(Editorial Note: Given the increasingly important role played by NFRA in the context of auditing, BCA Journal, will be continuing with reporting on NFRA developments. This new feature titled NFRA DIGEST will cover orders, reports, circulars, notifications, rules, inspection reports, discussion papers, etc. BCAJ seeks to bring to light some of the important changes affecting the profession of audit with a view that members and readers can learn from these developments. The aim is to enable members to improve their audit processes and reduce their audit risk by improving quality and governance frameworks mandated by applicable standards and regulatory expectations. In this context, we are pleased to bring this new feature NFRA Digest to our readers, covering NFRA updates. This is another in a row and will cover the circulars issued by NFRA to date and NFRA orders post-December 2023)

BACKGROUND ABOUT NFRA ORDERS/CIRCULARS:

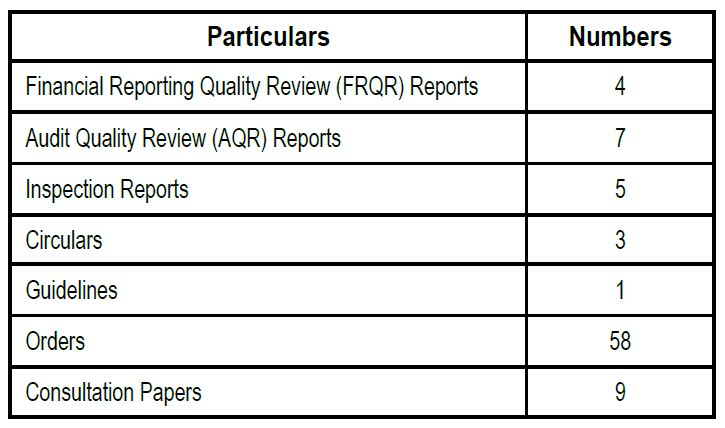

The National Financial Reporting Authority (“NFRA”) was constituted on 1st October, 2018, by the Government of India under section 132(1) of the Companies Act, 2013 (“the 2013 Act”). Since its inception, the NFRA has issued 67 orders till today highlighting significant deficiencies in the audit process, reporting by the auditors and other matters in relation to the audit of listed entities.

Our previous issues have covered, in detail, the structure of NRFA Orders and Powers of NFRA under Section 132(4)(c) of the 2013 Act with respect to the imposition of monetary penalties and debarment of the member or/and firm, where the professional or other misconduct is proved, key learnings from NFRA orders issued till 31st December, 2023.

In addition to these orders, the NFRA has also issued certain circulars on specific matters based on its findings during the proceedings or on its regular reviews. The NFRA has also issued an order highlighting significant deficiencies in an engagement other than audit engagements.

NFRA CIRCULARS

As per Sub-section 2(b) of section 132 of the Companies Act 2013 read with rule 4(2)(c) of the NFRA Rules 2018, the NFRA is mandated to monitor and enforce compliance with accounting and auditing standards. Further, NFRA is required by sub-section 2(d) of section 132 of the Act read with rule 4(2) of NFRA Rules, to perform such other functions and duties as may be necessary or incidental to the aforesaid functions and duties. NFRA monitors compliance with accounting standards by the companies as part of its review of published financial statements.

Based on these reviews, since inception, the NFRA has issued circulars on three important topics:

| Topics | Non-accrual of interest on borrowings |

| Date and Applicability of circular | 20th October, 2022

Applicability:

(a) All Listed companies (b) Unlisted companies specified in Rule 3 of NFRA Rules 2018 (c) Auditors of these companies |

| Summary of NFRA circular | Issue highlighted:

• The company had been classified as Non-Performing Asset (NPA) by the lender banks and was negotiating one-time settlements with the banks. The company had discontinued accrual/recognition of interest expense on these borrowings. • The company’s discontinuation of the recognition of accrual of interest while calculating the amortised cost of the borrowings was in violation of Effective Interest Method and Effective Interest Rate (EIR) principles. • The Statutory Auditors failed to identify and question the company on this change in accounting treatment and report on non-compliance with Ind AS. Requirement as per Ind-AS:

• As per para B3.3.1, a financial liability is extinguished only when the borrower is legally released from primary responsibility for the liability (or part of it) either by the process of law or by the creditor. • In the present case, the bank had not released the company from the liability of the borrowings as well the interest. The discontinuation of interest expense recognition on financial liability solely based on the Non-accrual of interest on borrowings borrowing company’s expectation of loan/interest waiver/concession without evidence of the legally enforceable contractual documents is non-compliance with Ind-AS. Hence, the company should have continued the accrual/recognition of interest expenses. Direction by NFRA: • All the companies required to follows Ind-AS and their audit committee are advised not to discontinue the recognition of principal and interest based on management expectation of likely settlement with or without concession from the banks. The auditors are required to ensure strict compliance with this circular. |

| Topics | Accounting policies for Revenue from Contract with Customers and Trade Receivables |

| Date and Applicability of circular | 29th March, 2023

Applicability:

(a) All Listed companies (b) Unlisted companies specified in Rule 3 of NFRA Rules 2018 (c) Auditors of these companies |

| Summary of NFRA circular | Issue highlighted:

• Revenue recognition: In many companies, it has been noticed that the significant accounting policies disclosed wrongly state that revenue is recognised and measured at fair value of the consideration received or receivable.

• Trade Receivables: In many companies it has been noticed that their accounting policy, either stating separately or as part of the policy for financial assets including trade receivables, wrongly stating that the trade receivables are initially recognised at fair value.

Requirement as per Ind-AS:

• Revenue recognition: As per para 46 of Ind AS 115, Revenue from contracts with customers requires that the entity shall recognise as revenue the amount of transaction price, excluding the estimates of variable consideration that is allocated to that performance obligation. Under Ind AS 115, the application of fair value is relevant only in a limited set of situations like fair value of consideration in form of other than cash. • Trade Receivables: As per para 5.1.3 of Ind AS 109, the financial assets in the form of trade receivables, shall be initially measured at their transaction price unless those contain a significant financing component determined in accordance with Ind AS 115.

Direction by NFRA: • The illustrative examples of correct accounting policies with respect to revenue recognition and trade receivables are mentioned in the circular. • All the listed companies and other entities falling with the domain of NFRA which are required to follow Ind-AS are hereby advised to comply with Ind AS 115 and Ind AS 109, as discussed above. The auditors of these companies are required to ensure strict compliance, in the performance of their audits, with the provision of the Ind ASs as brought out above. |

| Topics | Fraud Reporting- Statutory Auditors’ responsibilities |

| Date and Applicability of circular | 26th June, 2023

Applicability:

(a) Auditors of entities regulated by NFRA |

| Summary of NFRA circular | Issue highlighted:

• NFRA has noticed that auditors are not fulfilling their statutory responsibilities relating to reporting fraud as mandated under the Companies Act 2013 read with relevant rules and applicable Standards on Auditing (SAs).

• The Hon’ble Supreme Court of India in a recent judgement has held that the consequence of section 140(5) will be applicable also to those auditors who resign from their audit engagements without reporting fraud/suspected fraud.

Requirement under different provisions:

• Section 143(12) of CA 2013 and related rules lays down certain reporting responsibilities on the auditor in relation to fraud. Rule 13 of the Companies (Audit and Auditors) Rules 2014, prescribes detailed steps that need to be followed by auditors in relation to reporting of fraud.

• SA 240- The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements elaborately deals with the auditors’ responsibilities relating to fraud in an audit of financial statements. The guidance in SA 240 also details the communication to the management, TCWG and Regulatory & Enforcement authorities regarding reporting of fraud/suspected fraud.

Direction by NFRA:

• The Statutory Auditors is duty bound to submit Form ADT-4 to the Central Government u/s 143(12) even in cases where the Statutory Auditors is not the first person to identify the fraud/suspected fraud. • Resignations does not absolve the Auditor of his responsibilities to report suspected fraud or fraud as mandated by law. |

NFRA ORDERS:

A) On Statutory Audit Engagements: The observations summarised below relates to the orders issued by NFRA during the period from 01st January, 2024 to 30th April, 2024. Further, the issues covered in this publication represent additional/new observations other than those covered in the previous issues.

1. Despite of giving multiple communications by NFRA to submit the audit files through speed-post, e-mail communications and letters, EP did not respond. (Order No. 002/2024 dated 5th January, 2024)

2. Failure to evaluate the management’s assessment of the entity’s ability to continue as a Going concern despite the presence of significant indicators like defaults in repayment of Cash credit facilities and term loans, uncertainties relating to recoverability of trade receivables, continuing and increasing losses, negative operating cash flows, long delay in completion of many projects etc. (Order No. 003/2024 dated

08th January, 2024)

3. Failure to obtain sufficient appropriate audit evidence relating to revenue recognition and failure to evaluate the risk of fraud in revenue recognition. (Order No. 003/2024 dated 08th January, 2024)

4. Failure to perform physical verification or any alternate audit procedures to determine the existence and condition of inventory and also to modify his audit opinion with respect to inventory. (Order No. 003/2024 dated 08th January, 2024)

5. Failure to determine Materiality for the financial as a whole while establishing the audit strategy and to determine performance materiality for the purpose of assessing the risk of material misstatements and determining the timing, nature and extent of further audit procedures. (Order No. 003/2024 dated

08th January, 2024)

6. Failure to communicate in writing significant deficiencies in internal control with TCWG and with management on a timely basis. (Order No. 003/2024 dated 08th January, 2024)

7. Recognition of interest cost on borrowing rate at a rate lower than loan agreement for FY 2014–15 & 2015-16, disclosing balance interest liability as a contingent liability and non-recognition of interest at all for FY 2016–17 due to ongoing negotiations for restructuring of NPA accounts resulting into understatement of losses. (Order No. 005/2024 dated 22nd February, 2024)

8. Failure to obtain sufficient appropriate audit evidence for the verification of revenue. (Order No. 005/2024 dated 22nd February, 2024)

9. False reporting in CARO with respect to loans given to related parties. (Order No. 005/2024 dated 22nd February, 2024)

10. Violation of the Responsibilities as Joint Auditor. (Order No. 008/2024 dated 12th April, 2024)

11. Indulged in self-review by preparing material information for the financial statements of the Company, which subsequently became the subject matter of audit opinion, and this violated the Code of Ethics and Standards on Auditing. (Order No. 008/2024 dated 12th April, 2024)

12. Failure to analyse the contradictory evidence. (Order No. 008/2024 dated 12th April, 2024)

13. Failure to obtain sufficient appropriate audit evidence regarding the reasonability of estimate of Expected Credit Loss (ECL) on Financial Assets. (Order No. 008/2024 dated 12th April, 2024)

14. Acceptance of Audit Engagement before receipt of NOC from predecessor auditor (Order No. 012/2024 dated 26th April, 2024)

15. Not obtaining sufficient appropriate audit evidence of significant matters (fraud reported by previous auditors as the reason for resignation) reported by the previous auditor before acceptance of engagement and also during the course of audit and reporting.

B) On Other Engagements:

| Date of order | 3rd January, 2024 |

| Nature of Engagement | Reports u/s 80 JJAA of the Income Tax Act, 1961 |

| Observations by NFRA |

In the order, NFRA highlighted following significant deficiencies in the Form 10DA issued u/s 80JJAA of the Income-tax Act, 1961: a. Failure to verify reorganization of business with various parties

b. Failure to exclude employees whose contribution was paid by the Government c. Lapses in reporting additional employees d. Failure to verify payment of additional employee cost by account payee cheque/draft/electronic means e. Failure to verify the salary limit of ₹25,000 per month for new employees Based on the above, NFRA concluded that the |

Key Takeaways

The implementation of these circulars issued by NFRA on various matters will be reviewed for scrutiny by them in subsequent inspections of the entities or audit firms. Therefore, it is imperative that the audit firms should create adequate documentation in respect of their audit procedures and diligence applied to ensure compliance of the same either by an entity or themselves.

The NFRA’s recent action on certification engagement of listed entities carried out by CA firms is also one of its kind. The CAs in practice and specially engaged by listed entities for statutory audit or other engagements should exercise a greater degree of professional scepticism.

“It’s good to learn from your mistakes. It’s better to learn from other people’s mistakes.” Warren Buffett