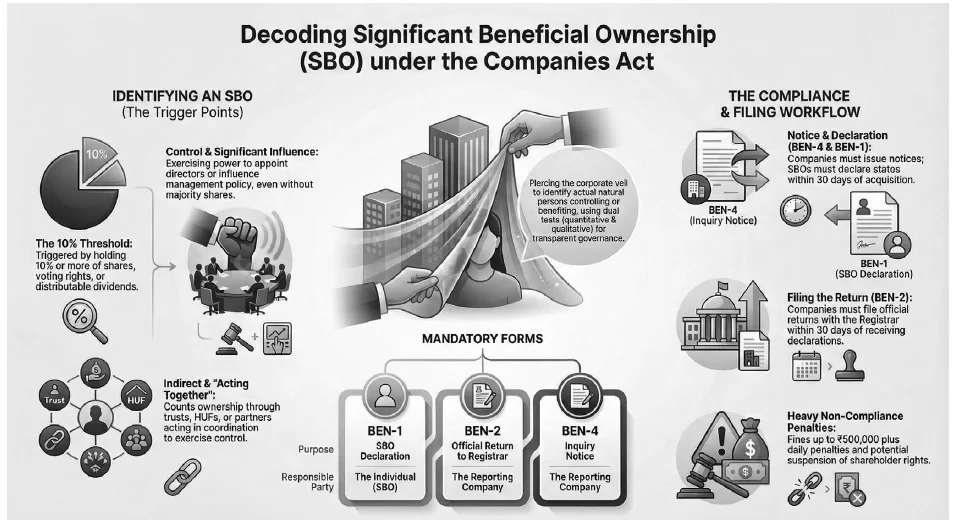

The Significant Beneficial Ownership (SBO) framework under the Companies Act 2013 identifies natural persons who ultimately control companies, preventing corporate misuse. SBO status triggers via a dual-test: a quantitative threshold of 10% indirect or combined shareholding, voting, or dividend rights, or a qualitative test of exercising “control” or “significant influence”. Companies must seek SBO details (Form BEN-4), SBOs declare interests (Form BEN-1), and companies notify the Registrar (Form BEN-2). Non-compliance invites steep penalties and NCLT restrictions on dividend and voting rights. Recent rulings against Samsung and LinkedIn underscore strict enforcement regarding indirect group control.

Significant Beneficial Ownership (SBO) represents one of the most critical compliance requirements under the Companies Act 2013 (CA 2013), aimed at identifying the natural persons who ultimately control or benefit from companies, thereby preventing misuse of corporate structures for illicit purposes. Following recommendations from the Financial Action Task Force (FATF) and the Company Law Committee, India introduced the SBO regime through the Companies (Amendment) Act 2017, which substantially amended Section 90 of the CA 2013. The regime underwent further refinement through the Companies (Significant Beneficial Owners) Rules 2018 (SBO Rules), subsequently amended in 2019, and further refined for Limited Liability Partnerships

(LLPs) in 2023, establishing a comprehensive framework for identification, declaration, and ongoing compliance.

This article provides a detailed examination of the SBO provisions, including identification criteria, trigger points, compliance procedures, and practical examples demonstrating various scenarios where SBO obligations are triggered.

1. UNDERSTANDING THE SBO FRAMEWORK

1.1 Statutory Definition and Scope (What is an SBO)

Section 90 of the CA 2013 establishes a comprehensive framework for identifying and reporting significant beneficial ownership.

Section 90(1) of CA 2013 reads as under:

(1) Every individual, who acting alone or together, or through one or more persons or trust, including a trust and persons resident outside India, holds beneficial interests, of not less than twenty-five per cent. or such other percentage as may be prescribed, in shares of a company or the right to exercise, or the actual exercising of significant influence or control as defined in clause (27) of section 2, over the company (herein referred to as “significant beneficial owner”), shall make a declaration to the company, specifying the nature of his interest and other particulars, in such manner and within such period of acquisition of the beneficial interest or rights and any change thereof, as may be prescribed:

Thus, every individual who, acting alone or together, or through one or more persons or trust (including trusts resident outside India), holds beneficial interests of not less than 25 percent (now 10 percent as per SBO Rules) in shares of a company or exercises the right to exercise or actually exercises significant influence or control (as defined in Section 2(27) of the Act), is required to make a declaration to the company.

However, the Companies (Significant Beneficial Owners) Rules 2018 have reduced this threshold to 10 percent, creating an important distinction between the statutory provision and the delegated legislation.

The definition of “significant beneficial owner” has been strategically broadened to encompass ultimate beneficial ownership, acknowledging that corporate structures often intentionally obscure the real owners behind multiple layers of corporate vehicles, trusts, and other entities. The legislation specifically contemplates an “extra-territorial reach,” applying to foreign registered trusts and persons resident outside India, thereby ensuring that sophisticated international structuring cannot circumvent Indian disclosure requirements. This approach aligns with global beneficial ownership disclosure standards promoted by the FATF and reflects India’s commitment to combating money laundering, terrorist financing, and other illicit financial activities.

1.2 Beneficial Interest under Section 89 and Section 90

A fundamental distinction exists between direct holdings and beneficial interests in the SBO framework. “Direct holding” refers to shares held in an individual’s own name as recorded in the company’s Register of Members, or shares in respect of which a declaration has been made under Section 89(2) of CA 2013. In contrast, “beneficial interest” encompasses a much broader concept defined in Section 89(10) of CA 2013, applicable to Section 90 of CA 2013 as well, extending to include the right to exercise any rights attached to shares or to participate in any distribution in respect of such shares, whether held directly or indirectly through any contract, arrangement, or otherwise.

This distinction is critical because the SBO Rules specifically exclude direct holdings as a sole basis for identifying an SBO, focusing instead on indirect holdings and the exercise of control or significant influence. This clarification, introduced through the 2019 Amendment Rules, ensures that the regime targets those who control companies from behind corporate veils rather than those whose shareholding is already transparent in the company’s register of members.

2. TRIGGER POINTS FOR SBO IDENTIFICATION:

2.1 Threshold-Based Trigger Points

The identification of an SBO is determined through a dual-test framework comprising both quantitative (objective) tests and qualitative (subjective) tests. The objective test primarily focuses on shareholding thresholds, while the subjective test examines control and significant influence exercised over the company.

2.1.1 The 10% Shareholding Threshold: Under the SBO Rules, an individual or a group of individuals triggers SBO status if they hold, either indirectly or together with direct holdings, not less than 10 percent of the shares of the company. This threshold represents the primary quantitative trigger point. For example, if Individual A holds 12 percent of the shares in his own name, he will not qualify as an SBO by virtue of direct shareholding even if it exceeds the 10 percent threshold. However, if Individual B directly holds 8 percent of shares and indirectly holds 3 percent through another entity, the aggregate holding of 11 percent would trigger SBO status.

2.1.2 Voting Rights and Dividend Participation: Beyond share capital, an individual is identified as an SBO if he holds, either indirectly or together with direct holdings, not less than 10 percent of the voting rights in shares. Additionally, an individual who has the right to receive or participate in not less than 10 percent of the total distributable dividend or any other distribution in a financial year, whether through indirect holdings alone or together with direct holdings, qualifies as an SBO. These alternative thresholds recognize that control over a company is not always exercised through share ownership but may be achieved through contractual arrangements that confer voting or dividend participation rights.

2.2 Control and Significant Influence:

Beyond shareholding thresholds, the SBO Rules establish a subjective test based on the exercise of control or significant influence. “Control” is defined in Section 2(27) of CA 2013 to include the right to appoint the majority of the directors or to control the management or policy decisions exercisable by a person or persons acting individually or in concert, directly or indirectly, including by virtue of shareholding, management rights, shareholders’ agreements, voting agreements, or any other manner. This definition is notably broad, extending control to those who influence policy through contractual arrangements rather than shareholding alone.

“Significant influence,” as defined in the SBO Rules, means the power to participate, directly or indirectly, in the financial and operating policy decisions of the reporting company but not constituting control or joint control of those policies. This intermediate category captures those who have substantial influence over company decisions without wielding decisive control.

For instance, an individual with the right to appoint one director (ensuring his presence is necessary to form quorum) would exercise significant influence but not control. Conversely, an individual with the right to appoint the majority of directors would exercise control.

These subjective tests are particularly important in identifying hidden beneficial owners in complex corporate structures where voting rights may be dispersed, or where control is exercised through management agreements or shareholders’ agreements rather than shareholding. The subjective test ensures that the SBO regime captures not only the formal shareholders but also the individuals who direct the company’s operations and strategic decisions.

2.3 Indirect Holding Mechanisms and “Acting Together” Concept:

2.3.1 SBO Identification Matrix:

Diverse Scenarios for SBO Identification Triggering Points

The SBO Rules establish detailed mechanisms for determining indirect holdings, recognizing that corporate structures often involve multiple layers of entities. An individual is considered to hold a right or entitlement indirectly in the reporting company if he satisfies one or more of the following criteria.

- Body Corporate Ownership: Where a shareholder in the reporting company is itself a body corporate (company or an LLP), an individual is regarded as indirectly holding the shares if he holds a majority stake in that body corporate or holds a majority stake in the ultimate holding company of that body corporate, whether incorporated in India or abroad. “Majority stake” means holding more than 50 percent of equity shares, voting rights, or the right to receive more than 50 percent of distributable dividend or other distributions. For instance, if Company X holds 30 percent of the shares in Target Company Y, and Individual C holds 60 percent of Company X, then Individual C’s indirect holding in Target Company Y would be calculated as 60 percent of 30 percent, equaling 18 percent.

- Undivided Family (HUF) Holdings: When a shareholder in a company is a Hindu Undivided Family, the Karta (the managing member of the HUF) is regarded as the natural person holding the beneficial interest. This provision recognizes that an HUF is essentially a family of natural persons holding shares collectively, and Karta, as the managing member, exercises control over those shares. If an HUF holds 12 percent of shares in a company and Individual D is the Karta, then Individual D would be identified as the SBO in relation to that shareholding.

- Partnership Entity Holdings: Where the shareholder is a partnership firm (including Limited Liability Partnerships), an individual or Group of Individuals is regarded as indirectly holding the shares if they meet any of the following conditions: (a) they are partners in that partnership firm; (b) they hold a majority stake in the body corporate where they are partners; or (c) they hold a majority stake in the ultimate holding body corporate of that partnership entity. The partnership provision acknowledges that partners collectively control partnership capital and profits.

• If Individual E holds 55 percent of a Limited Liability Partnership that holds 18 percent of the shares in Target Company Y, then since LLP is holding more than 10%, each partner is considered as an SBO.

• Take another situation. If Firm is holding more than 10% of ABC Private Limited (A). If Partner in the said firm is body corporate, then find an Individual holding more than 50% of the body corporate (B). Go up to the ladder find an Individual who holds more than 50% then he is an SBO (C). If no Individual meets the above criteria, then no SBO is identified in such a situation.

- Trust Holdings: In the case of trusts holding shares, the determination of indirect holdings varies depending on the nature of the trust. For discretionary trust (where beneficiaries have no fixed entitlements), the trustee is regarded as holding beneficial interest and would be identified as an SBO. This reflects the principle that the trustee exercises control over trust assets.

• For a specific trust or fixed-entitlement trust, the beneficiary or beneficiaries with entitlements are identified as holding beneficial interest.

• For a revocable trust, the author or settlor of the trust (the person who created and can revoke it) is regarded as the beneficial owner.

- Pooled Investment etc.: In case the Member of Reporting Company is (a) A Pooled Investment Vehicle (“PIV” i.e. Mutual Fund, Venture Capital Fund, etc.); or (b) An Entity Controlled by the Pooled Investment Vehicle (“Controlled Entity”), based in member State of the FATF on Money Laundering and the regulator of the securities market in such member State is a member of the IOSCO (International Organization of Securities Commissions). Further, the individual in relation to the Pooled Investment Vehicle is- (a) A General Partner; or (b) An Investment Manager; or (c) A CEO where the Investment Manager of such pooled vehicle is a Body Corporate or a partnership entity. However, where the PIV or Controlled Entity is based in a jurisdiction that does not meet the requirements above, the provisions of Explanation III (i) to (iv) to Rule 2(1)(h) of the SBO Rules, shall apply. PIV or Controlled Entity should be treated according to its legal form (as a company, LLP, trust, or HUF) and the company must identify all natural persons who, directly or indirectly, hold at least 10% of shares, voting rights, distributable dividends, or exercise control or significant influence over the reporting company.

2.3.2 The “Acting Together” Principle:

The SBO Rules introduce the concept of “acting together,” meaning natural persons who hold shares in concert or in coordination to exercise control or influence over the company. When several individuals act together, their shareholdings are aggregated to determine whether the combined holding reaches the 10 percent threshold. The critical element of “acting together” is not a general community of economic interests but rather a concerted exercise of control or significant influence specifically in relation to the target company. This togetherness is typically demonstrated through voting patterns, concerted acquisitions, holding of offices in concert, or explicit agreements (which can be formal or informal) to coordinate shareholding decisions.

For example, if Individual F holds 6 percent and Individual G holds 5 percent of the shares, but they have entered into a voting agreement under which they coordinate their voting decisions, their combined holding of 11 percent would trigger SBO status for both individuals.

3. IDENTIFICATION AND DECLARATION PROCEDURES

3.1 Initial Identification Obligations

Companies bear the primary responsibility for identifying SBOs within their shareholding structures. The Companies (Significant Beneficial Owners) Rules 2018, as amended in 2019, impose mandatory obligations on reporting companies to identify potential SBOs and solicit their declarations.

The identification process typically follows these sequential steps:

Step 1: Identification of Non-Individual Members: Every company must identify all non-individual members (entities such as companies, LLPs, partnerships, trusts) holding 10 percent or more shares, voting rights, or dividend participation rights. The company must then trace through these entities to identify the natural persons behind them, following the indirect holding mechanisms prescribed in the SBO Rules.

Step 2: Issuance of Form BEN-4 Notice: Upon identifying potential SBOs or non-individual members, the company must issue formal notice in Form BEN-4 to each such individual or entity, seeking information regarding their beneficial ownership status. The BEN-4 form is annexed with a blank declaration form (BEN-1) to facilitate response. This notice requirement applies both to members and non-members whom the company knows or has reasonable cause to believe may be SBOs. The notice period prescribed for response is 30 days from the date of notice.

Step 3: Receipt and Recording of Declarations: Upon receipt of declarations in Form BEN-1 from identified SBOs, the company must maintain a Register of Significant Beneficial Owners in Form BEN-3. This register must be open to inspection by members of the company upon payment of prescribed fees, ensuring transparency and accountability.

3.2 SBO Declaration Forms and Filing Requirements

The SBO compliance regime involves four primary forms, each serving a distinct purpose in the identification and reporting framework:

Form BEN-1 (Declaration by SBO): Every individual identified as an SBO is required to file a declaration in Form BEN-1 with the company, specifying the nature of his interest and other particulars as prescribed. The declaration must be submitted within prescribed timelines: (a) within 90 days of the applicability of the SBO Rules (a one-time filing for pre-existing SBOs), or (b) within 30 days of acquiring such SBO status in the future. Form BEN-1 captures detailed information regarding the SBO’s ownership structure, the mechanism through which they hold beneficial interest (direct, indirect through various entities, acting together, control, or significant influence), and confirmation of compliance with applicable laws.

Form BEN-2 (Return by Company to the Registrar): Upon receipt of a declaration in Form BEN-1, the company is mandated to file a return with prescribed fees to the Registrar of Companies in Form BEN-2 within 30 days of receiving such declaration. This return formally communicates the identification of an SBO to the regulatory authority, creating an official record of beneficial ownership disclosure. Form BEN-2 must be signed by a director, manager, CEO, Chief Financial Officer, or Company Secretary of the company and further certified by a practicing professional (Chartered Accountant, Company Secretary, or Cost Accountant) in whole-time practice. Filing delays result in additional fees as prescribed.

Form BEN-3 (Register of Significant Beneficial Owners): Every company must maintain and preserve a Register of Significant Beneficial Owners in Form BEN-3, comprising details of all individuals identified as SBOs. This register serves as an internal reference document documenting the company’s SBO identification exercise and is open to inspection by members and registered officials.

Form BEN-4 (Notification Letter to Potential SBOs): In accordance with Section 90(5) and Rule 2A of the SBO Rules, every company must issue a notice in Form BEN-4 seeking information regarding ultimate beneficial owners to (A) every non-individual member holding not less than 10 percent of shares, voting rights, or dividend participation rights, (B) any other person where the company has reasonable cause to believe that such member or person is SBO or, (C) has knowledge of the identity of a SBO or (D) was a SBO at any time during the immediately preceding three years.. This form initiates the identification process and gives potential SBOs an opportunity to disclose their status directly to the company.

3.3 Timelines for Compliance

The Companies (Significant Beneficial Owners) Rules 2018, as originally notified, established an initial one-time filing deadline of 90 days from the effective date (February 8, 2019) for all pre-existing SBOs to file their declarations. This transitional period recognized that companies with existing structures needed reasonable time to identify SBOs and facilitate their declarations. For new SBOs identified after this transition period, the timeline for declaration is 30 days from the date of acquiring SBO status. The company, upon receipt of an SBO declaration, must file the corresponding Form BEN-2 with the Registrar within 30 days. Importantly, delays in filing incur additional fees as prescribed under the Rules, creating a financial disincentive for non-compliance and encouraging timely reporting.

4. PRACTICAL EXAMPLES AND SCENARIOS

To understand the application of SBO provisions in diverse corporate structures, the following detailed examples illustrate various trigger points and compliance requirements:

4. 1 Direct Shareholding Exceeding Threshold

Scenario: Mr. Makrand holds 15 percent shares in ABC Private Limited, a private limited company. The shares are registered in his name on the company’s Register of Members.

Analysis: Although Mr. Makrand’s shareholding is direct and already visible in the Register of Members, since the 2019 Amendment Rules clarified that direct holdings of shares or voting rights are excluded from requiring mandatory declaration if the person is already on the Register of Members, Mr. Makrand would not need to file a separate BEN-1 declaration if he is already registered as a member holding 15 percent. The company would simply record this holding in the Register of Members.

Compliance Action: No separate BEN-1 filing required if registered member; no BEN-2 filing required as no additional disclosure is needed. (Mandatory Indirect Holding is necessary)

4.2 Indirect Holding Through a Single Corporate Layer

Scenario: Mr. Makrand holds 70 percent of the shares in Investment Company X Private Limited. Investment Company X holds 20 percent of the shares in Target Company Y Limited. Mr. Makrand is not directly registered as a member of Target Company Y.

Analysis: Mr. Makrand’s indirect holding in Target Company Y is calculated as 70 percent of 20 percent, equaling 14 percent. Since Mr. Makrand holds a majority stake (70 percent, which exceeds 50percent) in Investment Company X, which in turn is a shareholder in Target Company Y, Mr. Makrand’s holding through Investment Company X is regarded as an indirect holding under Rule 2(1)(h)(iii) of the SBO Rules. As his indirect holding exceeds the 10 percent threshold, Mr. Makrand qualifies as an SBO of Target Company Y.

Compliance Action: (1) Target Company Y must issue a Form BEN-4 notice to Investment Company X seeking information about ultimate beneficial owners; (2) Mr. Makrand must file a Form BEN-1 declaration with Target Company Y within 30 days from the notice date or 30 days of acquiring this status or within 90 days if pre-existing; (3) Target Company Y must file Form BEN-2 with the Registrar within 30 days of receiving Mr. Makrand’s BEN-1 declaration; (4) Target Company Y must record Mr. Makrand in its Register of Beneficial Owners (BEN-3).

4.3 Indirect Holding Through HUF

Scenario: Shetty Hindu Undivided Family holds 12 percent of the shares in XYZ Corporation Limited. Mr. Makrand Shetty is the Karta of this HUF and exercises management and control over the family properties, including this shareholding.

Analysis: Under Explanation III(ii) to Rule 2(1)(h) of the SBO Rules, where a shareholder in a body corporate is a Hindu Undivided Family, the individual who is the Karta of the HUF is regarded as the natural person holding the beneficial interest. Accordingly, Mr. Makrand Shetty, as the Karta of the Shetty HUF, is identified as the SBO in relation to the 12 percent shareholding held by HUF. The shareholding of 12 percent exceeds the 10 percent threshold, confirming Mr. Makrand’s SBO status.

Compliance Action: (1) XYZ Corporation Limited must identify the Karta of the HUF through the company’s records and/or issuance of Form BEN-4; (2) Mr. Makrand Shetty must file Form BEN-1 declaring his beneficial interest as Karta of the Shetty HUF; (3) XYZ Corporation Limited must file Form BEN-2 with the Registrar; (4) XYZ Corporation Limited must maintain the record in Form BEN-3.

Important Note: If Mr. Makrand Shetty holds an additional 5 percent of the shares in his personal name, his aggregate beneficial interest would be 12 percent (through HUF) plus 5 percent (direct), totaling 17 percent, which must be disclosed in his BEN-1 declaration.

4.4 Beneficial Interest Through Limited Liability Partnership

Scenario: Ms. Priya Sharma holds 60 percent of the capital contribution in Tech Innovations LLP. Tech Innovations LLP holds 15 percent of the shares in Software Solutions Limited. Ms. Priya is not a direct member of Software Solutions Limited.

Analysis: Under Explanation III(iii) to Rule 2(1)(h) of the SBO Rules, where a member (shareholder) in a company is a partnership entity, an individual is regarded as indirectly holding the shares if he is a partner holding a majority stake (more than 50 percent) in that partnership entity. Ms. Priya Sharma’s holding of 60 percent in Tech Innovations LLP constitutes a majority stake. Accordingly, her indirect holding in Software Solutions Limited is deemed to be 15 percent (the full holding of Tech Innovations LLP in Software Solutions Limited). Since 15 percent exceeds the 10 percent threshold, Ms. Priya qualifies as an SBO of Software Solutions Limited.

Compliance Action: (1) Software Solutions Limited must issue a Form BEN-4 notice to Tech Innovations LLP; (2) Ms. Priya Sharma must file Form BEN-1 disclosing her indirect holding through the LLP; (3) Software Solutions Limited must file Form BEN-2 with the Registrar; (4) Software Solutions Limited must maintain the record in Form BEN-3.

4.5 Control Through Board Appointment Rights

Scenario: Dr. Ravi Menon holds 8 percent shares of Healthcare Enterprises Limited. However, through a shareholder’s agreement, Dr. Ravi has the explicit right to appoint three directors out of a five-member board, thereby securing majority control of the board composition and management decisions.

Analysis: Although Dr. Ravi’s direct shareholding of 8 percent is below the 10 percent threshold, he exercises control over Healthcare Enterprises Limited through his contractual right to appoint the majority of directors. This control mechanism satisfies the subjective test under Rule 2(1)(h)(iv) of the SBO Rules, which identifies (as an SBO) any individual who has the right to exercise or exercises significant influence or control in any manner other than direct holdings alone. Dr. Ravi’s right to appoint three directors out of five constitutes control as defined in Section 2(27), exceeding the threshold for significant influence.

Compliance Action: (1) Healthcare Enterprises Limited must identify Dr. Ravi as an SBO based on his control through board appointment rights despite his below-threshold shareholding; (2) Healthcare Enterprises Limited must issue Form BEN-4 or directly request Form BEN-1 from Dr. Ravi; (3) Dr. Ravi must file Form BEN-1 disclosing his control mechanism and not merely his shareholding; (4) Healthcare Enterprises Limited must file Form BEN-2 with the Registrar specifying the basis of SBO identification as control, not shareholding; (5) Healthcare Enterprises Limited must maintain detailed records in Form BEN-3.

4.6 Acting Together – Coordinated Shareholding

Scenario: Mr. Rohan Desai holds 6 percent and Ms. Sneha Verma holds 5 percent of the shares in Retail Dynamics Limited. The two individuals have entered into a shareholders’ agreement which permits them to vote in unison on all company matters and to coordinate their shareholding decisions.

Analysis: Under the “acting together” principle, although neither Mr. Rohan nor Ms. Sneha individually meet the 10 percent threshold, their aggregate shareholding of 11 percent, combined with their commitment to exercise coordinated control through voting agreements, triggers SBO status for both individuals. The togetherness element is satisfied by their explicit shareholders’ agreement demonstrating concerted exercise of control. Each individual must be identified and declared as an SBO with specific reference to their acting-together arrangement.

Compliance Action: (1) Retail Dynamics Limited must identify both Mr. Rohan and Ms. Sneha as SBOs, noting their acting-together status; (2) Both individuals must file separate Form BEN-1 declarations, each specifying their 6 percent and 5 percent shareholdings respectively, along with a note indicating that they are acting together and the aggregate is 11 percent; (3) Retail Dynamics Limited must file two separate Form BEN-2 returns documenting the identification of each SBO; (4) Retail Dynamics Limited must maintain both individuals’ records in Form BEN-3 with clear indication of the acting-together arrangement.

4.7 Significant Influence Without Control

Scenario: Mr. Suresh Patel, a foreign investor, holds 8 percent of the shares in Manufacturing Corp Limited. Through his shareholders’ agreement, Mr. Suresh has the right to nominate one director to the board of five directors and has contractual rights requiring consultation on all acquisition, divestiture, and major capital expenditure decisions. However, he does not have the right to appoint the majority of directors or to control company policy unilaterally.

Analysis: Although Mr. Suresh does not hold 10 percent shareholding and does not exercise control (defined as the right to appoint majority directors), he exercises significant influence over Manufacturing Corp Limited. Significant influence encompasses the power to participate, directly or indirectly, in financial and operating policy decisions without possessing control or joint control. His rights to nominate one director require consultation on major transactions and participating in financial decisions constitute significant influence. This subjective test triggers SBO status despite his shareholding below the 10 percent threshold.

Compliance Action: (1) Manufacturing Corp Limited must identify Mr. Suresh Patel as an SBO based on significant influence through contractual arrangements; (2) Mr. Suresh must file Form BEN-1 specifying his 8 percent shareholding and explaining his significant influence mechanism; (3) Manufacturing Corp Limited must file Form BEN-2 with the Registrar; (4) Manufacturing Corp Limited must maintain detailed records in Form BEN-3 noting the basis of SBO identification as significant influence.

5. REGULAR COMPLIANCE AND ONGOING OBLIGATIONS

5.1 Maintenance of SBO Register and Updates

Once an SBO has been identified and declared, the company must maintain an up-to-date Register of Significant Beneficial Owners in Form BEN-3. This register must be preserved and made available for inspection by members, directors, and regulatory authorities upon payment of prescribed fees. The register must be open for inspection at the registered office of the company during

business hours, ensuring transparency in corporate governance.

Companies must also file information with the Registrar of Companies whenever there is a change in beneficial ownership. Any material change in an SBO’s holdings, control mechanisms, or identity triggers a new filing obligation. The concerned individual involved must file an updated Form BEN-1 within 30 days of the change, and the company must file a corresponding Form BEN-2 within 30 days of receiving the updated declaration. Changes include acquisitions or disposals of shares, changes in control arrangements, changes in the identity of the Karta of an HUF, changes in partnership composition, or changes in trust beneficiaries or trustees.

Additionally, companies are required to file regular returns with the Registrar and to notify the Registrar whenever an SBO ceases to have beneficial interest falling below the triggering thresholds. These ongoing compliance obligations ensure that the beneficial ownership information maintained by the Registrar of Companies remains updated and reflective of the actual ownership structures.

There has to be a mechanism in place with an SBO as well as the Company for understanding the changes in the Significant Beneficial Ownership since the provisions of Section 90 specifically state that the SBO shall make a declaration to the company, specifying the nature of his interest and other particulars, in such manner and within such period of acquisition of the beneficial interest or rights and any change thereof, as may be prescribed. In this situation, any kind of change in the particulars which are already declared needs to be declared again which imposes a lot of responsibility on the SBO.

SBO identification under section 90 and the SBO Rules continues to pose interpretational and practical challenges, especially for layered, cross-border and complex ownership structures. One needs to note the confusion between Section 90(4A) and Section 90(5) of CA 2013. Section 90(4A) casts an absolute duty on the company to identify SBOs, even without “reason to believe”, whereas section 90(5) is triggered only when such reason exists. Absence of a defined due diligence standard creates uncertainty when a company can safely say that it has discharged its obligation. Even when utmost care is taken for identification of SBOs, non-identification can expose the company to the penalties prescribed.

There can be a situation that after the analysis by SBO or by the Company there is no SBO who is traced and, in such circumstances, or in case the Company is not required to comply with the provisions of the Act as mentioned above, it would be prudent to have a noting of the same in the meeting of a Board of Directors of the Company. Also, just like annual disclosures received from the Directors for their interest and non-disqualification, the Company may have a mechanism of noting the no change in SBO declaration even though this is not specifically mentioned in the rules or Section.

6. PENALTIES FOR NON-COMPLIANCE

CA 2013 prescribes stringent penalties for non-compliance with Section 90 and the SBO Rules, reflecting the regulatory importance of beneficial ownership transparency. The penalty regime operates on multiple levels:

- Penalty on the Individual (SBO): If an individual fails to make the required declaration as an SBO or makes false or incomplete declarations, he is liable to a penalty of ₹50,000 and an additional ₹1,000 per day for continuing violations, up to a maximum of ₹200,000. The daily component creates a substantial financial disincentive for sustained non-compliance. If the individual willfully furnishes false or incorrect information or suppresses material information, additional consequences may follow under Section 447 of the CA 2013, which deals with fraud and carries criminal penalties.

- Penalty on the Company: If a company fails to maintain the SBO register, fails to file the required information with the Registrar, or denies inspection of the register to authorized persons, the company is liable to a penalty of ₹100,000 with an additional ₹500 per day for continuing violations, up to a maximum of ₹500,000. These enhanced penalties reflect the company’s greater ability to control compliance and its role as the custodian of beneficial ownership information.

- Penalty on Officers in Default: Directors and senior management personnel of the company who are in default with respect to the company’s obligations are liable to a penalty of ₹25,000 with an additional ₹200 per day for continuing violations, up to a maximum of ₹100,000. This provision ensures personal accountability of corporate decision-makers for non-compliance.

7. REGULATORY ACTIONS AND NCLT REMEDIES

Beyond penalties, Section 90(7) of the CA 2013 empowers the National Company Law Tribunal (NCLT) to issue orders imposing restrictions on shares held by non-compliant SBOs. If a person fails to provide information sought by the company through Form BEN-4 notice, or if the information provided is not satisfactory, the company may apply to the NCLT seeking an order directing that the shares in question be subject to the following restrictions:

- Restrictions on transfer of beneficial interest

- Suspension of voting rights

- Suspension of all dividend rights and other distributions

- Such other restrictions as may be prescribed.

These NCLT orders create significant practical consequences for non-compliant shareholders, potentially rendering their shares economically worthless by suspending dividend rights and preventing any monetization through transfer. This NCLT remedy mechanism provides a powerful enforcement tool for ensuring SBO compliance, as the consequences extend beyond monetary penalties to substantive restrictions on shareholder rights.

8. RECENT CASE STUDIES AND REGULATORY DEVELOPMENTS

8.1 Samsung Display Noida Private Limited Case

A significant regulatory development occurred in the case of Samsung Display Noida, where the Registrar of Companies (Uttar Pradesh) issued an adjudication order dated June 12, 2024, penalizing the company and its officers for violation of SBO disclosure requirements under Section 90 of CA 2013. Samsung Display Noida is a wholly owned subsidiary of Samsung Display Co. Limited (South Korea), which is in turn 84.8 percent owned by Samsung Electronics Co. Limited (South Korea). The company initially contended that because its shareholding was transparent (being entirely owned by Samsung Display Co.), no additional SBO declaration was required. However, the Registrar’s order rejected this position, holding that Samsung Display Noida failed to identify and declare the ultimate beneficial owners, including individuals residing outside India who exercised control through the corporate chains.

The Registrar specifically noted that the company failed to recognize that persons residing outside India hold beneficial interest in the reporting company, which falls squarely within Section 90(1) of CA 2013. The company was required to identify and declare specific natural persons holding controlling interests through the multi-layered structure, including the appointment of Mr. Lee (the director of Samsung Electronics) as an SBO. The Registrar’s order imposed aggregate penalties of ₹8,14,200/ on Samsung Display Noida Private Limited, its managing director, and other key managerial personnel for the default period of approximately 1,212 days.

Key Learning: This case establishes that companies cannot rely on transparent corporate shareholding alone to satisfy SBO obligations. Even where shareholding structure is entirely clear, companies must trace through non-individual members to identify and declare the ultimate beneficial owners, including foreign residents who exercise control through appointment rights, management decisions, or policy influence.

8.2 LinkedIn India Technology Private Limited Case

The Registrar of Companies (Delhi and Haryana) issued an adjudication order on May 22, 2024, determining that LinkedIn India and its parent entities failed to comply with SBO disclosure requirements. The order found that LinkedIn Corporation (USA) exercises control over LinkedIn India through its ability to influence the composition of the Indian subsidiary’s board of directors. This control was attributed to overlapping directorships and reporting structures within the corporate hierarchy. The Registrar further held that the acquisition of LinkedIn by Microsoft extended this control to Microsoft’s CEO, Satya Nadella. Consequently, both Satya Nadella and Ryan Roslansky (LinkedIn CEO) were deemed significant beneficial owners of LinkedIn India.

The order imposed penalties of approximately ₹27 lakhs on various individuals, including Satya Nadella and other executives. This order is particularly significant because it establishes that control exercised through board appointment mechanisms and corporate governance arrangements, even without direct shareholding, constitutes sufficient basis for identifying an individual as an SBO.

Key Learning: The LinkedIn order demonstrates that control and significant influence exercised at the group level, including through appointment of nominee directors and management hierarchies, triggers SBO status in subsidiary companies. This order has expanded the practical scope of SBO identification to encompass group structures with centralized management and board control.

The case highlights how crucial it is to openly disclose nominee directors, even if they are employees of the holding company. It suggests that if a holding company can stop its employees from being on a subsidiary’s board, those directors might be seen as nominees.

The Adjudicating Officer’s emphasis on “widespread control” through financial dealings and the authority given to parent company employees sets a standard for examining the real control that holding companies have over their subsidiaries, even when it looks like just administrative arrangements

This case is a big reminder for MNCs working in India to carefully review their corporate structures and beneficial ownership, making sure they follow Indian corporate laws, which might interpret “control” and “significant influence” more broadly than in other countries.

9. EXEMPTIONS FROM SBO DISCLOSURE

The SBO regime (through The Companies (Significant Beneficial Owners) Rules, 2018) provides specific exemptions recognizing that certain categories of investors operate under different regulatory regimes or pose minimal risk of misuse. Exempted Investors include:

- IEPF: The authority constituted under sub-section (5) of section 125 of the Act (Investor and Education Protection Fund)

- Holding Company of reporting company: Its holding company, provided that the details of such holding company shall be reported in Form No. BEN-2.

- Government Companies: Government Companies as defined under Section 2(45) of CA 2013 are exempted from the requirement to maintain and disclose SBOs, recognizing the public sector governance framework and parliamentary oversight.

- SEBI-Registered Investment Vehicles: Shares held by SEBI-registered investment vehicles such as mutual funds, Alternative Investment Funds (AIFs), Real Estate Investment Trusts (REITs), and Infrastructure Investment Trusts (InvITs) are exempt, reflecting the comprehensive regulatory oversight exercised by SEBI.

- Other Regulated Investment Vehicles: Investment vehicles regulated by the Reserve Bank of India, Insurance Regulatory and Development Authority of India, or Pension Fund Regulatory and Development Authority are also exempt, in view of their stringent ownership, disclosure, and supervisory frameworks.

These exemptions must be understood in the context of the SBO regime’s core objective of identifying natural persons exercising ultimate control. Exemptions are granted where the exempt entity itself operates under regulatory oversight that serves the same transparency and control objectives.

10. DISTINCTION BETWEEN SBO AND RELATED CONCEPTS

Understanding SBO is enhanced by distinguishing it from related concepts under CA 2013:

- Beneficial Interest (Section 89): While Section 89 requires disclosure of beneficial interests in shares and provides a mechanism for interested persons to declare beneficial interests to the company, it does not impose thresholds or identification obligations on companies. Section 89 is primarily a mechanism for voluntary disclosure by shareholders of beneficial interests when they exist.

- Section 90, by contrast, imposes mandatory obligations on companies to identify SBOs meeting specified criteria.

- Promoter Status: CA 2013 defines “promoter” as a person who has been instrumental in the incorporation of the company or has subscribed to its memorandum or contributed capital or property in kind during its establishment phase. While promoters typically hold substantial shareholding, not all promoters are SBOs (if their shareholding or control falls below thresholds), and conversely, not all SBOs are promoters (if they acquire beneficial interest post-incorporation).

- Related Parties (Section 2(76): Related party status under CA 2013 encompasses a broader category than SBOs, including parties related by virtue of subsidiaries, associates, joint ventures, key management personnel, and relatives of key personnel. While SBOs often fall within the related party classification, the SBO regime operates independently with its own identification and disclosure mechanics.

11. PRACTICAL COMPLIANCE CHECKLIST FOR COMPANIES

To ensure comprehensive and timely compliance with SBO requirements, companies should implement the following systematic compliance framework:

11.1. Identification Phase:

- Identify all members (including non-individual members) holding 10% or more of shares, voting rights, or dividend participation rights.

- For each non-individual member, determine the natural person(s) behind them through the prescribed indirect holding mechanisms.

- Identify individuals exercising control or significant influence through contractual arrangements, board composition rights, or management agreements.

- Document and trace multi-layered ownership structures to ultimate natural persons.

11.2. Documentation Phase:

- Maintain detailed ownership structure charts and supporting documentation.

- Prepare communications explaining SBO status and declaration requirements.

- Maintain copies of all Form BEN-4 notices issued along with proof of dispatch and responses received.

11.3. Declaration and Filing Phase:

- Issue Form BEN-4 notices to all potential SBOs and non-individual members.

- Upon receipt of Form BEN-1 declarations, file Form BEN-2 with the Registrar within 30 days

- Ensure that Form BEN-2 filings are certified by qualified professionals (CA/CS/CMA)

- Maintain comprehensive records for audit and regulatory purposes.

11.4. Record Maintenance Phase:

- Prepare and maintain Form BEN-3 (Register of Beneficial Owners) with accurate and updated information.

- File updates whenever changes occur in beneficial ownership, including changes in shareholding, control mechanisms, or SBO identity.

- Ensure the register is preserved and available for inspection.

11.5. Ongoing Monitoring:

- Implement systems to track shareholding changes and control arrangements.

- Monitor board composition and director appointment arrangements.

- Review and update SBO records annually or whenever material changes occur.

- Maintain communication with SBOs regarding any changes affecting their status.

12. WAY FORWARD:

SBO identification in India is currently hindered more by interpretational gaps than by the bare text of section 90 and the SBO Rules. Stakeholders therefore need from MCA/ROC targeted clarifications on specific grey areas rather than fresh obligations.

Below are the key points on which a formal guidance or FAQs from the regulator would help substantially reduce disputes and compliance risk in SBO identification:

- Individuals who do not meet the thresholds under the provisions should not be treated as SBOs. For instance – Senior management or directors of upstream non-individual members should not be automatically presumed to be SBOs unless they meet the criteria. There should be a formal guidance published which clearly states the circumstances under which an individual should, or should not, be treated as an SBO. Clarify the relationship between section 90(4A) “necessary steps” and section 90(5) “reasonable cause to believe” so companies know whether they must proactively investigate all non individual members or only where there are triggers suggesting a possible SBO. Define what constitutes sufficient “necessary steps” by a company under section 90(4A): e.g., minimum public domain checks, reliance on client KYC, use of group structure charts, and the number and form of follow up notices (BEN 4) before the company can conclude that no SBO exists or that information is not readily obtainable.

- Confirm whether the SBO regime is strictly “twin test” (ownership threshold and control/significant influence) or whether any “control based” test (e.g., financial control, reporting channel, global group leadership) can be read in by ROCs as seen in recent orders discussed above.

- Clarify the level of verification expected on information received in BEN 1: whether the company can rely on declarations in the absence of red flags , or must independently verify upstream ownership each time, and how far up the chain it must reasonably go.

- Publish standardised interpretative guidance (or illustrative case studies) reflecting the tests used by ROCs in recent enforcement orders, with explicit confirmation of which tests are legally endorsed and which were fact specific, to avoid companies having to guess ROC thinking from penalty orders.

Last but not the least, an online helpdesk to give interpretative clarification such as SEBI (Informal Guidance) Scheme 2003 which will be specific to the facts and will help companies address their issues.

These focused clarifications, preferably through detailed MCA FAQs or a circular with examples, would allow companies and professionals to operationalise SBO identification with clear audit trails and substantially fewer interpretational hurdles will definitely go a long way to help companies avoid penalties.

SUMMARY

Significant Beneficial Ownership (SBO) represents a sophisticated regulatory framework designed to pierce(lift) corporate veils and identify the natural persons ultimately controlling or benefiting from Indian companies. The dual-test framework, combining quantitative thresholds (10% shareholding, voting rights, and dividend participation) with qualitative assessments (control and significant influence) ensures comprehensive coverage of diverse ownership and control structures. The regime’s extra-territorial application to foreign residents and structures reflects India’s alignment with international beneficial ownership standards and FATF recommendations.

The identification process, centered on objective tests of shareholding and voting rights alongside subjective tests of control, captures both transparent and hidden beneficial interests. Indirect holding mechanisms through corporate entities, HUFs, partnerships, trusts, and the “acting together” principle address complex corporate structures that might otherwise obscure true beneficial ownership. The declaration and filing requirements, implemented through Forms BEN-1, BEN-2, BEN-3, and BEN-4, establish a transparent record of beneficial ownership accessible to regulatory authorities and company members.

Recent regulatory developments, including the Samsung Display and LinkedIn orders, demonstrate regulatory commitment to rigorous enforcement of SBO requirements, particularly in corporate groups with multi-layered structures and foreign investors. The substantial penalties prescribed for non-compliance, ranging up to ₹50,000 plus ongoing daily penalties for individuals, ₹100,000 plus daily penalties for companies, and the severe consequences of NCLT orders imposing share restrictions, create powerful incentives for compliance.

For Chartered Accountants and compliance professionals, expertise in SBO identification and compliance has become essential as companies face increasing regulatory scrutiny. Systematic implementation of an SBO compliance frameworks, maintaining detailed documentation, and ongoing monitoring of beneficial ownership changes are critical elements of effective corporate governance and regulatory compliance. Given the evolving nature of regulatory interpretation and the expanding scope of beneficial ownership obligations, practitioners must maintain current knowledge of regulatory updates, case law developments, and amendments to the SBO framework to serve their clients effectively and ensure sustained compliance with this increasingly important statutory obligation.