TALK ON ‘ACHIEVING SUCCESS – LIVING VALUES’

The H.R. Committee, along with the RVG Educational Foundation, organised a talk for the benefit of students and young members on 24th November, 2019 at the RVG Hostel Auditorium. Mr. M.K. Ramanujam addressed the gathering on ‘Achieving Success – Living Values’ in his eloquent style and in an interactive session.

He started his talk by explaining the difference between success and happiness. Success, he said, invariably refers to targets, milestones, goals, etc. But happiness is born out of love, abundance and inspiration. Therefore, one ought to choose to do something out of inspiration and love for a subject, for a career, for one’s dreams and so on. ‘Success’ is a challenge because it is short-lived. One often postpones happiness till one achieves success. Happiness, on the other hand, flows from inspiration during the process of achieving it; and despite the challenges, one remains cheerful.

Mr. Ramanujam explained the acronym ‘PREMA’ and the most important concept of ‘Purpose’.

‘P’ Stands for positive emotions. One must venture out with positive emotions. Negative emotions are like Velcro that gets fixed to us easily. We should not be like Velcro but like a Teflon coating so that we are not stuck to negative emotions. For a daily practice of positive emotions it would be best to remember and note down at least three nice things that happened during the day and objectively assessing why these felt like positive happenings.

‘R’ Stands for Relationships. One must invest time, effort, energy and willingness in building relationships with nature, friends, teachers, seniors, the environment and everything around. They are the best support systems.

‘E’ stands for Engagement. Give your best. Introspect and ask yourself, why are you doing what you are doing? Put all your energy into whatever you are doing. Even if you are compelled to do certain things that you do not want to do (e.g., due to parents’ pressure), put in your best. Love what you do and do what you love. Put your 100% and think beyond your own self. Think what contributes to your happiness… Expand your horizon.

‘M’ stands for Meaning. In all that you do, you ought to have meaning for the self and for all those concerned

with it.

‘A’ stands for Achieving. You must complete what

you have begun. There is joy in finishing and

achieving things.

Purpose: Everything in the universe is driven by purpose. Align your work with the purpose. Clarity of ‘Why’ lightens the burden of ‘How’ and ‘What’. Purpose can be understood with deep introspection with ’Why’ and values can be understood by questioning ‘How’. Success is what others measure in you and happiness is what you measure in yourself.

One hundred and ten participants, including more than 80 students, attended and enjoyed the talk.

President Manish Sampat welcomed the participants and gave information about the Society and also shared its vision. Chairman Rajesh Muni provided a broad outline of the activities of the H.R. Committee, especially those carried out for the benefit of students. He invited and encouraged students to register and participate in the Study Circle and the Students’ annual programmes which enable students to showcase their talents.

Mr. Lalchand Chaudhari, President of the RVG Foundation, shared information about the number of chartered accountants who had benefited as alumni of the hostel. He also shared the ‘Vision 2024’ plan set out for RVG. Mukesh Trivedi proposed the vote of thanks.

WORKSHOP ON NBFCS

The NBFC sector has been facing several challenges of late. Apart from business and regulatory challenges, it is also confronted with challenges in Ind AS implementation and other compliances of ECL provisioning and disclosure, etc. Further, regulatory norms are also being notified on a frequent basis.

The Accounting and Auditing Committee of the BCAS has always been at the forefront in planning programmes for NBFCs in order to bolster them and to equip professionals to deal with challenges. Accordingly, the Committee conducted a ‘Workshop on NBFCs’ on 13th December, 2019 at Hotel Orchid, Mumbai to have an in-depth discussion on the current developments in the field from the regulatory perspective and various issues arising from first-time Ind AS implementation.

It was structured into five sessions followed by a panel discussion. The technical sessions dealt with a variety of topics such as Key regulatory updates in the NBFC Sector, Financial Instruments, Applying the ECL Model and related disclosure requirements, Disclosure requirements under Schedule III of the Companies Act, 2013, Statutory audit aspects, followed by an interesting panel discussion on Challenges of first-time adoption of Ind AS.

The Workshop was attended by more than 80 persons, with increased participation from the industry.

The Workshop started with an inaugural address by Samir Kapadia, BCAS Hon. Joint Secretary, who stressed the importance of NBFCs in the overall development of the financial sector in India. Himanshu Kishnadwala, Chairman of the Committee, introduced the structure of the Workshop to the participants, the thought process behind its design and the need for such a Workshop.

The first session was conducted by Bhavesh Vora who dealt with the important aspects of key regulations surrounding NBFCs and the recent changes therein. While dealing with these, he also took participants on a journey of the NBFC sector over a period of time and gave valuable insights into the regulatory impact on various categories of NBFCs.

In the second session, Santosh Maller dealt with Financial Instruments, Classification of Financial Instruments based on the business models and the measurement of various Financial Instruments with several examples for ease of understanding.

Rukshad Daruvala, who conducted the third session, took up the key issues and requirements in applying the Expected Credit Loss (ECL) model dealing with the provisioning requirements of Advances of NBFCs.

Post lunch, Rukshad Daruvala was once again at the helm, at the session on Disclosure Requirements under Schedule III, including various critical disclosures required under the Ind AS regime.

The subject of Statutory Audit aspects was dealt with in the fifth session by Jayesh Gandhi. He discussed in detail the requirements while conducting audit of NBFCs and shared his vast experience with the participants as

he explained the importance of Audit in the current economic scenario.

In the final session, the challenges of first-time adoption of Ind AS were discussed by a panel comprising Govind Jain, Jayesh Gandhi and Haren Parekh. The discussion was ably moderated by Ashutosh Pednekar. It revolved around the first-time adoption challenges faced by the NBFC industry and the auditors’ perspective on the same. The panellists shared their practical experience on the subject for the benefit of all participants.

TRAINING SESSION FOR CA ARTICLE STUDENTS

The Students’ Forum under the auspices of the H.R.D. Committee organised a training session for CA article students on ‘Recent Developments in Income Tax’ on 10th January, 2020 at the BCAS Hall.

It was conducted by Jayna Shah. Ms Dhristhti Bajaj, the student coordinator, introduced the speakers and described the upcoming events for students.

Anand Kothari, Convener of the H.R.D. Committee, welcomed the speakers and presented them with a memento each.

Jayna Shah explained the various amendments in income tax such as the change in the corporate tax rate, introduction of faceless assessment, changes to boost cashless economy, new provisions and amendments in TDS provisions and so on. It was an interactive session and the speakers answered all the queries raised by the participants.

The training session ended with Student Study Circle Coordinator Dnyanesh Patade proposing the vote of thanks to the speakers and also to the participants.

NANI PALKHIWALA MEMORIAL LECTURE

The Nani Palkhiwala Memorial lecture meeting was organised jointly with the Forum of Free Enterprises at NCPA Tata Theatre on 16th January, 2020.

Mr. N. Chandrasekaran, Chairman of Tata Sons Ltd., who was the guest speaker, dwelt on the subject ‘Building India for the Future’. Mr. Y.H. Malegam presided over the proceedings.

A documentary film, ‘Nani the Crusader’, was screened at the start of the meeting. It was based on the life of the late Mr. Nani Palkhiwala and showed glimpses of his life, his rise in the legal fraternity and the accolades that he won from all quarters on account of his brilliance. It also threw light on some of the major cases on Constitutional matters that he had won and that saved India’s democracy and shaped the country’s future.

The film screening was followed by the release of a book, ‘Essays & Reminiscences’ in honour of Mr. Palkhiwala. Mr. Arvind P. Datar, the general editor of the book, fondly recalled his vivid memories of the late stalwart.

Mr. Chandrasekaran spoke of suspicions and ‘micro-management’ of the economy as the impediments faced by businesses in India. He stressed on the need for creating a harmonious atmosphere by trusting and treating business as an essential pillar for

nation-building. The Tata group was an excellent example of how business can contribute to nation-building. Mr. Palkhiwala had set an example of how businesses, by maintaining their core values, could co-exist in a competitive economy and had helped government to build the present-day India. This happened because even his strictest criticism was taken in a positive spirit and with implicit trust by the government.

The core thrust of Mr. Chandrasekaran’s speech was how, with the co-operation of business and government, the vast potential of India could be tapped and the benefits of growth could reach the poorest segment of people to build a strong India, making its future

extremely bright.

Mr. Deepak Parekh, HDFC Bank Chairman, while proposing the vote of thanks, called for maintaining the values of the Indian Constitution. Pointing out that ‘while times and circumstances change, strong values and principles do not’, he said that while we should hold on to the learnings that Mr. Palkhiwala had left behind, it was important not to be consumed by ‘pessimism and doom-mongering’. Admitting that he was an optimist, he said he was confident about the future of India and that ‘our youth will see India’s best days’.

SEMINAR ON PRESUMPTIVE TAXATION

The Taxation Committee organised a seminar on ‘Presumptive Taxation’ with several distinguished speakers sharing their deep knowledge on the subject. It was held at the Walchand Hirachand Hall of the IMC on 18th January, 2020. The event attracted overwhelming response and saw an attendance of 111 participants, including outstation participants from five different cities / towns. President Manish Sampat welcomed the attendees and gave the opening remarks.

The following topics were taken up for discussion by the speakers:

| Sections 44AD and 44ADA: – • Purpose of the provision • How is it different from section 28 – 43CA • Assessee to offer business income under this section • Assessees who cannot offer income under presumptive taxation • Maintenance of books of accounts• Calculations of gross receipts• Determination of GR without BOA and case studies |

Bhadresh Doshi |

| Sections 44AE, 44AF, 44BB, 44BBA, 44BBB – Purpose of the sections, applicabiltity, issues, recent jurisprudence – Interplay of tax audit – Case studies |

Mehul Shah |

| Brain trust questions – Presumptive taxation issues –Issues concerning return of income, books of accounts, tax audit, assessments, penalties, ICDS, etc. |

Gautam Nayak,

Anil Sathe and Kinjal Bhuta |

In the first session, Bhadresh Doshi highlighted the technical aspects of sections 44AD and 44ADA. He concentrated on various issues arising right from the time of the introduction of the presumptive taxation scheme under these two sections. He gave his views and insights on multiple issues and explained the jurisprudence affecting them. He advised participants to read and understand the section and scheme and not to rely on general perceptions.

On his part, Mehul Shah dwelt on the presumptive basis of taxation under sections 44AE, 44AF, 44BB, 44BBA and 44BBB. He explained sections with the help of case studies. It was a highly interactive session and the speaker answered all the questions posed by the participants.

Gautam Nayak, Anil Sathe and Kinjal Bhuta were the ‘brain trustees’ for the last session that was moderated by Ameet Patel. The ‘brain trustees’ were allotted specific questions based on various issues raised by BCAS members from time to time.

Starting the session, Gautam Nayak gave his views on whether presumptive taxation provisions under sections 44AD and 44ADA are qua assessee or qua income. He also responded to various issues raised by the participants pertaining to sections 44AD and 44ADA.

Anil Sathe gave his views on fundamental issues concerning the presumptive basis of taxation and responded to questions based on real examples. He also gave his views on issues concerning sections 44AE and 44BB.

Finally, Kinjal Bhuta shared her insights while addressing questions relating to important definitions such as eligible business, etc. under the presumptive basis of taxation. She also elaborated on the overall scheme and answered queries related to return of income for assessees adopting the presumptive basis of taxation.

All the sessions were interactive and the speakers shared their insightful views. The participants benefited immensely from the guidance and practical views on various issues offered by the faculties.

NFRA AND PCAOB – DISSECTING

PERFORMANCE EVALUATION OF AUDITS

A lecture meeting was organised on 22nd January, 2020 in the BCAS Conference Hall to deal with the above topic. It was addressed by Chirag Doshi who went through the process of inspection by the Public Company Accounting Oversight Board (PCAOB) of a firm’s quality controls and review of audit assignments carried out by that firm.

He provided an overview of the functioning of the PCAOB with its top areas of focus during the exercise of a firm’s quality review process. The major focus areas were:

(i) System of quality control in firms;

(ii) Independence;

(iii) Recurring audit deficiencies relating to ICFR, Revenue Recognition, Allowance for loan losses, Other Accounting Estimates and ROMMs.

The review process is split into two parts, viz., Quality Control Review and Audit Engagement Review. The major focus is on compliance with auditing standards and not the accounting standards.

Chirag Doshi dwelt on the on-field procedure for review as well as the procedure after field reviews and highlighted the thorough professionalism and independence involved in the whole review process.

He then dealt with the National Financial Reporting Authority (NFRA) which has been constituted on the lines of the PCAOB with the objective of monitoring and enforcing compliance with auditing standards. For achieving this objective, the NFRA would be reviewing the working papers of the audit firms and other communication related to the audits to evaluate the sufficiency of the quality control system of the auditor.

Chirag Doshi went on to deal with the first report of NFRA in the form of an Audit Quality Review (AQR) Report in the case of the auditee, ‘IL&FS Financial Services Limited’ for the F.Y. 2017-18. The purpose of discussing the findings was to make the members aware of the necessity to document and to put on record the findings during the audit process in such a manner that it goes on to prove the independence of the auditor as well as displaying adequate professional scepticism during the conduct of the audit process.

He provided inputs for creating an in-house audit manual by small and medium-size firms for the efficient conduct of audit.

The meeting was well attended and attracted a full house.

FEMA STUDY CIRCLE

Here is a brief report on the FEMA Study Circle meeting held at the BCAS Conference Hall on 23rd January, 2020.

Ms Mitali Pakle’s presentation was comprehensive and lucid in nature and covered a variety of case laws that made it easy for everyone to grasp the subject matter being discussed. In the course of her brief talk, the speaker managed to cover various aspects of the ECB Guidelines and made it quite interesting.

The discussion was further enriched by some thought-provoking questions that the participants posed and the answers provided by the speaker.

DTAA COURSE 2019-20

The 20th Study Course on Double Taxation Avoidance Agreement was conducted at the BCAS Hall over nine days – 13th, 14th, 20th and 21st December, 2019 and 4th, 5th, 11th, 12th and 25th January, 2020.

Thanks to regular feedback and continuous refinement, the Study Course was re-designed and covered all BEPS and MLIs along with the Articles of DTAA, FEMA / GAAR, Transfer Pricing, Source Rules under the Income-tax Act, 1961, TDS u/s 195, Substance vs. Form and other relevant provisions.

All the lectures delivered by 31 eminent faculties were very well received. The faculties were generous in sharing their experience by way of case studies on critical topics such as residence and PE, as well as the amendments sought to be made through the MLI.

The Study Course was attended by 73 participants from diverse backgrounds such as senior professionals, practising CAs, young professionals associated with big and SME accounting firms and so on. Apart from Mumbai, there were registrations from other cities such as Ahmedabad, Baroda, Chennai, Jaipur and Delhi. All of them contributed to making the course a huge success.

For those who came in late, the Study Course is an eagerly-awaited event amongst the practitioners of international taxation from all over the country and was well received and appreciated. It was coordinated by Maitri Ahuja and Mahesh Nayak.

‘INDIAN PRIVATE TRUSTS – TAX AND FEMA ASPECTS’

The International Taxation Committee arranged a meeting on ‘Indian Private Trusts – Tax and FEMA Aspects’ on 28th January, 2020 at the BCAS Conference Hall. The meeting was led by Group Leader Naresh Ajwani who explained the far-reaching income tax and FEMA implications in case of trusts.

The speaker walked the audience through the provisions of income tax and FEMA on trusts and explained various basic terms, the genesis of trusts, kinds of trusts, ownership of trust property, AOP / BOI taxation, beneficial interest, beneficial ownership and other provisions. With the help of some simple illustrations, he explained various concepts and particulars – including terms that do not exist in Indian law such as ‘Trust is not a person’, ‘Grantor Trust’, ‘Trustee taxable as Representative Assessee’ and so on.

Naresh Ajwani also dealt with and answered queries raised by members of the audience. The meeting was interactive and the participants received enormous benefit from the discussion and the insights provided.

Acknowledging the importance of the subject, the Committee plans to host another meeting on trust provisions, details of which will be shared with members very soon.

FELICITATION OF YOUNG CAS AND ‘VISION 2020 – SHAPING THE FUTURE’ FOR NEWLY-QUALIFIED CAS

A special programme was organised for the newly-qualified Chartered Accountants (emerging successful from the November, 2019 examination) under the aegis of the Seminar, Public Relations and Membership Development (SPR&MD) Committee. But within a few days of the announcement, the online enrolments crossed the record figure of 300, forcing BCAS to close registrations!

The event was held at the BCAS Hall on Friday, 31st January, 2020. It attracted a full house of over 190 participants, including some walk-ins. They were greeted at the registration desk with a few BCAS publications – ‘Changing Paradigms for CSR in India’, a ‘Monograph Series’ containing five booklets on various laws, a copy of the BCAJ Journal of the last two months and BCAS membership forms.

The evening started with a one-on-one interactive session focussed on mentoring with eminent mentors, Nandita Parekh and Robin Banerjee. The participants were divided into two groups between the speakers so that they could interact and take help from them on all their queries, including guidance for future careers. These sessions were appreciated by all the newly-qualified CAs.

This was followed by an address by President Manish Sampat who talked about his early days as a qualified Chartered Accountant, the sound advice that he had received from his seniors to associate himself with the BCAS, the positive impact that the Society had had on his career as a CA – and to the present day when he heads the Society as President. He also briefed the new CAs on the various initiatives of the Society.

Narayan Pasari, Chairman of the SPR&MD Committee, pointed out that the youth or ‘yuva shakti’ is an integral part of the numerous activities organised by the BCAS. He appealed to the new CAs to become members of BCAS, benefit from it and play an active role in its innumerable activities. He pointed to the BCAS Referencer, the Annual RRC and the other programmes conducted in the last few months and said that youth had contributed significantly in all these events.

He proudly revealed that the BCAS is very active on social media and its handle @BCASGlobal has recently crossed the 33K mark; it also has 11K followers each on LinkedIn and YouTube.

The ‘Thought Leader’ for the evening, Nilesh Vikamsey, then took the floor and offered valuable advice to young CAs from the variegated learnings of his own life. He spoke at length on upcoming fields for CAs and stated that he believes ‘ABCD is the future’ – that is, Artificial Intelligence, Block Chains, Cyber Security and Data Analytics.

He also answered all the questions posed to him by the newly-minted CAs. He advised them to join the nearest Study Circles and pointed out that at an association like BCAS, the process of learning never stopped.

This was followed by a felicitation ceremony, with all the participants being presented with a memento by ‘Team BCAS’. The event showcased the vibrancy of the participants, many of whom showed great interest in signing up to become members of the Society.

Interestingly, some of the participants were eager to ask even more questions to their Mentors. The proceedings ended with a vote of thanks proposed by the coordinator, Rimple Dedhia.

18TH RESIDENTIAL LEADERSHIP RETREAT

The 18th Residential Retreat programme was held on 7th and 8th February, 2020 on the theme ‘Future Begins Now’. Twenty-nine participants, including ten newcomers, had registered for the programme. The trainer, Mr. Deepak Shinde (a disciple of Shri Mahatria), had flown in from Bengaluru for the event.

A cool winter breeze flowing over the green, serene and spacious campus, amidst the shade of swaying trees and the chirping of birds, set the perfect tone for the Retreat, which was held at the Rambhau Mhalgi Prabodhini, Essel World Road, Uttan.

The programme commenced with the invocation prayer. President Manish Sampat welcomed the participants and shared information about the activities of the BCAS. He proudly narrated his journey at the Society which had begun many years ago as Convener of the Human Resource Committee. He complimented the participants and the organising team for devising such an interesting workshop.

Trainer Deepak Shinde discussed several important concepts and pointers of life with the participants over the two-day Retreat.

He opened with the story of Alexander the Great King and the Saint Diogene, driving home the point that to become king or to achieve something, one has to put in huge efforts. But to be like Saint Diogene (and in permanent bliss) one need not depend on external things. One can be in that state quite naturally. To be happy, one must adhere to right values. One can be an achiever, become successful and also remain blissful like a saint.

His advice was to always begin the day with the greeting ‘Happy Morning’. Doing this all 365 days of the year would turn it into a habit. And one would not need to depend on people, places, objects, time, or seasons to be happy. If one was dependent on such external factors, the happiness would be temporary and external factors would make one subservient and vulnerable to them.

‘We have a tendency to judge people with our own biased and limited vision. In doing so we miss to be in touch with people and miss happiness. One’s life must be full of happiness and love, such that the epithet on one’s grave describes one’s life with apt, inspiring and happy words.’

In the second session, Trainer Deepak Shinde spoke about perfect balance and alignment of the laws of nature and man’s tendency to interfere. He used the simile of a Rubik’s Cube. At the beginning it is perfectly balanced with each of six sides uniformly reflecting one colour. The moment one turns, twists and revolves the cube, the entire symmetry of colour and pattern gets disturbed. The learning from this is not to interfere with the well-aligned laws of nature.

He then moved to thoughts and words. One becomes as one thinks; similarly, as one feels, so one attracts. He discussed at length the power of positive words and prayers and said that cheerfulness, abundance, gratitude, appreciation, encouragement and inspiration bring happiness and energy.

The third, evening session, was conducted in the open amphitheatre area, in the lap of nature, and the Trainer discussed peace vs. prosperity. He emphasised that one must clearly define what one wants in life. To earn peace and goodwill, one may come under pressure to sacrifice one’s own space. On the other hand, to enjoy material wealth one may have to compromise with values, goodwill and peace. The question was how to balance both, peace and prosperity? By using positive words and feelings, one can be in harmony and have perfect balance, he stressed.

Practising grace. Grace is one’s ability to carry out an act without disturbing the environment. ‘With grace, accept the outcome of action, inaction and efforts as a gift of the Lord (prasad buddhi).’

Late in the evening on the first day, the participants enjoyed a brilliant campfire. Some of them took to singing and dancing to music. The relaxed participants appeared charged up for the next morning’s session.

The first session on the second day began quite early, at 7 o’clock, in an open area witnessing the rising sun and its golden glow. The discussion turned to ‘Faith’ and ‘Energy’. Faith is something invisible with strong conviction of its presence. Trainer Deepak Shinde called faith the thread of a kite flying high in the sky. It is the connection with the thread that keeps the kite (symbolising life) flying high in the sky.

He explained the ‘God concept’ with cause and effect principles. One draws energy from the effulgence of the sun and knowledge; exercise and sattvik food for the body, positive words and prayer for the mind; and reflection, contemplation and meditation for the intellect. Energy charges the sub-conscious mind. ‘Therefore, live with grace and align with nature with faith and receive energy’.

Narrating a conversation between Lord Rama and Hanuman, he shared the view that our faith in the Lord is much more powerful than the Lord. ‘God is the symbol of love. One need not have fear of the Lord.’

In the third session, the discussion focused on relations, expectations and situations. In life sometimes one may need to take a U-turn from one’s position. One ought to understand the people around, understand that man expects happiness and woman, love. But both love and happiness are complementary. Learn to say no without guilt and not to please others.

The two-day programme concluded with a vote of thanks.

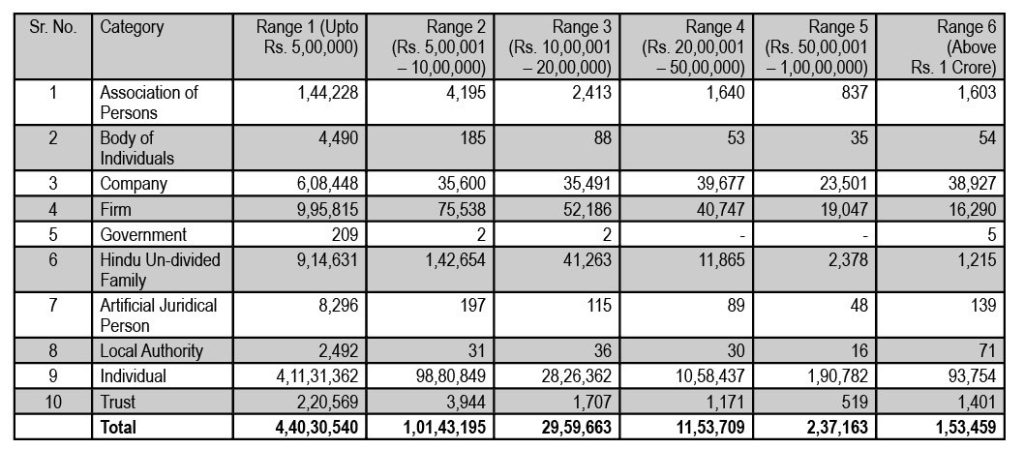

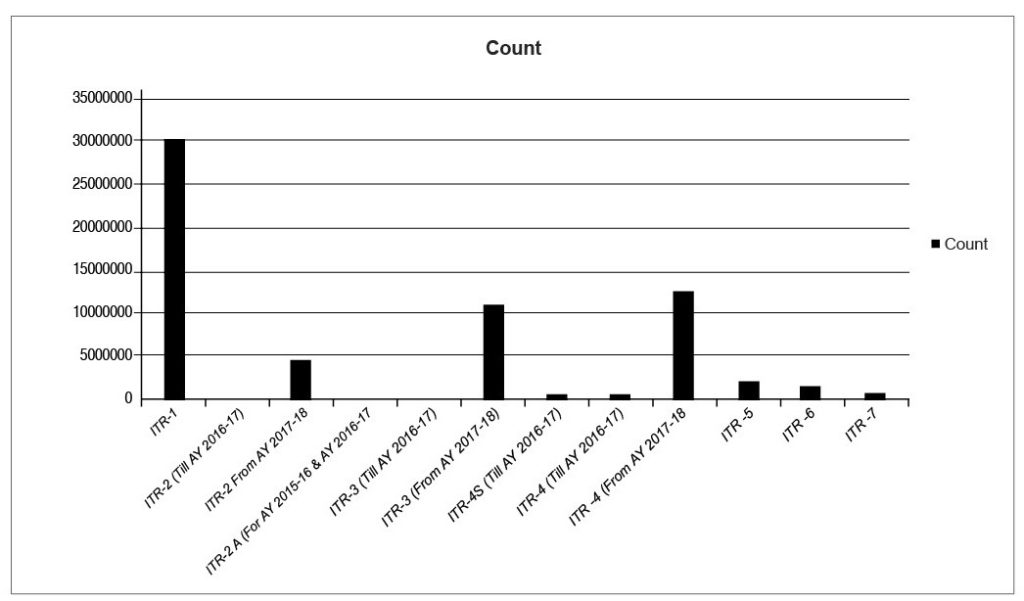

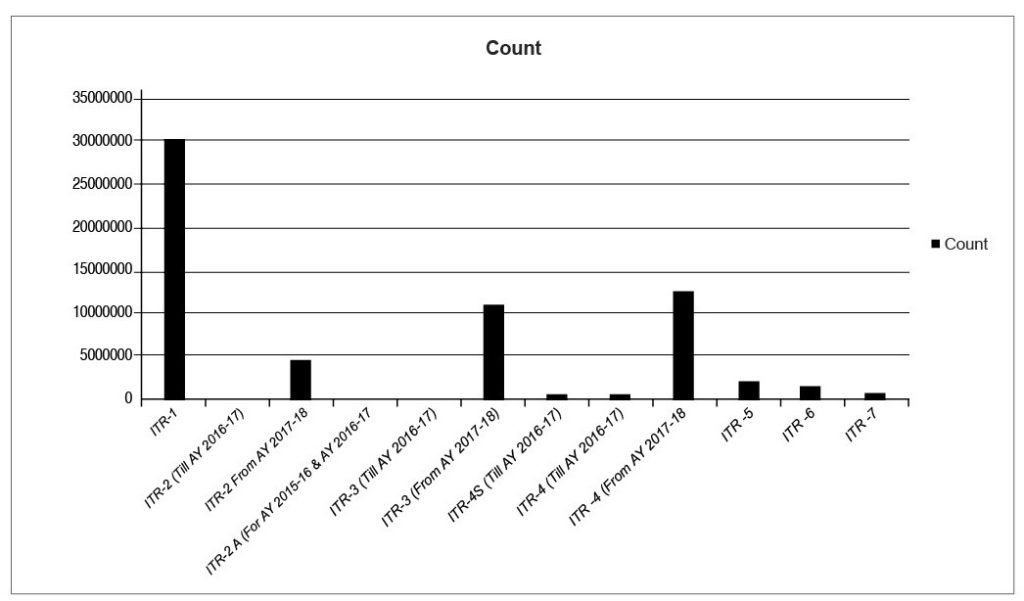

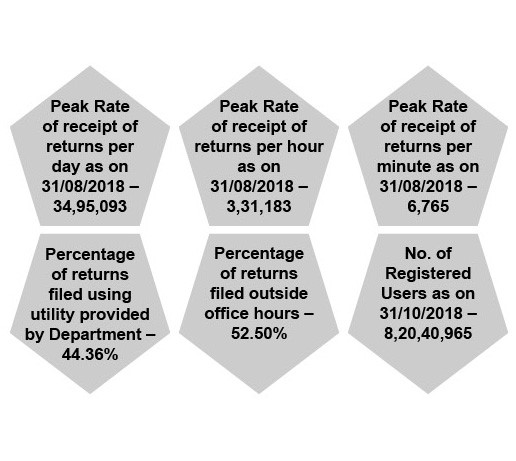

Source: www.incometaxindiaefiling.gov.in

Source: www.incometaxindiaefiling.gov.in Source: www.incometaxindiaefiling.gov.in

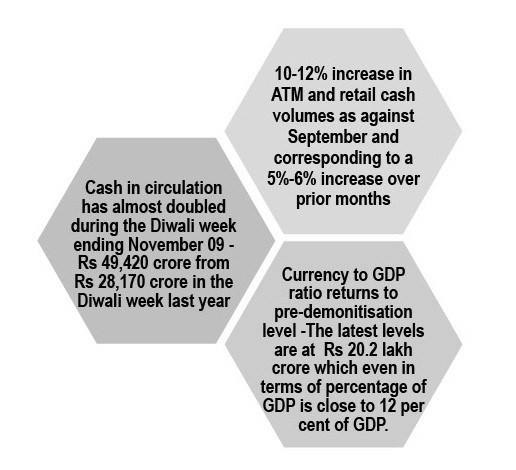

Source: www.incometaxindiaefiling.gov.in Source: Economic times

Source: Economic times

– educating them on how to think using science. This helped them differentiate between chinta and chintan

– educating them on how to think using science. This helped them differentiate between chinta and chintan  i.e.going to root cause, understanding real problem and find appropriate resolution.

i.e.going to root cause, understanding real problem and find appropriate resolution. – The Seven pillars:

– The Seven pillars: – The King – Leader

– The King – Leader – The Minister

– The Minister – The Country – Your Market / Client / Customer

– The Country – Your Market / Client / Customer – Fortified City – The Head Office

– Fortified City – The Head Office -The Treasury

-The Treasury – The Army – Your Team

– The Army – Your Team – The Ally – Mentor / Friend / Consultant

– The Ally – Mentor / Friend / Consultant