Justice Delayed Is Justice Denied

VISHWAS BADHAO, VIVAD GATAO

In the recent decision in the case of OM Vision Infrasapce Private Limited vs. ITO, the Gujarat High Court (HC) made serious observations on the pendency of appeals before CIT(Appeals). It was a case where the petitioner approached the Court against the recovery proceedings pending appeals before the CIT(A). The Court took serious note of pending appeals before the CIT(A) for more than three to four years and issued notices to the Chairman, CBDT, The Finance Secretary, Principal CCIT (National Faceless Appeal Centre, Delhi) seeking replies on the pendency of appeals before the CIT(A), the average life of the appeal (i.e., time taken for the disposal of appeal), how many appeals are allocated on an average basis to each Commissioner and remedial measures suggested by the CBDT in cases of inordinate delay, as in the case of the appellant.

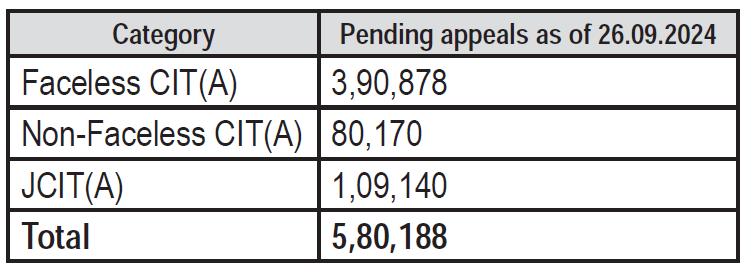

Interestingly, the Income-tax Department filed an affidavit giving the following statistics of the pending appeals as of 26th September, 2024:

With 279 CIT(A) working in a faceless manner, 64 CIT(A) working in a non-faceless manner, and 100 JCIT(A), the average pendency of appeals with faceless CIT(A) was around 1,400 cases and around 1,252 cases with non-faceless CIT(A) as at 26th September, 2024. The High Court expressed its displeasure with the huge pendency of appeals and lack of any concrete plan to dispose of them expeditiously and ruled in favour of the petitioners to grant a stay on recovery of the entire demand during the pendency of their appeals.

The pendency of appeals with CIT(A) has been a serious issue since the introduction of the faceless appeals scheme. The pendency is increasing day by day with Assessing Officers continuing to do high-pitched assessments, unwarranted adjustments being made by CPC while processing returns under section 143(1), frivolous additions / disallowances, denying credit of TDS / TCS, rectification applications being summarily dismissed, and other issues.

The Memorandum explaining the provisions of the Finance (No.2) Bill 2024 acknowledges the mounting pendency of cases at the CIT(A) level and the overall increase in litigation at various levels due to a larger number of new appeals than the number of appeal disposals.

Recently, the Supreme Court upheld the notices for re-opening the assessment under section 148 (under the erstwhile provisions of law), impacting more than 90,000 cases, thereby unsettling settled cases. As and when assessments are completed in these cases, a round of fresh litigation may start.

If we add the pendency of cases with the Tribunal, High Courts and the Supreme Court, the figure would be alarming.

To address the issue, the government appointed 100 JCIT(Appeals) in 20231, also notified the e-Dispute Resolution Scheme in 2022, and enacted the Direct Tax Vivad se Vishwas Scheme 2024 (DTVSV 2.0). However, these measures are grossly insufficient, without any definitive timeline for completing the pending appeals or deciding cases by the various authorities / courts. Radical measures are certainly called for. At the current rate of disposals, it would take about five years to dispose of the existing pendency. Bunching of similar appeals or repeated issues for different succeeding years in appeals, covered matters, etc., could be one of the solutions which can help in the speedy disposal of appeals by CIT Appeals.

1.Section 246 and E-Appeals Scheme, 2023 dated 29th May, 2023

In the given scenario, taxpayers can avail the benefits of the DTVSV 2.0. However, this scheme may really be of assistance only to taxpayers whose appeals are pending at higher appellate levels.

DIRECT TAX VIVAD SE VISHWAS SCHEME, 20242

The first DTVSV was brought out by the Government in 2020 for the appeals pending as on 31st March, 2020 and was successful in garnering revenue to the tune of about ₹75,000 crores from about one lakh taxpayers. The objective of DTVSV 2.0 is to provide a mechanism for the settlement of disputed issues, thereby reducing litigation without much cost to the exchequer.

DTVSV 2.0 provides for a lower rate of taxes for the new appeals as compared to the old appeals. Old appeals are those which are pending since prior to 31st January, 2020, and the new appeals are those filed after 31st January, 2020 and pending as on 22nd July, 2024. In the case of old appeals where the declaration is filed before 31st December, 2024, 110 per cent of the disputed tax is to be paid. The corresponding rate is 120 per cent if the declaration is made on or after 1st January, 2025. For new appeals, 100 per cent of the disputed tax is to be paid for declaration filed on or before 31st December, 2024 and 110 per cent for declaration filed on or after 1st January, 2025. The amount payable under the scheme will be reduced to 50 per cent in cases where the Income-tax Department files the appeal or if the taxpayer’s case has been decided in his favour by the ITAT / High Court and has not been reversed by the higher authority, namely, High Court or Supreme Court, as the case may be.

The new scheme does not apply to search and seizure cases, or where the prosecution is launched before filing the declaration or where disputes are relating to undisclosed foreign sources of income or assets, or tax arrears pertaining to assessments or reassessments based on information received from the foreign government/s. Besides, the large number of writ petitions against reassessment proceedings, moving back and forth between the High Courts and the Supreme Court, would also not be eligible for settlement under the scheme. The scheme does not apply to cases where the time limit for filing appeals has not expired as on 22nd July, 2024, if the taxpayer does not file an appeal. The last date for the scheme is not yet announced.

Broadly, some taxpayers having long pending demands may benefit from the scheme, as it provides substantial relief in interest and penalty amount. In any case, one needs to do a cost-benefit analysis. On the one hand, there is a huge cost of litigation, mental stress, waste of time and energy and yet, the uncertainty of outcome; while on the other hand, there is certainty and mental peace through settlement of disputes.

2. CBDT Circular No. 12 of 2024 dated 15th October, 2024

TRUST DEFICIT

It is said that prevention is better than cure. A scheme like DTVSV is not a permanent solution. It is good for settling the existing litigation, but not in arresting the creation of fresh litigation. For that, we need simpler laws and pragmatic administration based on trust and respect for the taxpayers. Assessing officers should be empowered with a positive mindset to facilitate taxpayers in compliance with laws and not threaten them with power and authority. High-pitched assessment orders, frivolous litigations, pressure for unreasonable recoveries, blatant violation of principles of natural justice, arbitrary disallowances of legitimate business expenses and so on have increased the trust deficit between the tax administration and taxpayers over the decades.

Both taxpayers and the tax administration need to work together to build a strong nation. It is heartening to note that the Government is aware of this and has taken steps to simplify provisions of the Income-tax Act. However, the need of the hour is simple yet effective tax administration. When we look at the quantum of tax litigations in India vis-à-vis some developed nations, we find a stark difference. There is a dire need for a drastic reduction of tax litigations in India by comprehensive measures of tax simplifications and administrative reforms.

Interestingly, the Ministry of Personnel, Public Grievances & Pensions issued a Print Release on 13th August, 2024 on “Less Government More Governance”3, announcing several measures to simplify tax laws, streamline Government administration, use of technology, repealing archaic laws etc. Let us hope that we get some lasting solution to reduce the tax litigation such that we can devote more time for some constructive work to make the dream of a developed India come true.

3. See Editorial for November, 2024 [56 (2024) 891 BCAJ]