(This is the eighth and last article in the CARO 2020 series that started in June, 2021)

PART A – RESIGNATION OF STATUTORY AUDITORS

BACKGROUND

There have been several instances of resignations by statutory auditors mid-way through their tenures in the recent past. Whilst that may be legally permissible, what is more important is whether there is anything which is more than what meets the eye in the resignation that the incoming auditor needs to know. Also, resignation of an auditor of a listed entity/its material subsidiary before completion of the review/audit of the financial results/statements for the year due to frivolous reasons such as pre-occupation may seriously hamper investor confidence and deny them access to reliable information for taking timely investment decisions.

SCOPE OF REPORTING

The scope of reporting pertaining to the aforesaid clause is as under:Whether there has been any resignation of the statutory auditors during the year, if so, whether the auditor has taken into consideration the issues, objections or concerns raised by the outgoing auditors.

[Clause 3(xviii)]

PRACTICAL CONSIDERATIONS IN REPORTING

Before proceeding further it would be pertinent to note certain statutory requirements and professional pronouncements.SEBI Circular [CIR/CFD/CMD1/114/2019 dated 18th October, 2019]

The key requirements in respect thereof are summarised hereunder:

a) All listed entities/material subsidiaries shall ensure compliance with the following conditions while appointing/re-appointing an auditor:

• If the auditor resigns within 45 days from the end of a quarter of a financial year, then the auditor shall, before such resignation, issue the limited review/ audit report for such quarter.

• If the auditor resigns after 45 days from the end of a quarter of a financial year, then the auditor shall, before such resignation, issue the limited review/ audit report for such quarter as well as the next quarter.

• Notwithstanding the above, if the auditor has signed the limited review/ audit report for the first three quarters of a financial year, then the auditor shall, before such resignation, issue the limited review/ audit report for the last quarter of such financial year as well as the audit report for such financial year.

b) The auditor proposing to resign shall bring to the notice of the Audit Committee the reasons for his resignation including but not limited to areas where he has not been provided the necessary information / documents and explanations to matters raised during and in connections with the audit.

c) The above information has to be provided to the company in the format specified in Annexure A of the Circular, as under:

|

Sr.

No.

|

Particulars

|

|

1

|

Name of the listed

entity/ material subsidiary:

|

|

2

|

Details of the

statutory auditor:

a. Name:

b. Address:

c. Phone number:

d. Email:

|

|

3

|

Details

of association with the listed entity/ material subsidiary:

a.

Date on which the statutory auditor was appointed:

b.

Date on which the term of the statutory auditor was scheduled to expire:

c.

Prior to resignation, the latest audit report/limited

review report submitted by the auditor and date of its submission.

|

|

4

|

Detailed

reasons for resignation:

|

|

5

|

In

case of any concerns, efforts made by the auditor prior to resignation

(including approaching the Audit Committee/Board of Directors along with the

date of communication made to the Audit Committee/Board of Directors)

|

|

6

|

In

case the information requested by the auditor was not provided, then

following shall be disclosed:

a.

Whether the inability to obtain sufficient appropriate audit evidence was due

to a management-imposed limitation or circumstances beyond the control of the

management.

b.

Whether the lack of information would have significant impact on the

financial statements/results.

c.

Whether the auditor has performed alternative procedures to obtain

appropriate evidence for the purposes of audit/limited review as laid down in

SA 705 (Revised).

d.

Whether the lack of information was prevalent in the previous reported

financial statements/results. If yes, on what basis the previous

audit/limited review reports were issued.

|

|

7

|

Any other facts

relevant to the resignation:

|

Declaration

I/ We hereby confirm that the information given in this letter and its attachments is correct and complete.

I/ We hereby confirm that there is no other material reason other than those provided above for my resignation/ resignation of my firm.

Signature of the authorized signatory

Date:

Place:

Enclosures:

d) The listed entity / material subsidiary should cooperate in providing all the information and documents as requested by the auditor.

e) Disclosure should be made by the company as soon as possible but not later than twenty four hours of the Audit Committees’ views.

Duty of Outgoing Auditor [Section 140(2) of Companies Act, 2013]

The auditor who has resigned from a company shall file within a period of 30 days from the date of resignation a statement in Form ADT-3 with the company and the Registrar of Companies. In the case of a government company or any other company-owned or controlled by any of the governments, the auditor shall also file such a statement with the Comptroller and Auditor-General of India.

Clause 8 of Part I of First Schedule of the Chartered Accountants Act, 1949

A Chartered Accountant in practice shall be deemed to be guilty of professional misconduct, if he accepts a position as auditor previously held by another chartered accountant without first communicating with him in writing;

The underlying objective is that the member may have an opportunity to know the reasons for the change in order to be able to safeguard his own interest, the legitimate interest of the public and the independence of the existing accountant. It is not intended, in any way, to prevent or obstruct the change. When making the enquiry from the outgoing auditor, the one proposed to be appointed or already appointed should primarily find out whether there are any professional or other reasons why he should not accept the appointment.

The existence of a dispute as regards the fees would not constitute valid professional reasons on account of which an audit should not be accepted by the member to whom it is offered. However, in the case of an undisputed audit fees for carrying out the statutory audit under the Companies Act, 2013 or various other statutes having not been paid, the incoming auditor should not accept the appointment unless such fees are paid.

Implementation Guide on Resignation/ Withdrawal from an Engagement to Perform Audit of Financial Statements Issued by ICAI (the “Implementation Guide”)

In view of the increasing instances of withdrawal from audit engagements mid-way through the tenure, the ICAI has issued the above Implementation Guide that the outgoing and incoming auditors need to be aware. The Implementation Guide identifies various reasons for the resignation of auditors as under:

• SA 210 “Agreeing to the Terms of Audit Engagements” – If the auditor is unable to agree to a change in the terms of the audit engagement and is not permitted by the management to continue the original audit engagement, the auditor shall withdraw from the audit engagement.

• SA 220 “Quality Control for an Audit of Financial Statements” – If the engagement partner is unable to resolve the threat to independence with reference to the policies and procedures that apply to the audit engagement, if considered appropriate, the auditor can withdraw from the audit engagement.

• SA 240, “The Auditor’s Responsibilities relating to Fraud in an Audit of Financial Statements” – If, as a result of a misstatement resulting from fraud or suspected fraud, the auditor encounters exceptional circumstances that bring into question the auditor’s ability to perform the audit, the Standard suggests the withdrawal from the engagement as one of the options, subject to following certain procedures and measures.

• SA 315, “Identifying and Assessing the Risks of Material Misstatements Through Understanding the Entity and its Environment” – Concerns about the competence, integrity, ethical values or diligence of management, or about its commitment to or enforcement of these, may cause the auditor to conclude that the risk of management misrepresentation in the financial statements is such that an audit cannot be conducted. In such a case, the auditor may consider, where possible, withdrawing from the engagement, unless those charged with governance put in place appropriate corrective measures.

• SA 580, “Written Representations”– If the auditor is unable to obtain sufficient appropriate audit evidence, then the auditor is expected to determine the implications thereof to decide whether to qualify the opinion or to resign.

• Non-payment of auditor’s remuneration.

• Issuance of a Qualified report.

The Implementation Guide emphasises that the auditor is expected to describe the above specific circumstances, amongst others, while giving the reasons for resignation, instead of mentioning ambiguous reasons such as other preoccupation or personal reasons or administrative reasons or health reasons or mutual consent or unavoidable reasons.

Keeping in mind the above reporting requirements, the following are some of the practical considerations that could arise whilst reporting under this clause:

a) Modified Report issued by the outgoing auditor:-The nature and extent of the modification should be critically evaluated by the incoming auditor both from a qualitative and quantitative perspective. In doing so he may have to generally rely on oral discussions with the outgoing auditor since he may not be willing to part with the internal documentation and working papers, especially if it is an unlisted / non-public interest entity to which the SEBI circular mentioned earlier would not apply. In such circumstances he should advise the outgoing auditor to communicate in writing the specific reasons for withdrawal as per the Implementation Guide mentioned above to the appropriate level of management and those charged with governance and insist on a copy thereof, especially if the minutes do not reveal much. In such cases, there is no rule, written or unwritten, which would prevent an auditor from accepting the appointment in these circumstances once he has conducted proper due diligence before accepting the audit. He may also consider the attitude of the outgoing auditor and whether it was proper and justified.

b) Performing appropriate due diligence before stepping into the Outgoing Auditors shoes:- It is imperative that the incoming auditor undertakes appropriate inquiries and performs due diligence procedures as under before stepping into the shoes of the outgoing auditor who has withdrawn from the engagement:

(i) Evaluate diligently about the entity, the scope of the mandate, the resources (time, manpower and competence) available to execute the audit and then take a conscious call to accept or not to accept the engagement.

(ii) Have auditors frequently resigned from the entity in the past.

(iii) Evaluate the reasons for issuance of qualified, disclaimer opinion by the outgoing auditor.

(iv) Whether entity is regular in payment of statutory dues.

(v) Review the financial statements to ascertain any indication that the going concern basis may not be appropriate.

(vi) Check and understand accounting policies or treatment of specific transactions that cast doubt on the integrity of the financial information.

(vii) Are there issues arising from communication with the outgoing auditors, professional or otherwise, which suggest that the incoming auditor should decline the appointment.

(viii) Check whether the entity is involved in any long drawn litigation with the regulatory authorities.

(ix) Consider any other information available in the public domain.

CONCLUSION

The regulators have tightened the rules for withdrawal by statutory auditors from the engagement midway through their tenure to ensure that companies do not go scot-free and brush under the carpet any irregularities and misappropriations. The reporting responsibilities under this clause would ensure that there is a proper channel of communication between the incoming and outgoing auditors regarding any adverse matters concerning the entity.

PART B – CORPORATE SOCIAL RESPONSIBILITY (CSR)

BACKGROUND

The provisions dealing with CSR have been in force for a few years and many companies have now ingrained it as part of their DNA. Earlier, the approach of the regulators was more in the nature of ‘comply or report’. However, the emphasis is now on ensuring that companies take their CSR obligations more seriously. Earlier, there was no responsibility on auditors to comment on CSR compliance separately, and only the Board of Directors were required to report on the same. However, reporting under CARO 2020 would ensure greater accountability on companies who were not taking CSR seriously.

SCOPE OF REPORTING

The scope of reporting pertaining to the aforesaid clause is as under:

a) Whether, in respect of other than ongoing projects, the company has transferred unspent amount to a Fund specified in Schedule VII to the Companies Act within a period of six months of the expiry of the financial year in compliance with second proviso to sub-section (5) of section 135 of the said Act. [Clause 3(xx)(a)]

b) Whether any amount remaining unspent under sub-section (5) of section 135 of the Companies

Act, pursuant to any ongoing project, has been transferred to special account in compliance with the provision of sub-section (6) of section 135 of the said Act. [Clause 3(xx)(b)]

PRACTICAL CONSIDERATIONS AND CHALLENGES IN REPORTING

Before proceeding further it would be pertinent to note certain statutory requirements:

Additional Disclosures under amended Schedule III

While reporting under this Clause, the auditor will have to keep in the mind the amended Schedule III disclosures which are as under:

Where the company covered under section 135 of the companies act, the following shall be disclosed with regard to CSR activities in the financial statements;

|

1

|

amount

required to be spent by the company during the year,

|

|

2

|

amount

of expenditure incurred,

|

|

3

|

shortfall

at the end of the year,

|

|

4

|

total

of previous years shortfall,

|

|

5

|

reason

for shortfall,

|

|

6

|

nature

of CSR activities,

|

|

7

|

details

of related party transactions, e.g., contribution to a trust controlled by

the company in relation to CSR expenditure as per relevant Accounting

Standard/ Indian Accounting Standard,

|

|

8

|

where

a provision is made with respect to a liability incurred by entering into a

contractual obligation, the movements in the provision during the year should

be shown separately.

|

Whilst reporting, the auditor should make a cross reference to the above disclosures made in the financial statements to ensure that there are no inconsistencies.

Other Relevant Statutory Provisions

Section 135(5) and (6) of the Companies Act, 2013

Section 135(5):

The Board of Directors of every eligible company shall ensure that the Company spends in every financial year, at least 2% of the average net profits of the company during the 3 immediately preceding financial years, in pursuance of the CSR policy. The net profit shall be as computed in terms of section 198.

The expression “three immediately preceding financial years” in sub-section (5) shall be read as number of years completed by a newly incorporated company.

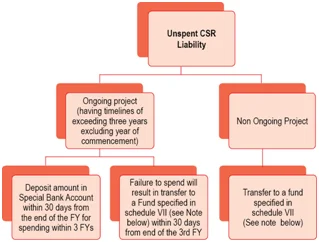

“Unspent amount” as referred to in sub-section (5) unless relates to an “ongoing project” shall be transferred to a fund specified in Schedule VII within 6 months of the end of the financial year.

Section 135(6):

Any amount remaining unspent under sub-section (5), pursuant to any ongoing project, fulfilling such conditions as may be prescribed, undertaken by a company in pursuance of its Corporate Social Responsibility Policy, shall be transferred by the company within a period of thirty days from the end of the financial year to a special account to be opened by the company in that behalf for that financial year in any scheduled bank to be called the Unspent Corporate Social Responsibility Account, and such amount shall be spent by the company in pursuance of its obligation towards the Corporate Social Responsibility Policy within a period of three financial years from the date of such transfer, failing which, the company shall transfer the same to a Fund specified in Schedule VII, within a period of thirty days from the date of completion of the third financial year.

Permissible CSR Activities [Schedule VII read with the Rules]:

Schedule VII prescribes the following broad heads of activities on which the prescribed classes of Companies need to spend to fulfil their CSR obligations:

|

Sub

Clause

|

Broad

Area

|

Projects

or Programmes related to Activities in the following areas

|

|

i)@

|

Hunger,

Healthcare,

Sanitation etc.

|

• Eradicating extreme hunger, poverty and

malnutrition

• Promoting health care including

preventive health care and sanitation

• Contribution to the Swatch Bharat Kosh.

• Provision for aids and appliances to

differently abled persons *

|

|

i)@

|

(continued)

|

• Disaster relief in

the form of medical aid, supply of clean drinking water and food supply*

• Trauma care around

highways in case of accidents*

• Supplementing of

Government Schemes like mid-day meal by corporates through additional

nutrition*

• Enabling access to

or improving delivery of public health systems (also covered under Clause iv

below)*

• Social Business

Projects involving giving medical and legal aid to road accident victims*

(also under Clause ii below)

|

|

ii)@

|

Education and vocational skills

|

• Promotion of education including special

education and employment enhancing vocational skills amongst:

(i) children,

(ii) women,

(iii) elderly, and

(iv) differently abled.

• Road safety awareness programmes

including drivers training, training

to enforcement personnel, traffic safety*

• Awareness of the above aspects through

print, audio and visual media*

• Setting up of Research Training and

Innovation Centres for the benefit of

predominantly the rural community covering the following aspects:

(i) Capacity building for farmers covering best

sustainable farm management practices*

(ii) Training agricultural labour on skill development*

• Providing Consumer Protection Services

covering the following aspects:

(i) Providing effective consumer grievance redressal

mechanism*

(ii) Protecting consumer’s health and safety,

sustainable consumption, consumer service, support and complaint resolution*

(iii) Consumer rights to be mandated*

(iv) All other consumer protection programmes and

activities*

• Donations to IIMs for conservation of

buildings and renovation of classrooms (also covered under clause v below)*

• Donations to Non Academic Technopark not

located within an academic institution

but supported by the Department of Science and Technology*

• Research and case studies in the areas

specified in Schedule VII (normally under the respective areas and, if not,

under this clause)*

|

|

iii)

|

Gender

equality

and

empowerment

of

disadvantaged

sections

|

• Promoting gender equality,

• Empowering women,

• Setting up of hostels, old age homes and

hostels for women and orphans, day care centres and such other

facilities for senior citizens, and

• Measures for reducing inequalities faced

by socially and economically backward groups.

• Slum Rehabilitation Projects and EWS

Housing*

|

|

iv)

|

Environmental

and

ecological

sustainability

and

conservation

of

natural

resources

|

• Maintaining ecological balance,

• Protection of flora and fauna,

• Maintaining quality of air and water

• Contribution to the Clean Ganga Fund

• Setting up of Research Training and

Innovation Centres for the benefit of predominantly the rural community

covering the following aspects:

(i) Doing own research on the field for individual

crops to find out the most cost optimal and agri-ecological sustainable farm

practices with a focus on water management*.

(ii) To do Product Life Cycle Analysis from the solid

conservation point of view*

• Renewable energy projects*

|

|

v)

|

Heritage,

Art and

Culture

|

• Protection of natural heritage,

• Protection of art and culture,

• Restoration and maintenance of related

buildings and sites of historical importance and works of art,

• Setting up public libraries,

• Promotion and development of traditional

arts and handicrafts

|

|

vi)

|

Armed

Forces

|

Measures for the benefit of:

(i) armed forces,

(ii) veterans, and

(iii) war widows.

|

|

vii)

|

Sports

|

• Training to promote:

(i) rural sports,

(ii) nationally recognised sports,

(iii) paralympic sports, and

(iv) Olympic sports

• Any training provided outside India to

sports personnel representing any State or Union Territory at National or

International level.

|

|

viii)

|

Political

Contributions

|

• Contributions to Prime Ministers National

Relief fund or

• Contributions to other funds set up by

the Central

Government for socio economic development

and relief and for the welfare of:

(i) Scheduled Castes,

|

|

viii)

|

(continued)

|

(ii) Scheduled Tribes

(iii) other backward classes and

(iv) women

|

|

ix)

|

Technology

Incubators

|

Contributions or funds provided to

technology incubators located within academic institutions approved by the

Central Government.

|

|

x)

|

Rural Development Projects

|

Any project meant for development of rural

India will be covered*

|

|

xi)

|

Slum Development Projects

|

Any project for development of slums would

be covered

|

|

xii)

|

COVID -19 Related Areas

|

Funds may be spent for COVID-19 purposes

under the following activities/Funds:

• Eradicating hunger, poverty and

malnutrition $

• Disaster

Management, including relief, rehabilitation and reconstruction activities $

• Contribution

to PM Cares Fund $

• Contribution

to State Disaster Management Authority $

• Ex-gratia

payment to temporary/casual/daily wage workers for the purpose of fighting

COVID-19 $

• Spending for setting up makeshift

hospitals and temporary COVID care facilities will be eligible under items

(i) and (xii) of Schedule VII. #

• Companies

engaged in R & D activities for new vaccines, drugs and medical devices

in the normal course of business may undertake similar new activities for

COVID-19 related matters for FYs 2020-21, 2021-22 and 2022-23 subject to the

following conditions:

a) Such

activities are carried out in collaboration with institutes or organisations

mentioned in item ix of Schedule VII

b)

Details thereof are disclosed in the Annual Report on CSR Activities

[Inserted

in the CSR Amendment Rules vide notification dated

24th August, 2020]

|

*As per the MCA Circular dated 18th June, 2014 providing clarifications on various aspects related to CSR activities.

@ The above referred circular provides that the items included under sub clauses (i) and (ii) above, should be interpreted liberally so as to capture their essence.

The above circular has also clarified on certain related aspects as under:

• One off events like marathons, awards, charitable concerts, sponsorship programmes etc. would not qualify as CSR expenditure.

• Only activities undertaken in project / programme mode are permissible.

• Expenses incurred in pursuance of legal obligations under Land, Labour or other laws would not quality as CSR expenditure.

$ As per MCA Circular dated 23rd March, 2020.

# As per MCA Circular dated 22nd April, 2021.

Monitoring Unspent Funds:

The provisions dealing with tracking and treatment of unspent funds, excess amounts spent and capital assets created or acquired as per the recent amendments which are crucial to reporting under this clause are tabulated and summarised hereunder:

Note:

The Funds specified under Schedule VII are as under:

• PM National Relief Fund

• Swach Bharat Kosh

• Clean Ganga Fund

• PM CARES Fund

• State Disaster Management Authority

• Skill Development Fund

Excess Amounts Spent:

As per the amended Rules, notified on 22nd January, 2021, any excess amount beyond the prescribed limit can be set off against the spending requirements in the immediately succeeding three financial years subject to the following conditions:

a) The excess amount available for set-off shall not include any surplus arising out of the CSR activities.

b) The Board of Directors shall pass a resolution specifically permitting the same.

The aforesaid carry forward shall not be allowed for excess amounts spent during any financial year ended before 22nd January, 2021.

Creation and Acquisition of Capital Assets:

As per the amended Rules, any CSR amounts may be utilised by a Company towards creation or acquisition of capital assets, only if the assets are held by any of the following:

a) A company registered under Section 8 of the Act, or a Registered Public Trust or Society having charitable objects and a CSR Registration Number; or

b) Beneficiaries of the said CSR project in the form of Self-Help Groups or Collective Entities; or

c) A public authority.

In case of any such assets existing prior to the amendment i.e. 22nd January, 2021, the same shall be transferred within 180 days from the commencement date.

Keeping in mind the above reporting as well as requirements, the following are some of the practical challenges that could arise in reporting under these clauses:

a) Reporting Issues and Challenges in the Initial Period of Applicability:- The amendments are prospective from 22nd January, 2021. Accordingly only the unspent amount for F.Y. 2020-21 in respect of other than ongoing projects needs to be transferred to the fund specified in Schedule VII within six months from the end of the financial year. This is the case even if the Company has unspent amounts in earlier years. However, if the Company has made provisions for unspent amounts of the earlier years, which remains outstanding as on 31st March, 2021 the same should be transferred to the separate bank account or Schedule VII fund as the case may be within the prescribed periods as indicated earlier. The auditors should ensure that appropriate factual disclosures are made where deemed necessary. Further, there could be several other practical issues which could be encountered in the first year of reporting, few of which are discussed hereunder together with their possible resolution by the auditors, coupled with appropriate reporting of all relevant facts as deemed necessary based on their best judgement:

|

Issues

|

Possible

Resolution

|

|

A Company has a running project that was

commenced few years back and is expected to continue for next 2 years. Can

this be considered as an Ongoing project?

|

Subject to the definition of ongoing

project in terms of the timeline, the Board of Directors can henceforth

consider and approve this current running project as an Ongoing Project with

reasonable justification.

|

|

A CSR project was undertaken and

subsequently abandoned by Implementing Agency due to lack of additional

funds. Can this be considered as an Ongoing project?

|

Subject to the definition of ongoing

project in terms of the time line, the Board of Directors can henceforth consider and approve the aforesaid project

as an Ongoing Project with reasonable justification.

|

|

A Company contributed a certain amount to

the Implementing Agency for the construction of a hospital. It paid the full

amount in F.Y. 2020-21, whereas the hospital is expected to be completed in

F.Y. 2022-23. Can this be considered as an Ongoing project?

|

If the Company has already paid the whole

amount of its CSR obligations during F.Y. 2020-21, then it is not required to

consider it as Ongoing Project. However, it is the duty of the Board as per

Rule 4 (5) to satisfy itself that the funds so disbursed have been utilized

for the purpose and in the manner as approved by it and the CFO or the person

responsible for financial management need to certify to that effect. Hence

the Company needs to have a report from the Implementation Agency for the

spends and utilization of funds and report it in the Board Report for F.Y.

2020-21 with facts and details. Further, a mandatory impact assessment

needs to be done by a Monitoring Agency in case of companies with mandatory

spending of Rs. 10 crores or more in the three immediately preceding

financial years and for individual project outlays in excess of Rs.1 crores as

per the amended Rules.

|

b) Monitoring in case of Multiple Projects:– In case of companies having huge CSR budgets and financing multiple projects, both ongoing and others, a robust internal control mechanism would have to be implemented to monitor project-wise utilisation to ensure that unspent amounts are transferred on a timely basis and their subsequent utilisation in case of ongoing projects, which needs to be verified by the auditors to enable them to report compliance under Clause 3(xx)(b). Whilst there is no requirement to maintain separate special bank accounts for each project it is desirable to ensure proper monitoring and greater transparency. The Board may consider laying an appropriate policy in this regard.

c) Funds Utilised towards acquisition of Capital Assets in earlier periods:- For companies that have utilised funds in earlier periods and shown them as capital assets, it is mandatory to transfer the same within 180 days from 22nd January, 2021 to the prescribed authorities /entities as indicated earlier. Though no specific reporting is required under these clauses, it would be incumbent on the auditors to verify the same as part of their audit and in case the report is dated after the expiry of the said period, he may consider drawing attention to the same since it is a statutory requirement. Similar factual disclosure could be considered in the case where the period of 180 days has not elapsed on the date of signing, and the same are not transferred.

d) Transactions with Related Parties:- In many companies, CSR obligations are fulfilled by transferring the funds to group entities registered as NPOs under Section 8/25 of the Companies Act, 2013 / 1956. In such cases, care should be taken to ensure that the same are towards approved projects. The monitoring of the same is done in accordance with the revised guidelines on monitoring and impact assessment, including the need for involving an external agency, if required, as discussed earlier. In case of any lapses or deficiencies noticed the same should be factually reported under Clause 3(xx)(b) based on materiality and use of judgement.

CONCLUSION

The additional reporting requirements have placed very specific responsibilities on the auditors to supplement the revised regulatory landscape of CSR of “comply or pay up”, which views CSR spending more as a tax then a social obligation. As is always the case, it is the auditors who have to bell the cat!