This article attempts to consolidate recent key commercial and regulatory developments having a bearing on Corporate Restructurings and Mergers & Acquisitions. It could help decision-makers in preparing for the expected resurgence of corporate actions as we step into ‘Mission Begin Again’.

BACKDROP

The F.Y. 2019-20 was hampered by a global structural slowdown which got further amplified with the novel Covid-19 pandemic bearing significant impact on business models and corporate actions.

From a sustenance stand-point, raising fresh capital for organic and inorganic needs is clearly the need of the hour. We are seeing the outlier transaction of Jio Platforms’ Rs. 115,693 crores aggregate fund raise1 and then we have the flurry of announcements for rights issues, NCDs, venture debts and loan top-ups. From the startups’ perspective, pricing and dilution issues are forcing them towards debt and venture debt with unique situations around collaterals and dynamic business models with cash burn.

With Unlock 1.0 and the expectation of ‘normal’ monsoon2 serving as a confidence-booster, markets and industries are moving in a green zone, at least on a month-on-month basis, including for capital markets.

| Index |

Current levels (1st June, 2020) |

% change from 1st Jan to 31st Mar |

% change from 31st Mar to 1st June |

| SENSEX |

33,303 |

– 29% |

+ 13% |

Subject to the possibility of Covid continuing to lash out again and again in waves, Q3FY21 and Q4FY21 may provide some clarity on business feasibilities, cash runways, etc. which could act as a direct feeder for potential internal and external restructurings and M&A actions and consolidation across sectors.

1 https://www.bseindia.com/xml-data/corpfiling/AttachHis/715b628f-8f44-413a-b509-2943a2dd3f22.pdf

2 http://internal.imd.gov.in/press_release/20200601_pr_827.pdf

Each corporate action, irrespective of its nature, size and scale, has its unique internal and external challenges, including:

From the preparedness point of view, the above agenda clearly needs at least two to four months of planning before actual execution of corporate action. So, the time is NOW.

With almost all the businesses exposed due to the pandemic, it is absolutely essential to take a hard look / relook at the story, rephrase it and create a platform for market participants for ease of deal-making.

On the M&A horizon, we are seeing re-negotiations of live transactions, revalidating offerings and numbers to see if strategic reasons still hold good, to re-assess deal valuations, covenants, etc. For already ‘closed’ transactions, re-negotiations are expected in the capital structure (cap tables, as they are known commonly), earn-out targets, valuation covenants, agreed business plans and covenants in the shareholder / transaction agreements. Such re-negotiations may also get extended to ESOPs and sweat equity allocations and agreed benchmarks.

For us professionals, we can add significant value on both sides of the table, especially keeping tax and regulatory requirements in mind.

RIGOROUS OPERATIONAL ASSESSMENTS COULD LEAD TO RESTRUCTURINGS AND DEALS

An assessment of costs, commitments, scenario analyses, markets and stakeholders’ concerns during the lockdown could help in identifying ‘good apples’ and ‘bad apples’.

Consolidation (mergers) and hive-offs (de-mergers or slump sale or itemised sale) can be evaluated for the following scenarios:

| Indicator |

Possible solution |

| New-age business or product |

Hive-off to attract new-age capital |

| Excess capacities, facilities and assets |

Hive-off and sale / leases, white-labelling arrangements, joint ventures |

| Unviable undertakings / companies |

Consolidation with parent to optimise on costs going forward |

| Business succession issues due to shifting of talent, labour and resources |

Merger / consolidation with other market participants

Creating group or sector-level outsourcing vehicles with independent business plan |

| High-performing businesses |

Separating from common hotchpotch and value realisation |

At times, segregation of businesses with distinct cash flows could help could lead the way forward for the company, investor interest and fund-raising. Such a raise also helps promoters to bring their contribution in the bank settlements which are generally in 20%-25% ratio of restructuring and thereby helping and working on an overall bailout plan.

The Insolvency and Bankruptcy Code, 2016 (‘IBC’) has fast-tracked the insolvency and resolution process requiring swift action on the part of management in the rescue attempt. It is often seen that viable assets / businesses are drawn into distress if not segregated in time.

By way of example, recently Gold’s Gym filed for bankruptcy protection in the US3. Interestingly, they have closed company-owned gyms; however, licensing (franchising) business is expected to keep the company a going concern. We have had many such examples in India in the past.

Global companies and investors are looking out for replacing China with India and other developing countries. In times like these, corporates which are placed well from the structure, clarity of business plan, readiness and compliance point of view could be the preferred choice for external investors and also help in faster ‘closing’ of deals.

3 https://www.goldsgym.com/restructure/

Even a simple decision of choice of a legal entity between Limited Liability Partnership vs. Private Limited Company could have significant impact on the IRR of the project merely due to the difference in applicable income tax rates.

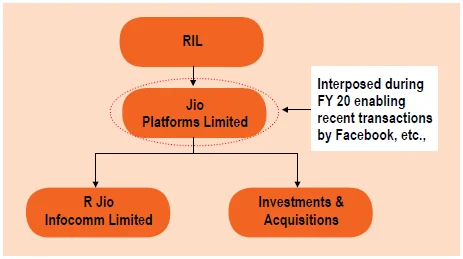

In October, 2019 RIL created a structural as well as technological platform providing flexibility in deal-making4.

Structures like these provide significant flexibility in deal-making or primary listing at a multiple level, like platform company, telecom company, investees or even any combination thereof.

The current slowdown and the ability to go back to the drawing board can certainly be leveraged to prepare for M&As, restructurings and the expected resurgence in Q3FY21 onwards. Going by experience, we often find ourselves hard-pressed for availability of sufficient time to implement the most effective structure and thereby compromising on possible savings even in time value of money terms.

From the balance sheet optics point of view, historically, companies have also used the capital reduction process u/s 66 of the Companies Act to adjust negative reserves or assets which have lost value against the capital. Companies can evaluate such strategies to right-size the balance sheet, especially absorbing the Covid impact.

IMPACT OF COVID-SPECIFIC ANNOUNCEMENTS

As announced under the Atmanirbhar Bharat initiatives and further ratified by the IBC (Amendment) Ordinance, 2020 dated 5th June, 2020:

- No application for IRP shall be filed for any default arising on or after 25th March, 2020 for a period of six months or such further period not exceeding one year from such date; and

4 https://www.ril.com/DownloadFiles/Jio%20Presentation_25Oct19.pdf

(ii) there shall be a permanent ban on filing of applications for any default which may occur during the aforesaid period.

Separately, government also intends to raise the minimum threshold to initiate fresh IBC proceedings to Rs. 1 crore.

Corporates can use this for their benefit in multiple ways, including:

(a) Design and negotiate a restructuring strategy directly with lenders and creditors;

(b) Speedy disposal of internal restructuring schemes involving merger, de-merger, capital reduction, etc. due to expected reduction in the burden of cases on NCLTs.

The Government of India has also proposed multiple schemes such as the Rs. 3 lakh crores Collateral-free Automatic Loans for Business5, including MSMEs; Rs. 20,000 crores Subordinate Debt for MSMEs; Rs. 50,000 crores equity infusion through MSME Fund of Funds. Ultimately, financing under any such scheme will be subject to the strength of the business and balance sheet. Corporates have been using mergers as a tool to demonstrate higher asset and capital base.

Other recent initiatives announced by the government giving impetus to transactions include:

(1) Direct listing of securities by Indian public companies in foreign jurisdictions;

(2) Sector-specific initiatives and reforms in agriculture, defence, space, coal, food processing, aircraft MRO, logistics, education, etc.;

(3) Private companies which list NCDs on stock exchanges need not be regarded as listed companies.

OVERSEAS LISTING OF PUBLIC COMPANIES – A NEW PARADIGM

In December, 2018 SEBI published the Expert Committee Report6 suggesting a framework for listing shares of Indian companies on overseas exchanges and vice versa.

In March, 2020 the Companies (Amendment) Bill, 2020 introduced in the Lok Sabha proposed to amend section 23 and provide for – such class of public companies may issue such class of securities for the purposes of listing on permitted stock exchanges in permissible foreign jurisdictions or such other jurisdictions, as may be prescribed.

5 https://www.eclgs.com/

6 Report of the Expert Committee for Listing of Equity Shares of companies incorporated in India on Foreign Stock Exchanges and of companies incorporated outside India on Indian Stock Exchanges, dated 4th December, 2020As of today, Indian companies can access the equity capital markets of foreign jurisdictions through the American Depository Receipts (‘ADR’) and Global Depository Receipts (‘GDR’) regimes. Indian companies can list their debt securities on foreign stock exchanges directly through the masala bonds and / or foreign currency convertible bond (‘FCCB’) / foreign currency exchangeable bonds (‘FCEB’) framework.

The proposed framework is expected to provide:

As stated in the Expert Committee Report, over the period 2013-2018, 91 companies with business operations primarily in China raised US $44 billion through initial public offerings on NYSE and NASDAQ in the USA. This indicated the potential for Indian companies, especially unicorns, to tap additional capital in the new structure.

The report also listed jurisdictions where listing could be allowed – USA, China, Japan, South Korea, UK, Hong Kong, France, Germany, Canada and Switzerland.

Key beneficiaries of this could be IT/ITES, unicorns, healthcare, infrastructure, companies having significant global exposure, companies having strong corporate governance and having third-party investors such as PE, VC investors.

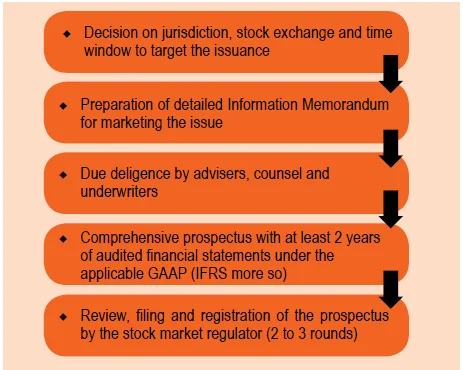

From the process point of view, some of the critical aspects of the process include:

Key nuances of overseas listings include:

- Relatively higher process and adviser costs;

- Approximately six months of overall timelines;

iii. Potential class action suits for significant drops in the prices, etc.;

- Understanding of and compliance with foreign regulations such as stock exchange regulations, regulations such as FCPA (anti-corruption regulations), FATF compliances; and

- Enhanced disclosures and continuous investor, market engagements.

Before this becomes a reality, substantial changes are expected across the spectrum from corporate law to securities law and tax laws.

OTHER RECENT REGULATORY DEVELOPMENTS

With the number of new proposals, disclosure requirements could also lead to re-assessment of group structures.

CARO 2020

Under CARO 20207, a disclosure is required whether a company is a Core Investment Company (‘CIC’) as per RBI regulations and whether the group has more than one CIC. As a fallout, if at such group level the aggregate asset of the CICs exceeds Rs. 100 crores, such CICs are required to be registered with RBI as ‘Systematically Important CICs’ (CIC-ND-SI).

Some of the legacy groups could unintentionally run into unwanted, tedious registration or compliance requirements with such new disclosures and focused assessment. It could even be reason enough to liquidate or consolidate unwanted holding / operating companies with the objective to cut costs and streamlining operations to reduce the regulatory burden.

7 Applicability extended from financial year 2019-20 to financial year 2020-21 onwards

Minority squeeze-outs

On 3rd February, 2020 sub-sections 11 and 12 were introduced in section 2308 to provide for compromise or arrangement to include takeover offers made in such manner as may be prescribed (except for listed companies where SEBI regulations are to be followed).

The MCA also notified the National Company Law (Amendment) Rules 2020 (‘NCLT Rules’) and the Companies (Compromises, Amalgamations and Arrangements) Amendment Rules, 2020 (‘Companies Rules’) to deal with the rules and procedures.

This will certainly provide an additional and specific window for companies looking to delist and provide them with a framework to eliminate the minority shareholders completely. This will help them to effectively take 100% control over operations and help in decision-making during corporate actions.

SEBI’s Press Release for Listed Companies having Stressed Assets9 and other relaxations

The timing of SEBI’s Press Release (PR No./35/2020) could not have been better. It principally deals with relaxation in the pricing of preferential issues and exemption from making an open offer for acquisitions in listed companies having ‘Stressed Assets’ (as per the eligibility criteria set out) by way of:

- Relaxation of pricing guidelines and limiting the pricing calculation based on past two weeks’ data only. Existing regulations also mandate considering 26 weeks’ price data which may not capture the Covid disruption;

- Exemption from making an open offer even if the acquisition is beyond the prescribed threshold or if the open offer is warranted due to change in control.

The above proposal comes with conditions such as non-applicability for allotment to promoters, approval of majority of the minority shareholders, disclosure and monitoring of proposed use and lock-in period of three years.

8 https://tinyurl.com/ycdc3tvs

9. https://www.sebi.gov.in/media/press-releases/jun-2020/relaxations-for-listed-companies-having-stressed-assets_46910.html

Further, SEBI also issued PR No./ 36 / 2020 temporarily relaxed pricing guidelines (up to 31st December, 2020) for all the corporates and provided an additional option to price the preferential allotments at the higher of 12-week or two-week prices with lock-in of three years.

The above decisions could help in faster resolution of stress and avert liquidation proceedings under IBC and large M&As and also provide an incentive to the promoters to provide liquidity to the companies at current prices.

Peculiar situations arising in deals

Declining valuations create opportunities to seek deals that create long-term value and total shareholder returns

In fact, the numbers of buyers could also be limited in today’s times. This could be the single most important reason for deals to return soon and chase companies that have survived the impact of Covid-19

Valuation and volatility issues around primary markets are expected to spur secondary market deals and M&As at least for the rest of F.Y. 2020.

Ex-IBC M&A activity itself has seen a lull even in F.Y. 2019. For various reasons, transactions also take too long to close. Limited partners of PE Funds have also advised the general partners and fund managers to tread with caution and focus on situations in existing portfolio companies during Covid.

Key discussions amongst the investment community are revolving around the following points:

(a) Re-negotiations are rampant;

(b) Decision-making has slowed across the globe and parties are trying to fully understand the impact of Covid-19 on businesses;

(c) M&A deal-making teams need to identify what would be the ‘new normal’;

(d) Sectors like healthcare, agri, logistics and technology would get more investments in the near future, as their inherent need has been clearer due to the Covid situation. On the other hand, discretionary spends like luxury goods, hotels, tourism, etc. might have longer downturns;

(e) The deal-making process will change to more virtual meetings, online DDs, etc., managements may not be immediately comfortable in taking such strategic decisions through virtual meetings, leading to slower deal-making processes;

(f) Companies / business models which are cash-positive will be more in demand and would attract buyers’ interest;

_____________________________________________________________

8 https://tinyurl.com/ycdc3tvs

9 https://www.sebi.gov.in/media/press-releases/jun-2020/relaxations-for-listed-companies-having-stressed-assets_46910.html

10 MINISTRY OF FINANCE (Department of Economic Affairs) NOTIFICATION, New Delhi, 22ndApril, 2020

(g) Keeping a tab on regulatory changes, compliance timelines, ability to avail of fiscal benefit has been an area of concern. For example, post-22nd April, 202010 , foreign investment from neighbouring countries will require prior government approval.

Key changes in some of the deal-making aspects are dealt with as under:

Constrained due diligences with renewed focus areas:

The security of supply chains, possible crisis-related special termination rights in important contracts and other issues that were considered low-risk in times of economic growth will become more important.

Areas requiring special focus or an expert opinion during the diligences include:

(i) Business Continuity Plan,

(ii) IT infrastructure and data security,

(iii) Insurance and Risk Mitigation policies,

(iv) Impact and scenario analysis, especially for fiscal benefits,

(v) Strength of supply chain.

One solution here could be ready with a vendor due diligence (‘VDD’) report upfront.

Pricing and instrument structuring: Pricing is generally a forward-looking exercise on the back of the latest financial performance.

Earnings / profitability-based pricing models are more relevant in case of established businesses, whereas indicators such as Daily Active Userbase (DAU), Merchandise Value or traction are used in valuing new-age businesses.

Due to changing dynamics and demand / supply chain disruptions, the problem is around sustainability of earnings of F.Y. 2020 and the estimation of earnings for F.Y. 2021.

In such situations, pricing based on a stable period which could be F.Y. 2021 or even F.Y. 2022, could be looked at whereby consideration can be back-ended or involving escrow arrangements. Such structures would also necessitate careful structuring from the income tax point of view.

Further, in case of FDI / cross-border transactions, transfer of equity instruments between an Indian resident and a non-resident, an amount not exceeding 25% of the total consideration –

(A) may be deferred or settled through escrow for a period not exceeding 18 months from the date of transfer agreement; or

(B) may be indemnified by the seller for a period not exceeding 18 months from the date of the payment of the full consideration.

While point (A) is often seen in practice, it does provide limited flexibility of 18 months. To address this, one can consider structuring staggered acquisition of shares over a period of time where performance needs to be comforted with an appropriate legal documentation or even using dilutive convertible instruments to the extent possible.

Disclosure lists, indemnities, representation and warranties:

While some of the risks are still not insurable, significant reliance and discussions could be around various disclosures since some of the standard representations may not hold good; let’s say the possibility of one of the largest customers calling off a contract, or a vendor renegotiating prices causing material adverse effect, etc.

It is imperative to provide for sufficient headroom for financial covenants typically agreed in shareholder agreements, especially for credit or quasi-credit deals.

Transaction structuring-related aspects:

Most often we see peculiar structuring needs around optimising tax costs, timelines, low compliances, etc. Table A (See below) provides a quick view of key parameters of some basic structuring ideas.

CONCLUSION

At the cost of many innocent lives, these unprecedented times are expected to bring in significant focus on sustainability and on an essentially minimalist and fundamental approach for any action or decisions. The ongoing fiscal, regulatory and geo-political changes are expected to add to the vibrancy for a living or corporal person.

Depending upon the strategy a business may adopt, defensive measures could help to protect the future and aggressive actions could actually help in transforming or even re-writing the future. On this positive note, we continue to look forward to some interesting corporate actions and decision-making.

Table A

| Important Covid-19 Parameters |

Share Acquisition / Slump Sale |

Scheme of Arrangement (NCLT Route) |

| Consideration |

Cash flows or share swaps |

More flexible & comprehensive. Issue shares, convertible instruments, other securities or cash flow |

| Valuation |

Limited flexibility on account of certain taxation and commercial aspects and related costs |

Ability to structure the valuation subject to going concerns and future parameters |

| Tax Outflow |

Immediate tax liability – could put pressure on cash flows |

Could be structured as tax neutral combination or divestment, thereby postponing actual tax incidence to the liquidity event |

| Timelines |

1 to 2 months

(Could increase in case of regulatory involvement) |

4 to 8 months subject to NCLT process |

| Stamp Duty Costs |

Subject to state-specific laws

Could range between 0.25% to 3%, depending upon transfer of shares or transfer of business |

Subject to state laws

Example, in Maharashtra – It is higher of 0.7% of value of shares issued and 5% of value of immoveable property situated in the state, subject to overall cap of 10% in the value of shares issued |

| GST |

Share transfers excluded. Asset sale subject to GST |

Transfer of business undertakings may not be subject to GST |