may own several other assets. For instance — the person can have an interest in a partnership firm or LLC or can own gold, jewellery, paintings, etc. As a practice, the RBI has taken a view since 1992 that a person is eligible to continue owning / holding all the foreign assets after turning resident, which he had acquired as a non-resident. This also includes such assets or investments which he could not have otherwise owned or made as a resident.

24.6 Insurance abroad: Returning NRIs may have different types of insurance policies issued by insurers in India as well as outside India. As explained above, funds covered under Section 6(4) of FEMA and lying abroad can be utilised for any purpose, including premium payment for insurance policies. FEMA provisions pertaining to s the utilisation of Indian funds for foreign insurance policies16 by Returning NRIs are as follows:

a. Health insurance policy can be continued to be held by a Returning NRI provided the aggregate remittance including the amount of premium does not exceed the LRS limit.

b. Life insurance policy can be continued to be held by a Returning NRI if it was issued when he was a non-resident. Further, if the premium due on such policy is paid by remittance from India, the maturity proceeds or amount of any claim due on the policy should be repatriated to India within 7 days of receipt.

24.7 Loans abroad: If a person has taken a loan abroad as a non-resident and becomes a resident later, he can service such loans subject to such terms, conditions and limits as specified by RBI. In general, RBI has not objected to a Returning NRI using his or her foreign funds covered under Section 6(4) of FEMA to service such loan repayments.

24.8 Foreign currency: Returning NRIs may need to bring in foreign currency notes and coins into India. Notification No. FEMA 6(R)17 provides that such person can bring into India without limit foreign exchange (other than unissued notes) from any place outside India. However, a declaration needs to be made to the Customs authorities.

16. Para 2 of Master Direction on Insurance - FED Master Direction No. 9/ 2015-16 - last updated on 7th December 2021.

17. Reg. 6(b) of Foreign Exchange Management (Export and import of currency) Regulations, 2015.

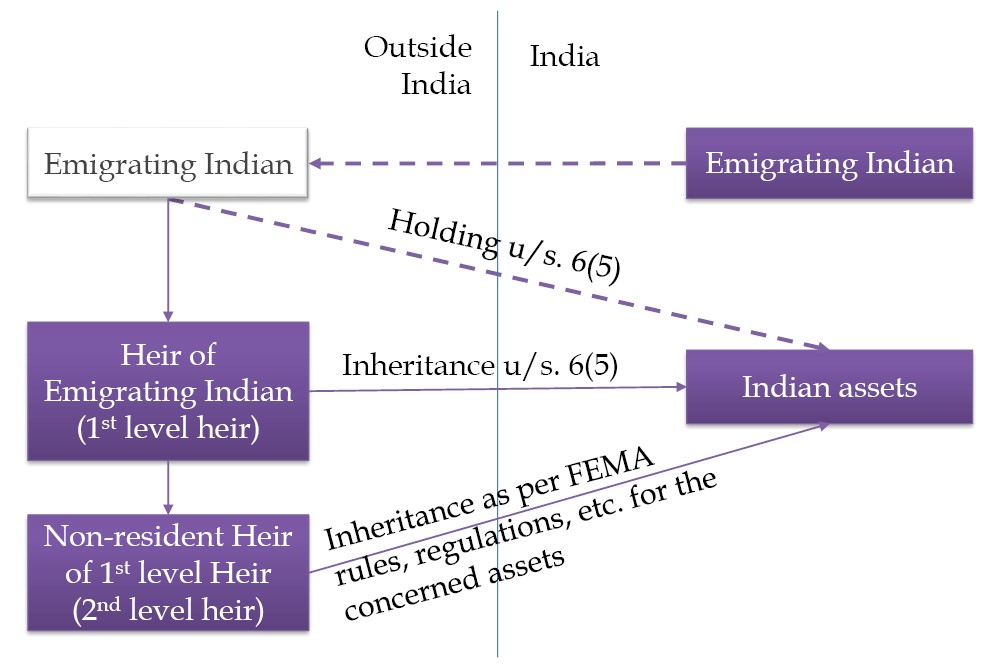

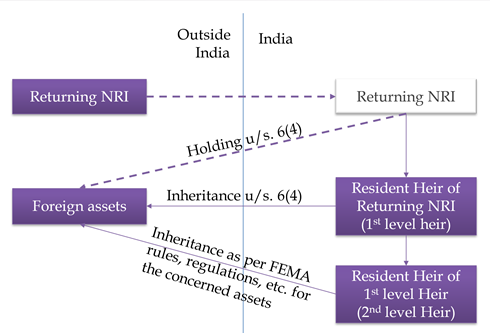

24.9 Inheritance of assets covered under Section 6(4) of FEMA: The first limb of Section 6(4) allows residents to hold assets abroad which they had acquired as a non-resident. The second limb further allows a resident heir of such Returning NRI to inherit these foreign assets from him or her. This is in line with the reliefs provided through the circulars issued earlier under FERA. However, it should be noted that this provision covers only one level of inheritance, i.e., from the Returning NRI to his or her heir. Later, if a resident heir of such heir wants to inherit these foreign assets, it is not covered by Section 6(4). The relevant notifications, rules, etc. under FEMA corresponding to the concerned assets need to be checked for the same. A summary of the holding and inheritance of foreign assets under Section 6(4) of FEMA can be summarised as follows:

Exceptions to this rule are for overseas immovable properties18 and foreign securities19, inheritance for which is allowed up to any generation if the investment and holding of such foreign property were as per extant FEMA regulations.

18. Rule 21(2)(i) of OI Rules.

19. Para 9(b) of Schedule III to FEMA Notification 5(R)/2016-RB – FEM (Deposit) Regulations,2016.

It should be noted that there are several controversies surrounding Section 6(4) of FEMA, including the interpretation of its second limb. We have not discussed all the controversies here, considering this is an article on a broader topic.

25 Impact on Indian assets

25.1 Bank and demat accounts: Returning NRIs need to designate their NRO bank and demat accounts as normal Resident accounts once they become residents20.

There are some special types of accounts in which non-residents can hold funds like NRE, FCNR, etc. On becoming a resident, NRE accounts need to be closed; however, FCNR deposits are permitted to be continued till maturity. Funds in both these accounts can be either transferred to the Resident account (becomes non-repatriable) or to the RFC account (repatriability continues, and such funds remain out of FEMA purview). Returning NRIs are permitted to hold foreign exchange in India in RFC accounts. The funds lying in an RFC account can be remitted abroad without any restrictions and can be used or invested for any purpose. The provisions of FEMA do not apply to the same. The provisions for such accounts will be discussed in detail in the upcoming articles in this series of articles.

20. Para 9(b) of Schedule III to FEMA Notification 5(R)/2016-RB – FEM (Deposit) Regulations, 2016.

25.2 Loan from NRI / OCI to a resident: If an NRI / OCI has given a loan to a resident (as per the FEMA guidelines) and he becomes a resident later, the repayment may be made to the designated account of the lender maintained with a bank in India as per the RBI guidelines, at the option of the lender.

25.3 Privately held investments in India: There could be investments in Indian companies, LLP, partnership firms, etc., made by Returning NRIs when they were non-residents. The implications of such investments due to a change of residence are explained below:

25.3.1 Indian assets held on a non-repatriable basis: NRIs and OCIs are permitted to invest in India on a non-repatriable basis, which has minimal restrictions and no reporting requirements. In such cases, if the person becomes a resident of India, there is no change in the character of the holding. The investment was anyway treated at par with domestic investment and no reporting, etc., is required. Normally, there is no formal record to be kept by the investee entity regarding the residential status of the person if the investment is on a non-repatriation basis. However, if there is any such record maintained, the residential status should be updated therein.

25.3.2 Indian assets held on a repatriable basis: Let us say the person has made investments in India on a repatriable basis. As a non-resident, he can remit full sale proceeds abroad without any limit. Now, if such a person returns to India and becomes a resident, the resultant structure is that an Indian resident is holding an Indian asset. The repatriable character of the investment is lost! This is a particularly important provision. All investments held by a non-resident on a repatriable basis become non-repatriable from the day he becomes a resident. In fact, there is nothing like repatriable or non-repatriable investment for a resident. Every Indian asset of a resident is considered as a domestic investment. It is only assets covered under Section 6(4) and the funds transferred to the RFC account, which are free from FEMA. This becomes a critical point, which every Returning Indian should consider in advance. When a non-resident holding an investment in an Indian entity on a repatriable basis becomes a resident, he should intimate it to the entity, and the entity should record the shareholding of the person as domestic investment and not foreign investment.

25.3.3 Indian assets held through a foreign entity: Let us say, a non-resident invests in Indian assets on a repatriable basis. However, instead of investing in his personal name (as explained in the above para), the investment is made by his foreign entity. Thereafter, the person becomes an Indian resident. The resultant structure is that an Indian resident owns a foreign entity which has invested in India on a repatriable basis. This enables the following:

a. Holding in Foreign entity: The ownership in the foreign entity by the Returning NRI is covered under Section 6(4). He can thus continue to hold such investments.

b. Repatriability of Indian assets: The Indian assets continue to be held on a repatriable basis by the foreign entity. All incomes and sale proceeds therefrom can be remitted abroad by the foreign entity without any limit. Had the individual directly held Indian assets and became resident, the repatriable character would have been lost — as highlighted above in Para 25.3.2. However, one should consider the tax implications of such a structure, especially with regard to POEM, Transfer Pricing and Permanent Establishment provisions under the ITA, as explained in para 21 above.

26 Remittance facilities for resident individuals

Liberalised Remittance Scheme: LRS is the remittance facility available for resident individuals. The LRS limit of USD 250,000 per financial year is the ceiling for all current and capital account transactions covered under the Current Account Transaction Rules. Barring exceptions like exports and imports and certain relaxations21 which are available in limited situations, the remittance facilities for a person resident in India under FEMA are constrained to the LRS limit. Returning NRIs should hence note that their remittances from India will be restricted to a considerable extent compared to what they were allowed as non-residents22. Even the liberty of remitting current incomes without any limit is not available for resident individuals.

21 Like use of International Credit Card while being on a visit outside India; higher amount of remittance allowed for educational or medical expenses; or for acquisition of ESOPs, sweat equity, etc.

22 Please refer to Para 7.6 in Part-I of this article for USD 1 Million Scheme which is available to NRIs.

27 Fresh incomes earned abroad

Let us say the individual earns fresh income abroad after becoming a resident – like salary, royalty or even receiving a gift of funds from a non-resident. A resident individual cannot retain such foreign exchange abroad. He is required to take all reasonable steps to realise the foreign exchange due or accrued to him and repatriate the same within 180 days of the date of receipt23.

23. Section 8 of FEMA r.w. Regulation 7 of FEMA Notification 9(R)/2015-RB.

C. OTHER RELEVANT ISSUES COMMON TO CHANGE OF RESIDENTIAL STATUS

28 Change of Citizenship

Change of citizenship has several ramifications beyond change of residence, especially under FEMA. The issues to be kept in mind when a person has obtained foreign citizenship are elaborated in Para 11 to 16 in Part-I of this Article covered in the June 2024 issue of the BCAJ. Returning foreign citizens should consider the implications of the country of their citizenship on their move to India — especially where such countries are taxing them based on their citizenship, exit taxes and estate duty or inheritance tax — all of which are explained briefly below.

29 Change of residence for a short period

One can see that the scope of FEMA and the Income-tax Act changes drastically with the change of residential status. This article attempts to cover aspects where there is a change of residence for good. If the residential status of a person changes for a short period of time, caution should be exercised before taking the benefits of a change of residence. Consider a situation where a resident goes abroad; claims to be a non-resident under FEMA or the Income-tax Act; takes benefit of such change (for example, by remitting USD 1 million from India or taking a treaty benefit as a non-resident of India); and again, becomes an Indian resident — all within a short period of time. In such cases, the regulator or tax officer may question the whole arrangement and consider that the change in residence is not genuine. Action can be taken based on anti-tax avoidance provisions under the Act and relevant treaty (please refer to para 35 below). Hence, there should be clarity on residential status; bonafides of transactions and genuineness of arrangements. In fact, sometimes it is ideal and safe if benefits are availed of only after the person is certain about his or her change in residential status and it is maintained over a period of time.

30 Succession Planning

There are several laws which need to be considered for succession planning like the applicable succession laws, Sharia law in the case of Muslims, Trust laws in case of Trusts, FEMA for cross-border transactions & assets, corporate laws in case of securities, stamp duty laws, Income-tax laws, Inheritance / Estate Tax etc. Hence, succession planning from a holistic approach is especially important wherever the family members or the assets are spread over more than one country. In fact, FEMA itself contains several complexities regarding inheritance. There are only a few provisions specifically dealing with inheritance and gifts under FEMA. These provisions are spread over many notifications. For several assets and situations, provisions are completely missing. To top it all off, everything changes when a person shifts residence from one country to another. The whole succession planning exercise needs to be re-considered in such cases — especially due to FEMA provisions.

31 Inheritance Tax or Estate Duty

31.1 Migrating persons, as well as Returning NRIs, should consider the inheritance tax or Estate Duty laws of the foreign jurisdiction. Different countries levy such taxes based on different criteria like citizenship, visa (green card in USA), domicile (UK), etc. In the USA, there is the Federal Estate Tax as well as the State Estate Tax. Residents of countries where such taxes or duties are applicable should have proper Estate Duty planning done. There have been cases where Estate Duty or Inheritance Tax is payable in the foreign country where a large amount of wealth was in the immovable properties which cannot be sold since the person is staying in the same. Further, if substantial wealth is situated in India, the limits on remittances abroad can also create a hindrance for paying such taxes. The following basic questions can be considered:

a. Applicability of such tax and the taxable events.

b. Connecting factors including domicile, citizenship, residence, etc.

c. Assets covered.

d. Thresholds applicable, if any, and tax rates.

e. Implications of gifts between family members.

f. Whether it applies to the inheritance of Indian assets received by the person on the death of his parents who are staying in India.

g. Treaties in relation to Double Taxation Relief for Estate Duties.

31.2 One common question asked is whether the Indian Government will bring in Estate Duties or Inheritance taxes. There is an unsupported fear in people’s minds of such duties impacting their wealth leading them to create Trust structures for protecting their wealth from such duties. The Government has earlier been on record to state that no such Estate Duties are planned. Further, even if such duties are introduced, they would have enough anti-avoidance provisions to counteract against any planning undertaken by taxpayers.

32 Exit Tax: Some countries have a concept of Exit Tax to prevent loss of revenue, if any, upon change of residential status / citizenship. It is levied when a person revokes citizenship or visa (like revocation of citizenship or green card in the USA) or if a person shifts his residence to another country (like Departure Tax in Canada). One may carefully plan the timing of their change of residence to minimise the impact of such taxes wherever possible.

33 Transfer Pricing

In simple words, Transfer Pricing triggers in case of a transaction which can give rise to income (or imputed income) between associated enterprises, of which at least one party is a non-resident. On change of residence, the migrating resident’s or Returning NRI’s continuing transactions with associated enterprises may come under the purview of Transfer Pricing provisions. All such transactions must be on an arm’s length basis. The implications under Transfer Pricing on the shift of a person from or to India should hence be considered.

34 Section 93 of ITA

Section 93 is a complex anti-avoidance provision which targets certain transfers of assets in a manner which leads to the income being earned by a non-resident, but the transferor still has the power to enjoy such incomes. The provision targets such transfers whereby incomes would have been chargeable to tax in the hands of the transferor if the transferor had earned such incomes directly. For example, a Returning NRI who transfers assets to another person before returning to India, but with a condition that income earned by such other person would be in control of the NRI, would be caught by this provision. There are several conditions and nuances in the provision, and one must note that any tax planning done before a change of residence can be impacted due to this provision.

35 Anti-tax avoidance provisions

While there are several Specific Anti Avoidance Rules (SAARs) prescribed under the Income-tax Act – POEM, Business Connection, Transfer Pricing, etc. – one should also consider General Anti Avoidance Rules (GAAR), which have been notified under Sections 95 to 102. GAAR would apply to an arrangement if it is regarded as an Impermissible Avoidance Arrangement (IAA). There are detailed provisions on the same. The ramifications of GAAR are massive. Once an arrangement is determined as IAA, the officer can treat the place of residence of such person at a place other than their claimed place of residence; ignore one or more transactions; deny benefits of a DTAA; recompute the income and tax of the assessee; and so on. While the Department has invoked GAAR in very few cases till now, it looks evident that GAAR will be invoked more frequently in the times to come. Recently courts have decided on the matter of applicability of GAAR in certain situations. Further, after the advent of the Multi-Lateral Instrument, several treaties that India has entered with other countries and jurisdictions have brought in anti-tax avoidance provisions where the change of residence is only for the purposes of claiming treaty benefit. These include the broader Principal Purpose Test and amendment in the preamble to the treaty, as well as the specific anti-tax avoidance measures that are today part of many double-tax avoidance treaties that India has signed.

36 Documentation and record-keeping

Change of residence typically leads to several queries from the tax department or regulator — especially for Returning NRIs in relation to their foreign assets. They would like to know that the foreign assets of such a person were acquired in a bona fide manner as a non-resident. One can refer to para 18 above explaining the same. Therefore, full documentation should be maintained. A few key areas where documentation should be maintained are:

a. Calculation of number of days of stay in India in each year and determination of residential status.

b. Passport copies to substantiate travel details and number of days stayed in India.

c. Relevant documents for every foreign asset and transaction, especially the opening statements, along with an explanation of the source of funds (irrespective of residential status).

d. Tax returns and other documents filed in the foreign jurisdiction.

e. Disclosure of foreign assets including in case of joint ownership, nomination, authorised signatory, etc.

f. Employment contract, salary slips, visa, etc.

g. Details and documents substantiating the purpose of immigration or emigration.

37 Impact of other laws

37.1 Transferring physical or movable assets from or into India: While FEMA permits holding assets in or outside India migrating or returning individuals may plan to move valuable assets with them from or into India – like gold, jewellery, art, etc. One should consider the permissibility and limits under Baggage Rules, 2016 of the Customs Act, along with the disclosures required thereunder. Further, certain movable items like art and antiques, as well as those dealing with wildlife, etc., need to be imported or exported only as permitted under the relevant laws24. Similarly, a migrating resident needs to check the parallel provisions of the country to which they are migrating.

24. The Antiquities and Art Treasures Act, 1972 and The Wild Life (Protection) Act, 1972, etc.

37.2 Indirect taxes: Indirect taxes have a significant impact, especially in a situation where the individual works in a personal capacity instead of employment. For instance, if Returning NRI continues working for a foreign entity as a consultant or in a similar manner, the applicability of GST and other indirect taxes needs to be checked.

37.3 Stamp duty laws: Certain individuals end up entering into gift deeds, powers of attorney, etc., on change of residence. Any document executed or brought within India can attract stamp duty. The stamp duty laws need to be checked before executing any such document. Similarly, the stamp duty law of the foreign country should also be considered.

37.4 Other laws: There are several other laws which could apply while executing a transaction or on account of a change of residence. It could be visa and citizenship rules; laws pertaining to family and marriage; labour, and social security regulations/norms. These laws should be considered for India as well as the host country.

38 Geopolitical, Economical, and Cultural Considerations / Challenges

Moving base has its own set of challenges. Certain personal factors can be dealt with by the individual concerned to a large extent. However, such individuals should also appreciate that there are several factors which are beyond their control. These relate to the economic situation of the country they are moving to the cultural change they or their family members must deal with. Further, the global geopolitical environment has seen dramatic upheavals in the last decade. Apart from the economic and legal considerations, one should also keep the geopolitical developments in mind, especially in relation to India and the host country where they are migrating to or from.

Conclusion

One can see that a change of residence leads to a substantial change in the tax liability, compliances, and regulatory provisions applicable to the person. Further, the Income-tax and FEMA laws themselves have grey areas, with differing views between various stakeholders causing prolonged litigation. When we bring in laws of another country and their interplay with Indian laws to the same transaction or income, it leads to increasing complexities, contradictions, and uncertainties. When a person shifts residence from abroad to India or from India to abroad, the whole legal position surrounding the person takes a 180-degree turn. It is like turning the table halfway through in a game of chess! In such cases, it is ideal to consider all the legal implications in advance, so that informed decisions can be taken. Otherwise, it could happen that the person is “physically” moving to a particular location with several plans in mind, but “legally” spearing into uncharted territory with far-reaching consequences.