By V. Shankar

Chartered Accountant

On 12th March, 2020 BCAS made an announcement

deferring my talk scheduled a week hence. The previous

day, WHO had labelled the novel coronavirus disease

or Covid-19 as a pandemic. As a consequence, several

precautions snowballed into locking down half the world’s

population as the deadly virus quickly infected over four

million people in 210 countries and claimed tens of

thousands of lives. Our Prime Minister asked for 22nd

March to be observed as Janata Bandh following which

we are into Lockdown 3.0 (and now 4.0 till 31st May,

2020). Some have termed this outbreak as a Black Swan

event and the biggest challenge humanity has faced

since World War II, seriously impacting lives, earnings,

economies and businesses with a whopping toll on the

markets. We still have to see a flattening of the curve

and estimates are that this will trigger a global recession

for an extended period. The trillion-dollar question…

who could have anticipated this and, more importantly,

prepared for it?

Over the last few decades we have been witness to

quite some events of tremendous gravity such as Ebola,

SARS, Bird Flu, the 2008 meltdown, the 2011 Earthquake

and Tsunami, Brexit… With these abnormal occurrences

occurring with discomforting regularity, is this the new

normal?

But what have all these got to do with internal controls (IC)?

Sound internal controls which encompass identifying and

managing risks both internal and external, are a sine qua

non for running a sustainable business. Conventionally

though, internal controls were more of the order of internal

checks and internal audit (IA). Segregation of duties,

maker-checker procedures, vouching transactions,

physical verification of cash, stocks and so on received

a lot of prominence. And internal audit was seen as a

routine albeit necessary activity, coasting alongside the

main operations in business. Within corporations, too, this

function was never the sought-after role for accounting

and finance professionals. Not so any longer. The everchanging

world in which things are turning more complex

by the day, is only making this entire process difficult and

tricky as we reflect on the Covid-19 pandemic.

INTERNAL CONTROLS

Controls function to keep things on course and internal

controls in any business or enterprise provide the

assurance that there would be no rude surprises. The

Committee of Sponsoring Organisations1 (COSO) has

defined IC as ‘a process, effected by an entity’s board of

directors, management and other personnel, designed to

provide reasonable assurance regarding the achievement

of objectives relating to operations, reporting and

compliance’. As per SIA 120 issued by the Institute of

Chartered Accountants of India2, ICs are essentially risk

mitigation steps taken to strengthen the organisation’s

systems and processes, as well as help to prevent and

detect errors and irregularities. In SA 3153 it is defined

as ‘the process designed, implemented and maintained

by those charged with governance, management and

other personnel to provide reasonable assurance about

the achievement of an entity’s objectives with regard

to reliability of financial reporting, effectiveness and

efficiency of operations, safeguarding of assets and

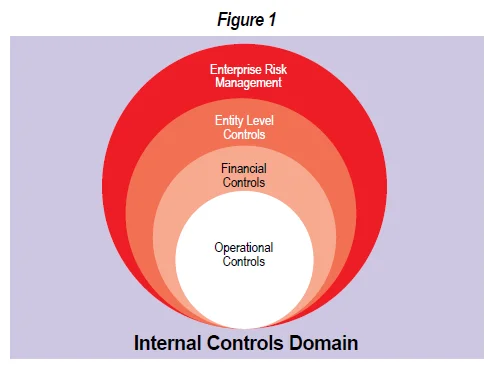

compliance with applicable laws and regulations’. IC

therefore encompasses entity level, financial as well as

operational controls (Figure 1).

1. COSO Committee of Sponsoring Organisations of the Treadway Commission:

Internal Control – Integrated Framework, May, 2013

2 Standard on Internal Audit (SIA) 120 issued by the Institute of Chartered

Accountants of India

3 Standard on Auditing (SA) 315 ‘Identifying and Assessing the Risks of Material

Misstatement Through Understanding the Entity and its Environment’, issued

by ICAI effective 1st April, 2008

A number of regulatory requirements are in place in the

realm of IC. The Companies Act, 20134 requires the

statutory auditor to report on ‘whether the company has

adequate internal financial controls system in place and

the operating effectiveness of such controls’. It requires

the Board to develop and implement a risk management

policy and identify risks that may threaten the existence

of the company. It imposes overall responsibility on

the Board of Directors with regard to Internal Financial

Controls. The Directors’ Responsibility Statement has to

state that ‘the Directors, in the case of a listed company,

had laid down internal financial controls to be followed by

the company and that such internal financial controls are

adequate and were operating effectively.’ And they have

also devised a proper system to ensure compliance with

the applicable laws and that such systems are operating

effectively. SEBI5 Regulations stipulate the preparation of

a compliance report of all laws applicable to a company

and the review of the same by the Board of Directors

periodically, as well as to take steps (by the company) to

rectify instances of non-compliance and to send reports

on compliance to the stock exchanges quarterly.

Furthermore, listed companies have additional

responsibilities on Internal Controls for Financial Reporting.

A Compliance Certificate is mandated to be signed by the

CEO and CFO to indicate that ‘they accept responsibility for

establishing and maintaining internal controls for financial

reporting and that they have evaluated the effectiveness of

the internal control systems of the listed entity pertaining to

financial reporting and they have disclosed to the auditors

and the audit committee, deficiencies in the design or

operation of such internal controls, if any, of which they are

aware and the steps they have taken or propose to take

to rectify these deficiencies’. The Institute of Chartered

Accountants of India has formulated Standards on Internal

Audit which are a set of minimum requirements that need

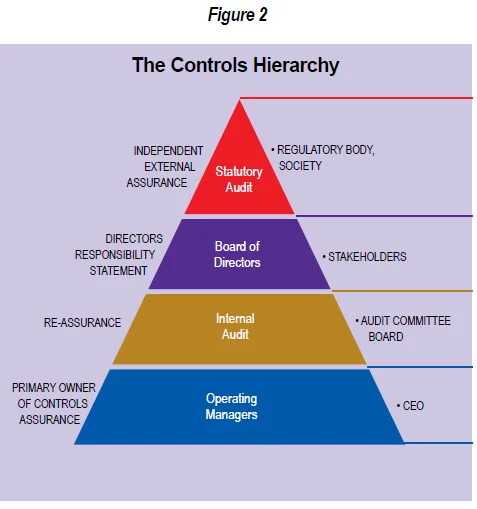

to be complied with. Hence, the overall responsibility

for designing, assessing adequacy and maintaining the

operating effectiveness of Internal Financial Controls rests

with the Board and the management (Figure 2).

THE CONTROL S HIERARCHY

Internal Controls is a vast topic in its own right. What we

will examine in this article are the following aspects:

(i) IC in action,

(ii) M anaging Risks, and

(iii) E xcellence in Business

4 The Companies Act, 2013: Sections 134, 143, 149

5 Securities and Exchange Board of India (SEBI) (Listing Obligations and Disclosure

Requirements) Regulations, 2015

Given the enlightened readers’ expert knowledge on the

above, I will dwell on anecdotes from my experience having

been on both sides of the table (auditor as well as auditee)

which could provide perspectives for due consideration.

Internal Controls in action

First, some ground realities:

* IC is commonly perceived as a specialist domain of

auditors whereas fundamentally it is the lookout of every

person in the workforce. Every manager must realise that

s/he has the core responsibility of running operations

consciously abiding by the control parameters. As the

primary owner, every person in charge must provide

assurance that their work domain is under control through

a control self-assessment mechanism;

* IA is perceived as a statutory duty and often deprived

of the credit it deserves. The irony is that this function is

not appreciated when all is well and the first issue to be

frowned upon when something goes amiss!

* O perations get priority and IA, instead of being seen

as a guide and ally to business, is perceived to be an

adversary.

In well-run enterprises there is realisation and

understanding of the importance of IC in running and

growing a sustainable business. Here are some good

practices I have experienced which build and nurture a

healthy control culture in the enterprise.

(i) In Hindustan Unilever (HLL then) there was an

unwritten practice that accountants had to go through a stint in IA. Speaking for myself, I can candidly state that my

appreciation of enterprise-wide business processes grew

during my tenure in Unilever Corporate Audit. I bagged

my first business role to run the Seeds Business in HLL

on the strength of the exposure to various businesses and

functions while in IA. A stint in IA is invaluable in opening

up the mind to the various facets of business;

(ii) U nilever Corporate Audit always reported to the

Board of Unilever and this chain of command percolated

down. In India, we were a resource for the region. IA,

therefore, had the desired independence. Not only did it

give us working exposure in several geographies, we often

worked in teams with members from different countries.

Apart from learning best practices from different parts of

the world, I found the attitude to audit and culture quite

varied. When we came up with issues, in many countries

it would be accepted and debated purely at a professional

level, whereas in some it would be taken as a personal

assault by the auditee! Managing such conflicts by open

communication and objective fieldwork / analytics is a

valuable experience in honing leadership skills;

(iii) IA used to take on deputation team members from

other functions such as Manufacturing, Sales, QA, etc.

This provided a two-pronged advantage. As a primary

owner of controls, such functional members became the

spokespersons for demystifying IA within the organisation.

Equally, these members brought in their domain expertise

to raise the quality within IA, in particular on operational

controls. Involving and engaging team members in

different ways helps in building the control culture;

(iv) A udit always began with a meeting with the Chairman

/ MD / Business Head as the case may be. Not only

did this give a perspective to the business but it also

highlighted for the IA team the priorities and areas where

the business looked for support from IA. This would also

demonstrate the senior leadership’s commitment to IA.

Soon thereafter, we would convert this into a Letter of

Audit Scope outlining the focus areas of the particular

audit. In a sense, it was like giving out the question paper

before the exam! Open communication with the auditee

and a constructive attitude is the core of a productive

outcome.

Managing Risks

At the core of Board functioning in a company is the task

of managing risks. With change and uncertainty being

the order of the day, regulations require listed companies

to have a separate Risk Management Committee at the Board level which is often chaired by an Independent

Director. While identifying and managing financial and

operational risks can be delegated to the management,

the Board focuses on strategic or environmental risks.

A major risk which we find emerging is that of disruptions.

While the other risks which are identified or anticipated can

be reasonably managed, businesses today feel challenged

due to disruptions coming from various quarters. These

could be in the form of Regulatory disruption (e.g. FDI in

multi-brand retail), Market disruption (e- and m-commerce

congruence), Competitive disruption (Jio in the telecom

space), Change in consumer buying behaviour (leasing

or renting vs. buying) or Disruptors in the service space

(Airbnb or Uber). What businesses need to be planning

for is not just combating competition from traditional

competitors, but that coming from the outside as well.

The purport of these external risks become clear, as

pointed out by the World Economic Forum6, as global risks

– an unsettled world, risks to economic stability and social

cohesion, climate threats and accelerated biodiversity

loss, consequences of digital fragmentation, health

systems under new pressures. As for Covid-19, there

were research papers published post the SARS event

warning about such an eventuality. Stretching it further,

even films such as Contagion portrayed this. It is feared

that a number of MSMEs and startups may get seriously

throttled due to this disruption. How seriously do Boards

and managements take the cue from such pointers going

forward and, more important, prepare for such disruptions

is going to be the key in sustaining businesses.

As we learn to work differently during lockdowns, there is

a growing reliance on remote working and heightened use

of technology. Webinars, video chats, video conferences,

e-platforms and Apps have become daily routines and

add another dimension to cyber security, data protection

and data privacy.

In Rallis India Limited, it had been the practice for many

years to have an off-site meeting of the Board devoted

to discussing strategy and long-term plans. It is now

imperative that companies use such fora at a Board and

senior leadership level not only to debate annual and

long-term plans, but also scenario planning simulating

various major risks. These are necessary to strengthen

IC by crafting exhaustive disaster recovery plans not

only for operations or digital disruptions, but also for force majeure events occurring in different magnitudes

across the extended supply chain both within and

externally.

6 World Economic Forum: The Global Risks Report, 2020

Excellence in Business

In the Tata Group, in addition to instilling the Tata Code

of Conduct, all companies adopt the Tata Business

Excellence Model7 (TBEM). Based on the Malcolm

Balridge model of the USA, TBEM encourages Tata

Companies to strive for excellence in every possible

manner. Instituted by Chairman Emeritus Mr. Ratan Tata

in honour of Bharat Ratna Late J.R.D. Tata who embodied

excellence, TBEM is the glue amongst Tata Companies

to share best practices and provide a potent platform

for leadership development. Last year marked the 25th

year of its highest award called the JRD-Quality Value

Award, which was bestowed on companies that reached

a high threshold of business excellence. Rallis won the

JRD-QV Award in 2011 and I benefited hugely having

been an integral part of the TBEM process. This gave

me tremendous perspectives on managing businesses,

especially in the following areas:

(a) T BEM is a wall-to-wall model touching every aspect

of business from leadership to strategy to customer

to results. A trained team comprising members from

different backgrounds and businesses comes together

for an assessment over many man-months. While

assessment is done against a framework, this is not

in the nature of an audit. Evidence and records do not

get as much importance as interactions with people. It

is not uncommon for a team to interact with a thousand

persons connected with the company being assessed,

both workforce as well as other stakeholders. Therefore,

the smell of the company would give a perspective on

governance matters as well. Excellence assessments

is a great discipline for organisations to get an external

assurance on both governance and internal controls;

(b) U nique to TBEM is the practice of having Mentors for

every assessment. I have been privileged to be a longstanding

Mentor. The Mentor essentially assesses the

strategy of the company and also plays the crucial role of

being a bridge between the company and the assessing

team. The Mentor finally presents the assessment finding

to the Chairmen both at the company and at the Group

level. Over the years this has given me exposure to various

industries ranging from steel to battery to insurance to

coffee and retail, not to speak of connecting with scores of people within the Group and beyond. A great tool for

leadership development;

(c) T BEM uses the lens of continuous improvement

to assess businesses. Deep within lies the twin benefit

of this not only sharpening controls but also constantly

improving the effectiveness and efficiency of business

processes. The DNA of excellence in an organisation

leads every individual to keep questioning and enriching

jobs. Excellence is a journey, not a destination and a way

of doing business.

7 www.tatabex.com – About us – Tata Business Excellence Model

Bringing these together

All the three components, viz., risk management, internal

audit and business excellence acting in unison are

crucial to building and nurturing a sustainable business.

In many organisations, however, the degree of maturity

and the level of execution of each of these vary and are

rarely found to be harmoniously in motion. Embedded in

this lies the fact that each of these is driven by different

frameworks, parameters, regulations, formats, reporting systems, teams and so on. A softer aspect is that most

of this is perceived as a theoretical exercise and the

operating management having to fill in tedious forms

while running the business!

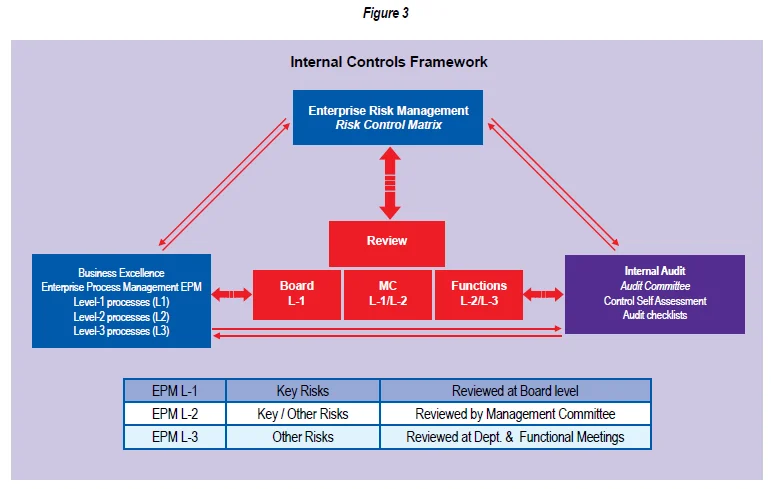

Here is an approach (Figure 3) which integrates all

of these driving similar goals and therefore avoiding

repeated exercises involving the operating teams.

The Enterprise Risk Management exercise carried out

across the organisation involving internal and external

stakeholders culminates in the identification of the

environmental, strategic, operational and financial risks

of the business. The Enterprise Process Management

model crafts all the business processes into three

levels which can be aligned and integrated with the

mitigation plans for the risks. These L1, L2 and L3

processes keep getting updated and improved annually

to drive continuous improvement as well as to enhance

controls.

The internal audit self-control checklists as well as audit

plans would be dovetailed with these mitigation plans and

processes. Such an approach will not only ensure that operations are run within the defined control framework

keeping risks within the appetite of the business, but

also strive continuously for excellence as processes

keep improving its efficiencies and effectiveness. This

integrated framework will then flow through populating the

various formats required and help the operating teams

to also address different reviews in a cohesive manner.

Above all, this brings in the desired objective of the entire

workforce viewing and putting into action the entire gamut

of the internal control framework enabling them to register

a superior performance in business.

The Late J.R.D. Tata’s quote sums this up well: ‘One

must forever strive for excellence, or even perfection, in

any task however small, and never be satisfied with the

second best.’

Driving excellence, all businesses will necessarily need

to uphold the highest standards of governance and

internal controls for long-term sustainable value creation,

committed to all stakeholders.

(This article is a sequel to Part 1 published on Page 15 in

BCAJ, March, 2020)