CA Firm of 2030

Let me begin by wishing you all a very Happy New Year. Every January brings its familiar mix of resolutions and reflections. This one arrives with an unmistakable question for the profession: With gradual reduction in opportunities across compliance and regulatory services, what is the future of the profession? What would the CA Firm of 2030 look like? For many professionals, the gradual reduction in professional opportunities over the last decade and rapid technological advancements, including affordable AI, has created a sense of unease.

But perhaps this moment is not a threat; it is a signal. The CA firm of 2030 will not be defined by the number of audits or compliances performed but by the quality of insight, the sophistication of systems, and the breadth of services it delivers. The redesign of our profession begins now, not in 2030.

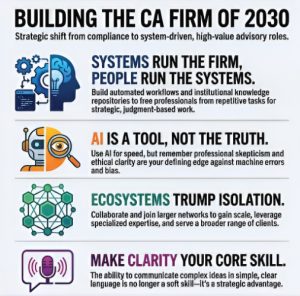

During my professional career, I have had the opportunity to visit firms of varying sizes and meet many professionals. The ones that felt genuinely future-ready were not necessarily the ones with the biggest teams, but those with the strongest systems, which in many cases, were automated. In one mid-sized practice, a GST reconciliation that earlier consumed a week was completed overnight because they had built an internal automation engine. The senior wasn’t replaced; he was liberated—able to focus on judgment rather than just data work. This is what the future will demand: humans doing the thinking, machines doing the lifting.

Yet digital capability brings a deeper responsibility. AI today can produce a draft submission or an audit memo in minutes. But the illusion of perfection can be dangerous, with high levels of hallucinations and bias. A young manager shared, “AI makes me faster, but forces me to be twice as sceptical.” She is right. As workflows automate, professional scepticism and ethical clarity become our defining edge. In a machine-first world, conscience becomes a competitive advantage.

Equally significant is the shift from individual-driven excellence to institutionalised resilience. Many firms still depend on a few irreplaceable seniors. When one leaves, years of templates, client nuances, and tacit knowledge vanish. A 2030-ready firm avoids this fragility by building documented SOPs, knowledge repositories, review layers, and digital memory. When such knowledge systems carry the practice, people can grow; when people alone carry it, systems collapse.

This transition to a process and system centric firm aligns closely with a broader national aspiration. The PMO’s recent push to develop large Indian accounting firms—firms with governance, specialisation, and scale comparable to global networks—captures a sentiment that has long been brewing. India’s economy demands Indian-origin institutions that can operate across cities, sectors, and service lines. I met a three-partner Jaipur firm that joined a national network and, within a year, began servicing a listed client by leveraging expertise from member firms in Mumbai and Bangalore. Their story mirrors the future: collaboration, scale, and ecosystems—not isolation—will define relevance.

Scale is just one determinant of relevance. Domain specialists can carve a niche to make scale redundant. In such a set-up, the objective is not to achieve high volume and low unit value but a low volume with high unit value. However, emphasis on processes, systems and collaboration will augur well in this approach too. A niche advise given to a client will also have to run through various processes to make sure it is balanced and implementable. In this complex world of information overload, knowledge systems can assist such expert to decipher relevant information and maintain his cutting knowledge edge. Collaboration may not take the structure of formal networks, but may be more through cordial human relationships to avoid the perception of being inaccessible or inapproachable.

And through all this, a human thread binds everything together: the ability to communicate clearly. Whether interpreting GST litigation trends, drafting an advisory note, or explaining risk in simple language, clarity has become a strategic skill. Good writing is not a cosmetic flourish; it is good thinking expressed. In the firm of 2030, every professional will need to be a designer of processes, systems, and words.

So here, at the start of 2026—amid regulatory shifts, AI acceleration, and a national call to build strong Indian accounting institutions—the real question is not, “What will happen to our profession?” but, “What will we choose to build?”

The firms that act now—by strengthening systems, embracing AI responsibly, collaborating intelligently, and communicating with clarity—will not just survive the decade. They will define it.