1. This article is a part of the series of articles on income-tax and FEMA issues faced by NRIs and deals with issues faced by individuals when they change their residential status. A resident who leaves India and turns non-resident is termed as a “Migrating Resident”; while a non-resident of India, who comes to India and becomes a resident of India is termed as a “Returning NRI” in this article.

2. Both Migrating Residents and Returning NRIs have to consider implications under income-tax and FEMA before taking any decision for change of residence. We have come across several instances where such a person has not taken due care before change of residence leading to unnecessary and avoidable legal issues. After the advent of the Black Money Act1, there are instances where corrective action is quite difficult under law. Further, resolution of violations under FEMA can be difficult or costly to undertake.

1. Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015

3. Key to the above concern is the fact that residential status definitions under the Income-tax Act (ITA) and FEMA are separate and different. While under ITA, the definition is largely based on number of days stay of the individual in India; under FEMA, it is based on the purpose for which the person has come to, or left India, as the case may be. An important objective in advising persons who are migrating from India or returning to India, thus, is to determine the date on which the change in residence has been effected and purpose thereof. Any discrepancy in this can lead to assumption of incorrect residential status which can have adverse implications, some of which are as under:

a. Concealment of foreign income which should have been submitted to tax as well as non-disclosure of foreign incomes and assets, which can have severe implications under the Black Money Act;

b. Incorrect claim of benefits under the Double Tax Avoidance Agreements (DTAAs);

c. Holding assets or executing transactions which are in violation of FEMA.

4. The provisions of residential status under the ITA, the DTAA and under FEMA are dealt in detail in th preceding articles of this series — in the December 2023 and January and March 2024 editions, respectively, of The Bombay Chartered Accountant Journal (the Journal) — and hence, not repeated here. Readers will benefit by referring to those articles for issues covered therein. This article deals with income-tax and FEMA issues specifically for Migrating Residents and Returning NRIs2 and is divided into three parts as follows:

| Sr. No. |

Topic |

|

Part-I |

| A. |

Migrating Residents |

| A.1 |

Income-tax issues of Migrating Residents |

| A.2 |

FEMA issues of Migrating Residents |

| A.3 |

Change in Citizenship |

|

|

|

Part-II |

| B. |

Returning NRIs |

| B.1 |

Income-tax issues of Returning NRIs |

| B.2 |

FEMA issues of Returning NRIs |

|

|

| C. |

Other relevant issues common to change of residential status |

2. There is an overlap of several sections under different topics. To prevent repetition and focus on the relevant issues, the sections are not repeated completely. Only the applicable provisions or part thereof, which are relevant to the topic, are referred here.

Issues related to Returning NRIs and other relevant issues common to change of residential status will be covered in Part II of this Article in the upcoming issue of the Journal.

A. Migrating Residents

India has the world’s largest overseas diaspora. In fact, every year, 25 lakh Indians migrate abroad.3 While Indians shift and settle down abroad, it seldom happens that they eliminate their financial ties with India completely. The common reason being that either they continue to own assets or continue their businesses in India, or their relatives stay in India with whom they enter into transactions. Hence, Migrating Residents generally have a continuing link with India even after they have left India. This can create issues under income-tax and FEMA, which are analysed in detail below.

3. https://www.moneycontrol.com/news/immigration/immigration-where-are-indians-moving-why-are-hnis-leaving-india-12011811.html

A.1 Income-tax issues relevant for Migrating Residents:

1. Continuing Residential status under ITA: An issue that Migrating Residents need to keep in mind in particular is their residential status in the year of migration. Clause (a) of Explanation 1 to Section 6(1)(c) of the ITA provides a relief from the basic “60 + 365 days test”4. The relief is available only under two specific circumstances, i.e., a citizen who is leaving India during the relevant previous year for the purposes of employment abroad or as a crew member on an Indian ship. If a person does not fall under either of these circumstances, the “60 + 365 days test” test applies.

4 “60 + 365 days test” means that the individual has stayed in India for 60 days or more during the relevant previous year and for 365 days or more during the four preceding years.

Hence, in such cases, if a person who was normally residing in India, stays in India for 60 days or more during the year of his or her departure, he or she will meet the “60 + 365 days test” and consequently, be a resident for the whole previous year under ITA and will be classified as ROR. In such cases, following implications should be noted:

1.1 As a resident, scope of total income under Section 5 of the ITA includes all incomes accruing or arising within or outside India. Hence, foreign incomes would be prima facie taxable, subject to relief under the relevant DTAA. However, in the year of migration, even treaty benefits may not be available as the Migrating Resident may not be considered as a resident of the other country. Further, the exposure is not just regarding tax, interest and penalty under the Income-tax Act on concealment of income, but also the penal provisions under the Black Money Act for non-disclosure of foreign incomes and assets.

1.2 The issue gets compounded for a Migrating Resident who would otherwise not need to file a tax return but is now required to file a tax return as they would generally have a foreign bank account abroad. A common example is of students who are leaving India. Fourth proviso to Section 139(1) provides that those persons who are resident and ordinarily resident of India and hold or are beneficiary of any foreign asset are required to file their tax return in India even if they are not required to file a tax return otherwise. The same issue can come up for senior citizens or spouses who generally are not filing tax returns, but now need to do so in the year they are moving abroad. It should be noted that this requirement has no relief even if such person is termed as a non-resident for the purposes of the treaty under the relevant DTAA. Such an error can lead to harsh penalties under the Black Money Act for non-disclosure of foreign incomes and assets.

Hence, persons migrating abroad should be careful about their residential status in the year of migration.

1.3 Deemed Resident: Another instance where a Migrating Resident may still be considered as a resident under the ITA is due to the application of Section 6 (1A) of the ITA. This sub-section provides for an individual to be deemed as a resident of India if such individual, being a citizen of India, has total income other than income from foreign sources exceeding ₹15 lakhs during the previous year and is not liable to tax in any other country or territory by reason of domicile or residence or any other criteria of similar nature. While such deemed residents are considered as Resident but Not Ordinarily Resident as per Section 6(6)(d) of the ITA, their foreign incomes derived from a profession setup in India, or a business controlled from India are covered within the scope of income liable to tax in India. Readers can refer to the December 2023 edition of the Journal for an exposition on this provision.

1.4 Recording the change in status: On a person turning non-resident, his or her status should be correctly selected in the tax returns filed starting from the relevant assessment year of change in residence. It should be noted that the change in status recorded in the tax return does not automatically update the person’s status on the income-tax portal. Hence, such status should be changed on the income-tax portal also. Further, as of now, there seems to be no linking between the status updated in the tax return filed or on the income-tax portal with that recorded as per the local ward in the income-tax department. Hence, one should always ensure that such change is recorded in the local ward and the PAN is shifted to a ward which deals with non-residents. This will ensure that the status has been recorded in all manners with the tax department. This can be quite useful when the department issues notices to such persons.

2. Impact on change of residential status under ITA:

On change of residence, following are the important changes to keep in mind as far as ITA is concerned:

| Particulars |

ROR |

NOR |

NR |

| Scope of Total Income5 |

Global incomes taxable |

Indian-sourced incomes are taxable. Foreign-sourced income are taxable only if derived from a business controlled in India or profession set up in India.

Incomes being received for the first time in India are also taxable. |

Only Indian-sourced incomes taxable.

Foreign-sourced incomes are not taxable at all.

Incomes being received for the first time in India are also taxable. |

| Set-off of capital gains, dividend, etc., against unexhausted basic exemption limit |

Allowed6 |

Not allowed |

| Dividend |

Taxed at the applicable slab rate. |

Taxed @ 20%7 plus applicable surcharge & cess. (No set-off against unexhausted basic exemption, as stated above. No benefit of lower slab rate since special rate is mentioned.) |

| LTCG on unlisted securities and shares of |

20% with indexation8 |

10% without the benefit of indexation and forex fluctuation9 |

| a company, not being a company in which public are substantially interested |

|

|

| Withholding tax under ITA where the person is recipient of income |

Generally, at lower rates |

Generally, at a higher rate unless treaty relief availed |

| Access to Indian DTAAs |

Available as Resident of India under the DTAA |

Available if he is a resident of such host country as per the DTAA |

| FCNR Interest10 |

Taxable |

Not taxable |

| NRE Interest11 |

Exempt if the person is non-resident under FEMA |

| Benefits provided to senior citizens — higher basic exemption limit, non-applicability of advance tax in certain situations, higher deduction for medical premium u/s. 80D, deduction u/s. 80TTB, etc. |

Available |

Not available |

5. Section 5 of ITA.

6. Proviso to Section 112(1)(a) and

Proviso to Section 112A (2) of ITA.

7. Section 115A(1)(A)

8. Section 112(1)(a)(ii)

9. Section 112(1)(c)(iii)

10. Section 10(15)(iv)(fa)

11. Section 10(4)(ii)

3. Transfer Pricing: Transfer Pricing triggers in case of a transaction which can give rise to income (or imputed income) between associated enterprises (parties related to each other as per Section 92 of the Income-tax Act), of which at least one party is a non-resident. All such transactions must be on an arm’s length basis. The implications under Transfer Pricing on the shift of a person from India can lead to unnecessary complications. However, in some cases, such an implication may be unavoidable. Thus, the incomes earned by a Migrating Resident from his related enterprises in India and other International transactions with such enterprises would be subject to Transfer Pricing. There is no threshold on application of Transfer Pricing provisions.

Having considered the issues under the ITA, a Migrating Resident would need to study the impact of the DTAA, too, especially with regard to reliefs available. A detailed study of residential status as per the DTAA has been dealt with in the January 2024 issue of the Journal. Here, we focus on the issues a Migrating Resident needs to be concerned about:

4. Treaty relief:

4.1 A person can access DTAA if he is a resident of at least one of the Contracting States. To consider a person as resident of a Contracting State, DTAAs generally refer to the residential status of the person under domestic tax laws of the respective country. While there are different permutations possible, one important point to note is that while migrating abroad, there can be an overlapping period wherein the person is a resident of India as well as the foreign country during the same period. This leads to dual residency, for which tie-breaker tests are prescribed under Article 4(2) of the DTAA. There could also be a possibility of the concept of split residency under DTAA being applicable. Accordingly, the provisions of the DTAA can be applied. These provisions have been explained in detail in the second article of this series contained in the Journal’s January edition.

4.2 A dual resident status under the treaty can lead to the person being able to claim the status of a non-resident of India as per the relevant treaty even though they are a resident as far as the ITA is concerned. While this would provide them benefits under the treaty as applicable to a non-resident of India, it would not change their status under the ITA. Such persons would still need to file their tax return as a resident of India, and they would be treated as a non-resident only as far as application of the benefits of treaty provisions is concerned.

4.3 It should be noted that the benefit of treaty provisions as a non-resident is not automatic and is subject to conditions on whether such person qualifies as a tax resident of the country of his new residence as per the definition of the respective DTAA. Further, as per Section 90(4), a tax residency certificate should be obtained from the foreign jurisdiction. At the same time, as per Section 90(5), Form 10F needs be submitted online.

4.4 Individuals who claim treaty benefits without proper substance in the country of residence risk exposure to denial of such benefits under the anti-avoidance rules of the treaty like Principal Purpose Test or those of the Act in the form of General Anti-Avoidance Rules (GAAR) where the main purpose of such change of residence was tax avoidance.

A.2 FEMA issues of Migrating Residents:

5. Residential status: The concept of residential status under FEMA has been dealt with in the March 2024 edition of the Journal. FEMA uses the terms “person resident in India”12 and “person resident outside India”13. For simplicity, these terms are referred to as “resident” and “non-resident” in this article.

12 As defined in Section 2(v) of FEMA

13 As defined in Section 2(w) of FEMA

It is pertinent to note from the said article that only a claim that the person has left India — for or on employment, or for carrying on business or vocation, or under circumstances indicating his intention to stay outside India for an uncertain period — is not sufficient to be considered as a non-resident under FEMA. The facts and circumstances surrounding the claim are more important and should be backed up by documentation as well. For instance, leaving India for the purpose of business should be based on a type of visa which allows business activities and to support the purpose. Similarly, a person claiming to be leaving India for employment abroad should be backed up not only by an employment visa but also a valid employment contract; actual monthly salary payments (instead of just accounting entries); salary commensurate to the knowledge and experience of the person; compliance with labour and other applicable employment laws; etc. In essence, the intent and purpose should be backed by facts substantiated by documents which prove the bona fides of such intent.

6. Scope of FEMA: Once a person becomes non-resident under FEMA, such person’s foreign assets and foreign transactions are outside FEMA purview except in a few circumstances. However, such person’s assets and transactions in India would now come under the purview of FEMA. This can create issues in certain cases.

A common example of this is loans and advances between a Migrating Resident and his family members, companies, etc. On turning non-resident, the person generally does not realise that such fresh transactions can now be undertaken only as allowed under FEMA. A simple loan transaction can be a cause of unintended violations under FEMA — resolution for which is

generally not easy.

7. Existing Indian assets of migrating persons:

7.1 For a Migrating Resident, transacting with his or her own Indian assets after turning non-resident results in capital account transactions and, thus, can be undertaken only as permitted under FEMA. Section 6(5) of FEMA comes to the rescue in such a case. It allows a non-resident to continue holding Indian currency, Indian security or any immovable property situated in India if such currency, security or property was acquired, held or owned by such person when he or she was a

resident of India. In essence, Section 6(5) of FEMA allows non-residents to continue holding their Indian

assets which they acquired or owned when they were residents.

7.2 This also includes such assets or investments which cannot be otherwise owned or made by a non-resident. For instance, non-residents are not allowed to invest in an Indian company which is engaged in real estate trading. However, if a resident individual has invested in such a company and he later becomes a non-resident, he can continue holding such shares even after turning non-resident.

7.3 However, it should be noted that Section 6(5) permits only holding the existing assets. Any additional investment or transaction should conform with the FEMA provisions applicable to such non-residents.

Hence, if such an individual wants to make any further investment in the real estate trading company after turning a non-resident, he can do so only in compliance with FEMA. As investment by an NRI in an entity which undertakes real estate trading in India is not permitted under the NDI Rules14, such further investment would not be allowed even if the migrating person owned stake in such an entity before they turned non-resident.

14. Non-debt Instrument Rules, 2019

7.4 Further, incomes earned, or sale proceeds obtained, from such assets can be utilised only for purposes permissible to a non-resident. Thus, incomes earned by a non-resident from assets he held as a resident cannot be utilised, for instance, to invest in a real estate trading company in India. This is in contrast to Section 6(4) of FEMA which applies to Returning NRIs who are permitted to invest and utilise their incomes earned on their foreign assets covered under Section 6(4) or sale proceeds thereof without any approval from RBI even after they turn resident. This concept of Section 6(4) will be explained in detail in the second part of this article dealing with Returning NRIs.

7.5 Other assets: Section 6(5) of FEMA specifies only three assets: Indian currency, Indian security or any immovable property situated in India. A person would generally own several other assets. For instance, the person may have an interest in a partnership firm, LLP, AOPs or may own gold, jewellery, paintings, etc. There is no clarity provided in FEMA or its notifications and rules on continued holding of such other assets. However, as a practice, a person is eligible to continue holding all the Indian assets after turning non-resident which he owned or held as a resident. In fact, even the business of all entities can continue.

7.6 Repatriation of sale proceeds and incomes: On the migrating person turning non-resident, assets in India are considered to be held on a non-repatriable basis. That is, the sale proceeds obtained on transfer of such assets are not freely repatriable outside India. This is because transfer of an asset held in India by a non-resident is a capital account transaction and full remittance of sale proceeds of such assets covered under Section 6(5) is not specifically allowed.

However, separately, on turning non-resident, NRIs (including PIOs and OCI card holders) are allowed to remit up to USD 1 million per financial year from their funds lying in India15. It should be noted that such remittances can be only from one’s own funds. Remittances in excess of this limit would be only under approval route and there are low chances of the RBI providing any relief in such cases. Thus, in essence, a Migrating Resident would have limited repatriability as far as sale proceeds of their assets in India covered under Section 6(5) are concerned.

15. Regulation 4(2) of Foreign Exchange Management (Remittance of Assets) Regulations, 2016

Incomes generated from such investments, say dividend, interest, etc., can be freely repatriated from India without any limit as these are considered as they are current account transactions for which there are no limits on repatriation under FEMA for a non-resident.

7.7 Applicability of Section 6(5) of FEMA:

Section 6(5) of FEMA reads as under:

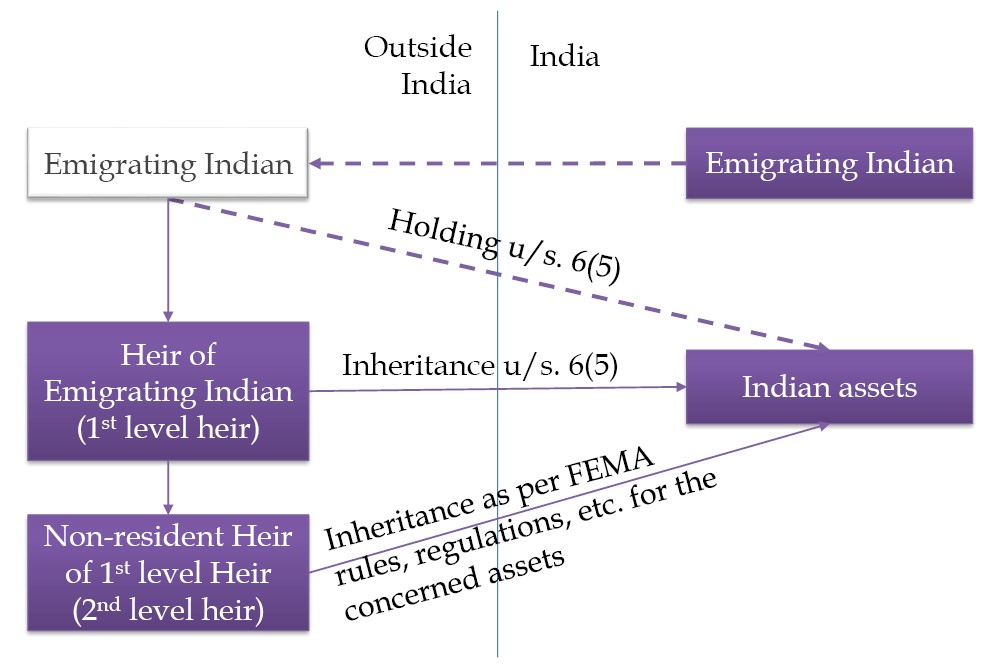

(5) A person resident outside India may hold, own, transfer or invest in Indian currency, security or any immovable property situated in India if such currency, security or property was acquired, held or owned by such person when he was resident in India or inherited from a person who was resident in India.

The first limb of Section 6(5) of FEMA allows non-residents to hold specified Indian assets which they owned or held as a resident. The second limb of Section 6(5) further allows the non-resident heir of such a migrating person also to inherit and hold such assets in India.

Thus, Section 6(5) allows both the Migrating Resident and his or her non-resident heirs to continue holding the Indian assets. It should be noted this provision covers only one level of inheritance, i.e., from the migrating person who has become non-resident to his non-resident heir. Later, if say the heir of such non-resident heir acquires such assets by way of inheritance, it is not covered under Section 6(5). The relevant notifications, rules, etc., under FEMA corresponding to the concerned assets need to be checked for the same. The permissibility for holding and inheritance under Section 6(5) can be summarised as follows:

An area of interpretation arises on a plain reading of the second limb of Section 6(5) which suggests that it covers inheritance by a non-resident heir only from a resident as the phrase reads as “a person who was resident in India”. However, the intention is to cover inheritance by a non-resident heir from another non-resident who had acquired the Indian assets when he was resident and later turned non-resident. Hence, if a non-resident acquires any asset in India by way of inheritance from a resident, the relevant notifications, rules, etc., under FEMA corresponding to the concerned assets need to be checked if they are permitted. For instance, if a non-resident is going to acquire an immovable property situated in India from a resident, it needs to be checked whether such inheritance is permitted under the NDI Rules16. Under Rule 24(c) of NDI Rules, an individual, who is non-resident, is permitted to acquire an immovable property situated in India by way of inheritance only if such person is an NRI or OCI cardholder. Hence, in this case, if the non-resident is an NRI or OCI cardholder, only then he is permitted to inherit an immovable property situated in India from a resident. This case will not be covered under Section 6(5).

16. Non-debt Instrument Rules, 2019

Apart from the general relief under Section 6(5) of FEMA, there are certain specific assets and transactions which are dealt with separately under the notifications as explained below.

7.8 Bank and Demat Accounts: Bank and demat accounts normally held by persons staying in India are Resident accounts. When a resident individual turns non-resident, he is required17 to designate all his bank and demat accounts to Non-Resident (Ordinary) account – NRO account. One must note that there is no specific procedure under FEMA for a person to claim or to even intimate to the authorities that they have turned non-resident on migrating abroad. Unlike OCI card, there is no NRI card. Further, there is no concept of a certificate under FEMA like a Tax Residency Certificate under ITA. The simplest manner this claim can be put forward is by designating their bank account as a Non-Resident (Ordinary) account (NRO) account. Thus, it is important that a Migrating Resident does not delay in designating their bank account as an NRO account. This becomes the primary account of the person for Indian transactions and investments. It should be noted that banks will ask for related documents which substantiate the change in residential status of the individual for designating the account as NRO. In fact, the redesignation of account as NRO is the most widely accepted recognition of a person as an NRI under FEMA, and therefore, it is important for the Migrating Resident to intimate his banker about the change of residential status.

17. Para 9(a) of Schedule III to FEMA Notification No. 5(R)/2016-RB. FEM (Deposit) Regulations, 2016.

Once the Migrating Resident becomes a non-resident as per FEMA, they are permitted to open different type of accounts like NRE account, FCNR account, etc., which provide permission to hold foreign currency in India, flexibility of making inward and outward remittances without limit or compliances, etc. Once a person becomes non-resident, he can take benefit of opening such accounts. (The provisions pertaining to the same will be dealt with in detail in the upcoming parts of this series of articles.)

7.9 Loans:

i. Loan taken by a Migrating Resident from bank: If a loan is taken by a resident from a bank and he later turns non-resident, the loan can be continued. This is subject to terms and conditions as specified by RBI, which have not been notified. However, in practice, banks are allowing non-residents to continue the loans taken by them when they were residents.

ii. Loan between resident individuals: Where a loan is given by one resident individual to another, FEMA would not apply. If the lender becomes a non-resident later, repayment of the same can be done by the resident borrower to the NRO account of the lender. There is no rule or provision in FEMA for a situation where the borrower becomes a non-resident. However, in such case, the borrower can repay the loan from his Indian or foreign funds. It should not be an issue.

7.10 Immovable properties: NRIs and OCIs are permitted to acquire immovable property in India, except agricultural land, farmhouse or plantation property18. However, what if a person owned such property as a resident and later turned non-resident. Section 6(5) covers any type of immovable property which was acquired or held as a resident. Hence, one can continue holding any immovable property after turning non-resident including agricultural land.

18. Rule 24(a) of FEM (Non-debt Instruments) Rules, 2019

7.11 Insurance: Almost every Migrating Resident would have existing insurance contracts covering both life and medical risks. While there is no specific clarification on continuance of such policies, a Migrating Resident can take recourse to the Master Direction on Insurance19 which provides that for life insurance policies denominated in rupees issued to non-residents, funds held in NRO accounts can also be accepted towards payment of premiums apart from their other accounts. Settlement of claims on such life insurance policies will happen in foreign currency in proportion to the amount of premiums paid in foreign currency in relation to the total amount of premiums paid. Balance would only be in rupees by credit to the NRO account of the beneficiary. This would also apply in cases of death claims being settled in favour of residents outside India who are assignees or nominees on such policies.

19. FED Master Direction No. 9/ 2015-16 - last updated on 7th December, 2021

7.12 PPF account: Non-residents are not permitted to open PPF accounts. However, residents who hold PPF account and turn NRIs (and not OCIs) are permitted to deposit funds in the same and continue the account till its maturity on a non-repatriation basis.20 While extension is not permitted, as a practice, the account is permitted to be held after maturity but additional contributions are not allowed.

20. Notification GSR 585(E) issued by Ministry of Finance dated 25th July 2003.

7.13 Privately held investments: Migrating person who holds investments in entities like unlisted companies, LLPs, partnership firms, etc. should intimate such entities about change in residential status.

8. Remittance facilities for non-residents: The remittance facilities for non-residents are generally higher and more flexible than for residents. These will be dealt with in detail in the upcoming editions of the Journal. However, an important point pertaining to the year of migration is highlighted below.

The bank, broker, etc., should be intimated about the change in residential status. Once the resident accounts are designated as NRO, the remittance facilities available for non-residents can be utilised.

One must note that, conservatively, the remittance facilities are to be considered for a full financial year and hence cannot be utilised as applicable for residents as well as non-residents in the same financial year. For instance, let’s say, a resident individual has utilised the maximum LRS limit of USD 250,000 available to him. In the same year, he migrates abroad and wishes to remit USD 1 million as a non-resident under FEMA. However, since the person had already remitted USD 250,000 during the year, albeit as a resident, he cannot remit another USD 1 million after turning non-resident. He can remit only up to USD 750,000 during that year. From the next financial year, the person can remit up to USD 1 million per year.

9. Foreign assets directly held by Migrating Residents:

9.1 More and more residents today own assets abroad. Generally, a resident individual could be holding overseas investment by way of Overseas Direct Investment (ODI), Overseas Portfolio Investment (OPI) or an Immovable Property (IP) abroad as per the Overseas Investment Rules, 2022. Let us consider that such an individual migrates abroad. Does FEMA apply to these foreign assets after such person becomes a non-resident? There is no express provision in the law or any clarification from RBI regarding applicability of FEMA in such cases.

9.2 The general rule is that FEMA does not apply to the foreign assets and foreign transactions of a non-resident. Hence, prima facie, where an individual turns non-resident, his foreign assets are out of FEMA purview. Thus, foreign investments and foreign immovable property obtained under the LRS route would go out of the purview of FEMA once a person turns non-resident.

9.3 However, there is a grey area for investments made under the ODI route by resident individuals. This is because investments under the LRS-ODI route stand on a footing different from other foreign assets of resident individuals. Many Resident Individuals set up companies abroad under the LRS-ODI route21, establish their overseas business and then migrate abroad. What gets missed out is to determine whether FEMA continues to apply even after they have turned non-resident.

21 Route adopted for overseas direct investment by Resident Individuals as per Rule 13 of Overseas Investment Rules, 2022 or as per erstwhile Reg. 20A of FEM (Transfer or Issue Of Any Foreign Security) Regulations, 2004.

Under LRS-ODI route, the investment and disinvestment need to be done as per pricing guidelines; all incomes earned on the investment and the sale proceeds thereof need to be repatriated to India within 90 days; reporting of every investment or disinvestment is required, etc. It is not clear whether these disinvestment norms and reporting requirements continue to apply after the person turns non-resident.

It is understood that when an intimation is provided that all the residents owning the foreign entity under the LRS-ODI route have turned non-resident, the RBI suspends the associated UIN22 but does not cancel it. This is done so that there is no trigger from the system for filing of Annual Performance Report (APR). In case the Migrating Residents decide to return to India in future and turn resident again, the suspension on the UIN would be removed and compliance requirements would restart.

22. Unique Identification Number provided for each ODI investment.

Apart from the compliance requirements, there are other rules that apply to investments under the LRS-ODI Route like pricing guidelines, repatriation of incomes and disinvestment proceeds, reporting of modifications in the investment, etc. There is no clarity on whether these rules continue to apply to such overseas investments once the Migrating Resident turns non-resident. One view is that in such a case the Resident should follow the applicable ODI rules. This is because the facility provided for making investments abroad under ODI route is with the underlying purpose that incomes and gains earned on such foreign investments would be repatriated back to India as and when due. Another reason seems to be that when the investment is made under LRS-ODI, the individual has used foreign exchange reserves of India and therefore, he or she is required to give the account of use of such funds till the investment is divested and compliances are completed. The alternate view is that FEMA does not apply to a foreign asset held by a non-resident individual. Hence, no compliance with rules under FEMA is required. Both views can be considered valid. However, without any clarification under the law, one should seek clarification from the RBI and then proceed in the alternate case.

10. Overseas Direct Investment (ODI) made by Indian entities of Migrating Residents: One more common structure is where the Indian entities owned by resident individuals make ODI in foreign entities. Later, the individuals migrate abroad. Since they have turned non-residents, FEMA does not apply to such individuals. However, sometimes these non-residents also consider that their overseas entities are also free from FEMA provisions.

Hence, they enter into several transactions like borrowing funds from such foreign entity, directing such entity to undertake portfolio investments, utilise the funds lying in such entity for personal purposes of the shareholders or directors, etc. All such transactions are not permitted under the ODI guidelines. It should be noted that once an investment is made in a foreign entity under ODI route by an Indian entity, the ODI guidelines need to be followed by the foreign entity irrespective of the residential status of its ultimate beneficial owners. Such a foreign entity can only do the specified business for which it has been set up abroad. Thus, if such an entity enters into any transaction outside its business requirements, it would be considered as a violation under FEMA.

A.3. Change of citizenship — FEMA & Income-tax issues: Apart from change of residence, a few Migrating Residents also end up changing their citizenship. Such people obtain citizenship of foreign countries for varied reasons: to avail better opportunities in such countries; to avoid regular visa issues, for ease of entry in other countries, etc. Since India does not allow dual citizenship, such people need to revoke their Indian citizenship. Between 2018 to June 2023, close to 8,40,000 people renounced their Indian citizenship.23 Further, India has allowed such individuals access to a special class of benefits as an Overseas Citizen of India. Several benefits have been conferred to OCI cardholders under FEMA and are treated almost at par with NRIs (who are Indian citizens but non-resident of India). The concepts of PIO and OCI have been explained in detail in the March edition of the Journal. Further, Indian residents and those coming on a visit to India, who have obtained foreign citizenship, also need to keep certain issues in mind. These issues are highlighted below.

23. Answer by Ministry of External Affairs in Rajya Sabha to Question No. 2466 dated 10th August, 2023

11. OCI vs PIO card: It should be noted that the PIO scheme has been replaced with OCI scheme. Under the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019, Foreign Exchange Management (Debt Instruments) Regulations, 2019 and Foreign Exchange Management (Borrowing & Lending) Regulations, 2018, only OCIs are recognised and not PIOs. Hence, this creates issues for borrowing and lending, investments in India, etc., if the individual, though of Indian origin, has not obtained an OCI card. An important point that may not miss the attention of PIOs is that inheritance of immovable properties and Indian securities is also permitted under these notifications only to OCI Cardholders and not PIOs. Most PIOs should be eligible for OCI status and hence, they should obtain OCI cards if they have, or will have, financial links with India.

12. Applicability of Section 6(1A) of the ITA: Section 6(1A) of the Income-tax Act which deems persons as Not Ordinarily Residents under certain circumstances applies only to Indian citizens. Hence, it does not apply to those who are not Indian citizens.

13. Leaving for the purpose of employment abroad: The benefit of leaving for employment outside India provided under Expl. 1(a) of Section 6(1)(c) is available only to Indian citizens. Hence, a person who is not an Indian citizen, cannot take this benefit.

14. Donations: Indian charitable trusts are not allowed to accept donations from foreign citizens unless they have obtained approval under the Foreign Contribution Regulation Act (FCRA). This prohibition is irrespective of whether the person is a PIO or an OCI. While it is a violation for the trust to accept the donation, even the donor should keep this in mind to not be a party to any contravention. At the same time, the FCRA prohibition does not apply to a non-resident who is a citizen of India. Hence, NRIs can continue to donate to Indian charitable trusts.

15. Citizenship-based taxation: In certain countries like the USA, the domestic tax laws have citizenship-based taxation whereby its citizens are taxed on their global incomes, irrespective of where they stay during the year. Even green card holders are taxed in a similar manner in the USA. Such persons when they return to India become dual residents on account of their physical stay in India and their foreign citizenship. Hence, such persons will be liable to tax on their global incomes both in India and the foreign country. Several issues of Double Tax and foreign tax credit arise in such cases and hence, proper planning is required.

16. Relief of disclosure of foreign assets: There is a limited and conditional relief from reporting of foreign assets under Schedule FA of the income-tax return forms for foreign citizens who have become tax residents while they are in India on a business, employment or student visa.

The above analysis intends to highlight the various issues that a Migrating Resident should be aware of. They should not be considered as a comprehensive list of issues that apply to a Migrating Resident. Issues relevant to “Returning NRIs” and other relevant but common issues of concern related to change of residence including inheritance tax, anti-avoidance rules under ITA, succession planning, documentation and record-keeping, etc., will be dealt with in the forthcoming issue of the Journal as Part II of this article.

The Human Resources Committee of BCAS organised a workshop (spread over four Saturdays), under the auspices of Amita Memorial Trust, where the Trainer, Mr. Shyam Lata dealt with various aspects of enhancing public speaking, communication and interpersonal skills. These four sessions helped the participants overcome limiting inhibitions. He guided them to develop a compelling desire, not only to express one’s ideas but to do so with conviction and assertion. 27 participants attended the workshop. They immensely benefited from the training.

The Human Resources Committee of BCAS organised a workshop (spread over four Saturdays), under the auspices of Amita Memorial Trust, where the Trainer, Mr. Shyam Lata dealt with various aspects of enhancing public speaking, communication and interpersonal skills. These four sessions helped the participants overcome limiting inhibitions. He guided them to develop a compelling desire, not only to express one’s ideas but to do so with conviction and assertion. 27 participants attended the workshop. They immensely benefited from the training.