A. KEY GLOBAL UPDATES

1. IASB: ILLUSTRATIVE EXAMPLES ON REPORTING UNCERTAINTIES IN FINANCIAL STATEMENTS

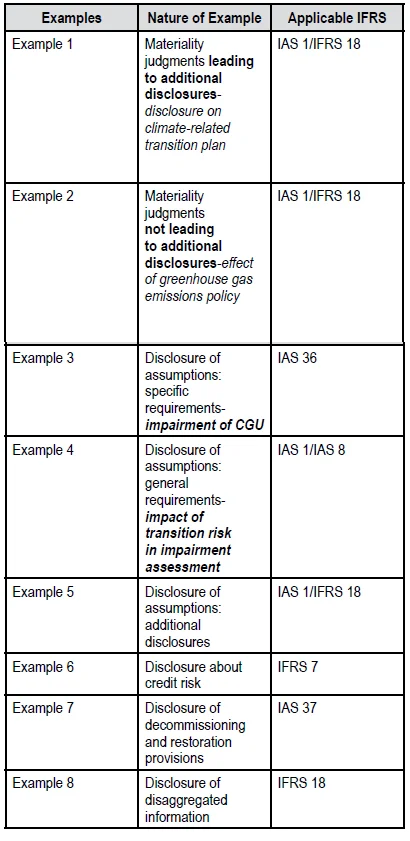

On November 28, 2025, the International Accounting Standards Board, in response to stakeholders’ concerns about the equity of information in financial statements relating to climate-specific and other uncertainties, issued illustrative examples on reporting such uncertainties in the financial statements.

Reporting uncertainties in the financial statements involves the exercise of judgement in determining what needs to be disclosed. This highlights the need for guidance to ensure consistency and sufficiency of disclosures relating to such uncertainties.

The examples highlight the following:

- Application of materiality for specific disclosures required by IFRS (Para 31 – IAS 1)

- Estimates used to measure recoverable amounts of cash-generating units containing goodwill or intangible assets with indefinite useful lives (Para 134 – IAS 36)

- Sources of estimation uncertainty (Para 125 – IAS 1)

- Credit Risk (Para 35A – IFRS 7)

- Indication of the uncertainties about the amount or timing of those outflows among other disclosures (Para 85 – IAS 37)

- Aggregation and disaggregation (Para 41 – IFRS 18)

The above examples reiterate the disclosure requirements prescribed in the above-mentioned standards and do not discuss any new matters.

2. FASB: NEW STANDARD TO IMPROVE INTERIM REPORTING

On December 08, 2025, the Financial Accounting Standards Board, to improve the guidance on interim reporting by improving the navigability of the required interim disclosures and clarifying when the guidance is applicable, issued a Narrow-Scope Improvements through Accounting Standards Update (ASU) – Interim Reporting (Topic 270).

The improvements are issued following feedback from the stakeholders about the challenges and complexity of Topic 270. As per the Financial Accounting Standards Board these challenges is a result of development of the source literature, the initial codification of the historical content, and subsequent amendments to the Topic as new accounting guidance was issued over time necessitating the improvements in Accounting Standards Update (ASU) – Interim Reporting (Topic 270).

The objective of the amendments is to provide clarity about the current requirements, rather than evaluate whether to expand or reduce interim disclosure requirements. These include:

- Applicability of Topic 270

- Types of interim reporting

- Form and content of interim financial statements

- Disclosure principle that requires entities to disclose events since the end of the last annual reporting period that have a material impact on the entity

These amendments in the Accounting Standards Update (ASU) – Interim Reporting (Topic 270) are effective for interim reporting periods within annual reporting periods beginning after December 15, 2027, for public business entities and for interim reporting periods within annual reporting periods beginning after December 15, 2028, for entities other than

public business entities. Early adoption is permitted for all entities.

3. FASB: NEW STANDARD TO IMPROVE HEDGE ACCOUNTING GUIDANCE

On November 25, 2025, the Financial Accounting Standards Board, to clarify certain aspects of the guidance on hedge accounting and to address several incremental hedge accounting issues arising from the global reference rate reform initiative, issued a Hedge Accounting Improvements through the Accounting Standards Update (ASU) – Derivatives and Hedging (Topic 815).

The improvements are a follow up to the amendments in the 2019 proposed update, which as per the stakeholders was inadequate in resolving the issues encountered by the stakeholders. Further, a need for update in several areas of the hedge accounting guidance to address the effects of reference rate reform on hedge accounting were identified in 2021 by the stakeholders.

The objective of the updates is to more closely align hedge accounting with the economics of an entity’s risk management activities. The following issues are discussed in the updates

- Similar Risk Assessment for Cash Flow Hedges: A group of individual forecasted transactions to have similar risk exposure rather than a shared risk exposure

- Hedging Forecasted Interest Payments on Choose-Your-Rate Debt Instruments: A module with simplified assumptions to assess the probability of occurrence of forecasted transactions and hedge effectiveness.

- Cash Flow Hedges of Nonfinancial Forecasted Transactions: Allows hedge accounting for eligible components of forecasted spot-market transactions, forward-market transactions, and subcomponents of explicitly referenced components in an agreement’s pricing formula.

- Net Written Options as Hedging Instruments: Accommodates differences in the loan and swap markets that resulted from the cessation of the LIBOR reference rate and eliminates the requirement for the net written option test in certain instances.

- Foreign-Currency-Denominated Debt Instrument as Hedging Instrument and Hedged Item (Dual Hedge): Eliminate the recognition and presentation mismatch related to a dual hedge strategy (that is, a hedge for which a foreign currency-denominated debt instrument is both designated as the hedging instrument in a net investment hedge and designated as the hedged item in a fair value hedge of interest rate risk).

These amendments in the Accounting Standards Update (ASU) – Derivatives and Hedging (Topic 815) are effective from annual reporting periods beginning after December 15, 2026, and interim periods within those annual reporting periods. For entities other than public business entities, the amendments are effective for annual reporting periods beginning after December 15, 2027, and interim periods within those annual reporting periods. Early adoption is permitted for all entities.

4. FASB: NEW STANDARD TO ADD GUIDANCE ON ACCOUNTING FOR GOVERNMENT GRANTS BY BUSINESSES

On December 04, 2025, the Financial Accounting Standards Board, to improve generally accepted accounting principles (GAAP) by establishing authoritative guidance on the accounting for government grants received by business entities, issued updates relating to accounting for Government Grants received by Business Entities through the Accounting Standards Update (ASU) – Government Grants (Topic 832).

These updates bring in specific authoritative guidance about the recognition, measurement, and presentation of a grant received by a business entity from a government which the GAAP did not provide. The absence of this guidance in the GAAP led the business entities to refer similar but not specific guidance on IAS 20 – Accounting for Government Grants and Disclosure of Government Assistance, Topic 450 – Contingencies (US GAAP) and Subtopic 958-605 – Not-for-Profit Entities—Revenue Recognition. Hence, to reduce diversity in practice and increase consistency among business entities these updates have been issued.

The following amendments are affected to the updates:

- Recognition criteria of a government grant received by a business entity if it meets the recognition guidance for a grant related to an asset or a grant related to income and depending upon probability of compliance with the conditions attached to the grant and the receivability of the grant.

- A grant related to an asset to be recognized on the balance sheet as a business entity incurs the related costs for which the grant is intended to compensate, either as a Deferred income (the deferred income approach) or as an adjustment to the cost basis in determining the carrying amount of the asset (the cost accumulation approach).

-

In case of deferred income approach:Measurement: a systematic and rational basis for income recognition over the periods in which a business entity recognizes as expenses the costs for which the grant is intended to compensate.Presentation: a general heading such as other income or deducted from the related expense.

-

In case of cost accumulation approach:Measurement: no separate subsequent recognition of the government grant proceeds in earnings. Depreciation or subsequent accounting depending upon the carrying amount of the asset.

These amendments in the Accounting Standards Update (ASU) – Government Grants (Topic 832) are effective for annual reporting periods beginning after December 15, 2028, and interim reporting periods within those annual reporting periods. For entities other than public business entities, the amendments are effective for annual reporting periods beginning after December 15, 2029, and interim reporting periods within those annual reporting periods Early adoption is permitted for all entities.

5. IAASB: NARROW-SCOPE AMENDMENTS RELATED TO IESBA’S USING THE WORK OF EXPERTS

On January 05, 2026, the International Auditing and Assurance Standards Board issued a narrow-scope amendments to its standards arising from the International Ethics Standards Board for Accountants’ (IESBA) Using the Work of an External Expert project.

The following standards stands amended:

- ISA 620 – Using the work of an auditor’s expert

- ISRE 2400 (Revised) – Engagements to Review Historical Financial Statements

- ISAE 3000 (Revised) – Assurance Engagements Other than Audits or Reviews of Historical Financial Information

- ISRS 4400 (Revised) – Agreed-upon procedures engagements

The amends relates to ethical requirements include provisions related to using the work of an expert, evaluation of competence, capabilities and objectivity of the expert, Prohibition on using the work of an expert if necessary competence or capabilities is not possessed or if no such evaluation is possible.

6. FRC: THEMATIC REVIEW: REPORTING BY THE UK’S SMALLER LISTED COMPANIES

The Financial Reporting Council, to support a high quality of reporting by the UK’s smaller listed companies and by doing so enhance investor confidence in the said companies, issued operational insights in its “Thematic Review: Reporting by the UK’s smaller listed companies”. The review is based on 20 companies with year-ends between September 2024 and April 2025 operating in a range of market sectors listed outside of the FTSE 350.

The publication highlight improvement in the following areas:

- Revenue: An accounting policy on revenue recognition for all material revenue streams should be aptly disclosed and should be consistent with the company’s business model. Explanations relating to the timing of satisfaction of performance obligations, determination of the transaction price, agent versus principal considerations, and the associated judgements should also be aptly disclosed as a part of the accounting policy.

- Cash flow statements: A clear explanation of specific transactions and the rationale for the classification of such items as operating, investing and financing activities should be provided. Consistency between the amount in the cashflow and other information must be ensured.

- Impairment of non-financial assets: Disclosure relating to the impairment reviews of non-financial assets, significant judgements and estimates, key assumptions and sensitivity analysis.

- Financial instruments: Company specific accounting policies for more complex financial instruments including initial classification and subsequent measurement should be disclosed.

B. GLOBAL REGULATORS – ENFORCEMENT ACTIONS AND INSPECTION REPORTS

1. THE FINANCIAL REPORTING COUNCIL, UK

a) Sanctions against KPMG LLP and Anthony Sykes

The Financial Reporting Council (FRC) in relation to serious breaches of the International Standards on Auditing (ISAs) in the statutory audit of the financial statements of N Brown Group plc (N Brown) for the financial year ended 26 February 2022 (FY22) by KPMG LLP (KPMG), imposed sanctions against KPMG and the concern Audit Engagement Partner in the Final Settlement Decision Notice (FSDN) under the Audit Enforcement Procedure.

KPMG and the concern Audit Engagement Partner have admitted to these breaches of the International Standards on Auditing (ISAs) in the audit work performed on impairment of non-current assets.

As per the International Accounting Standard 36 (IAS 36) a non-current asset should be tested for impairment if there are indications that the carrying value is more than the highest amount to be recovered through its use or sale by the company. The Auditors are required to determine if these impairment testing are performed in accordance with the standards. Impairment testing helps reflect accurate picture of the company’s financial position, ensuring that the company’s assets are not overstated.

N Brown is one of the UK’s largest online clothing and footwear retailers and at the relevant time was listed on the Alternative Investment Market of the London Stock Exchange. In FY 2022, there was indication of impairment, as the group’s market capitalisation was substantially lower than its net assets. The audit team identified impairment of non-current assets as a significant risk and key audit area for the audit.

The breaches in the audit performed with respect to IAS 36 is as under:

- Carrying value of the cash generating unit (CGU).

- Impairment model methodology.

- Cash flow forecasts.

- Discount rate.

- Sensitivity analysis.

- Reconciliation to market capitalisation

- The audit’s team’s overall conclusions.

Even after the breaches mentioned above, the FSDN has not questioned the truth or fairness of the FY 2022 financial statements. Although the inadequate audit work on impairment led to an overstatement of headroom (being the difference between the recoverable amount and carrying value), it has not been alleged that N Brown should have recognised an impairment in FY 2022.

B) FRC IMPOSES SANCTIONS AGAINST BDO LLP AND TWO AUDIT ENGAGEMENT PARTNERS

The FRC, in relation to misconduct by BDO LLP (BDO) and two former audit engagement partners, has imposed sanctions under the Accountancy Scheme against the BDO and its former partners.

The sanctions were imposed following a formal complaint against the respondents in April 2025, which led to an investigation into their conduct under the given circumstances.

In the investigation it was found that a Senior Manager was able to pursue, undetected, a dishonest course of conduct on numerous audits between 2015 and 2019, which included: creating false audit evidence, causing auditor’s reports to be issued without approval from the relevant audit engagement partner, and inserting electronic copies of the audit engagement partners’ signatures in auditor’s reports without their approval.

The outcome of the investigation into the Senior Manager, which provides further details of their Misconduct and the sanctions imposed, was published in November 2024.

The misconduct found in the investigation in the present case is as under:

- BDO’s inadequate response to internal reports which raised or should have raised concerns as to the Senior Manager’s honesty and integrity.

- Deficiencies in BDO’s systems and controls for ensuring adequate audit supervision by engagement partners, and audit quality in the period 2012-2019.

- The failure of the one of the former partners (in the period 2014 – 2019) and the other former partners (in the period 2015 – 2019) to adequately supervise, monitor and oversee 21 and 13 audits respectively, on which the Senior Manager worked, which resulted in each case in an Auditor’s Report being issued without their authority and, in some cases, where inadequate, or no, audit evidence had been obtained.

- One of the partner’s issuance of 10 Auditor’s Reports (for financial years ending between 2015-2018) in relation to audits on which the Senior Manager worked, when insufficient audit evidence had been obtained and where it is inferred that he had carried out no, or very limited, review of such evidence (if any) as had been obtained.

- BDO’s liability for the Misconduct of the Senior Manager and the former partners.

2. THE PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD (PCAOB)

a) PCAOB Sanctions Audit Firm, an Owner of That Firm, and a Former Audit Manager for Multiple Violations of PCAOB Rules and Standards

On January 13, 2026, The PCAOB, in the case involving violations of PCAOB rules and auditing standards in connection with the integrated audit of a public company – Genie Energy Ltd. (“Genie”) – for the year ended December 31, 2022, announced an order sanctioning to Zwick CPA, PLLC(“Firm”), Jack Zwick (“Zwick”) and (2) Jeffrey Hoskow (“Hoskow”).

Violations Found By the PCAOB

- Failure to properly plan, identify, and assess the risks of material misstatement.

- Failure to obtain sufficient appropriate audit evidence to support the Firm’s opinion on internal control over financial reporting.

- Failure to obtain sufficient appropriate audit evidence as to Genie’s reported revenue and unbilled revenue.

- Failure to properly supervise the work of the Firm’s engagement team members.

- Failure to prepare audit documentation pursuant to PCAOB standards.

b) PCAOB Sanctions U.S. Audit Firm for Violations Related to Communications Between Predecessor and Successor Auditors

On September 23, 2025, The PCAOB, in the case involving violations of PCAOB rules and auditing standards in connection with its transfer of draft workpapers to the Successor Auditors, announced an order sanctioning to Marcum Asia CPAs, LLP, a New York-headquartered firm formerly known as Marcum Bernstein & Pinchuk LLP (“Marcum BP”).

Violations Found By the PCAOB

- Failure to adhere to the PCAOB rules and auditing standards relating to transfer of draft workpapers to the Successor Auditor.

- Failure to reach an understanding with the successor auditor as to the use of the draft workpapers, in violation of under AS 2610, “Initial Audits -Communications Between Predecessor and Successor Auditors.”

Due to above violations, the successor auditor improperly used the draft workpapers in its audits and issued an unqualified audit report on the Company’s financial statements for the fiscal year 2015 till 2017. This conduct was the subject of a November 2023 PCAOB enforcement settlement.

c) PCAOB Sanctions Former Audit Partner for Multiple Violations of PCAOB Rules and Standards

On October 25, 2025, The PCAOB, in case of multiple violations of its rules and standards, announced an order imposing sanctions on a former partner in the Lima, Peru, office of Tanaka, Valdivia, Arribas & Asociados Sociedad Civil de Responsabilidad Limitada (“EY Peru”).

The former partner was the partner responsible for EY Peru’s full scope component audit (for the year ended December 31, 2020) of Gilat Networks Peru S.A. (“GNP”), a Latin American subsidiary of an Israel-based provider of satellite-based broadband communications.

Violations Found By the PCAOB

The PCAOB found that during the GNP audit work, the former partner:

- Violated its rules and standards in evaluating GNP’s revenue recognition, an identified fraud risk;

- Failure to appropriately supervise the GNP engagement team; and

- Failure to prepare audit documentation pursuant to PCAOB standards.

d) Deficiencies in Firm Inspection Reports:

K G Somani & Co. LLP

The Public Company Accounting Oversight Board (PCAOB) has issued a report detailing significant deficiencies in the audits conducted by K G Somani & Co. LLP. These deficiencies, which span various aspects of the firm’s audit practices, have raised serious concerns regarding the quality of their audits, compliance with PCAOB rules, and audit independence. Below is an overview of the key findings from the PCAOB inspection report, categorized into several critical areas:

1) Audits with Unsupported Opinions

One of the most concerning findings in the PCAOB inspection report is the firm’s failure to obtain sufficient appropriate audit evidence to support its audit opinions, particularly regarding the financial statements and Internal Control Over Financial Reporting (ICFR). Specific deficiencies identified in this area include:

Issuer A (Information Technology):

- Revenue, Accounts Receivable, Cash, Goodwill, and Intangible Assets: The firm did not perform adequate testing of these key areas, including revenue recognition and the valuation of goodwill and intangible assets.

- Inadequate Testing of Revenue Transactions: The firm failed to adequately test revenue transactions to ensure they were correctly recorded in accordance with accounting standards.

- Failure to Evaluate Key Controls: The audit did not adequately assess controls over critical areas such as journal entries or accounts receivable, which could have flagged material misstatements.

- Insufficient Fraud Risk Assessment: The firm did not perform sufficient procedures related to journal entries, which could indicate potential fraud. This failure led to an incomplete evaluation of the fraud risks inherent in the audit.

The deficiencies in obtaining sufficient evidence for these areas have resulted in unsupported audit opinions on the financial statements and ICFR of Issuer A. This raises concerns about the accuracy of the firm’s audit conclusions and whether the financial statements provided to stakeholders were truly reliable.

2) Other Instances of Non-Compliance

The inspection also identified several other areas where the firm did not comply with PCAOB standards, further compromising the reliability of their audits. These non-compliance issues include:

- Journal Entries: The firm did not perform sufficient procedures to ensure that the population of journal entries was complete when testing for possible material misstatements due to fraud, as outlined in AS 1105. This lack of thorough testing increases the risk of overlooking fraudulent activity in the audit.

- Audit Independence: The firm failed to properly assess the compliance of audit participants with independence requirements, as mandated by AS 2101. This represents a violation of critical PCAOB standards and raises concerns about the objectivity and integrity of the audit process.

- Risk Identification: The firm did not adequately inquire with the audit committee and the internal audit function about material misstatement risks, including fraud risks, as required under AS 2110. This failure in communication could have led to an incomplete or inaccurate risk assessment for the audit.

- Internal Control Reports: The firm’s internal control report was deficient, as it failed to reference the financial statements for all years included in the Form 10-K, violating AS 2201. This omission raises concerns about the completeness and accuracy of the firm’s reporting on the effectiveness of internal controls over financial reporting.

3) Independence Issues

The inspection report also identified concerns regarding the firm’s audit independence, an area of particular importance for maintaining the integrity of the audit process. Specifically, the firm may have violated SEC and PCAOB rules regarding audit independence. An indemnification agreement between the audit client and the firm impaired the auditor’s independence, violating Rule 2-01(b) of Regulation S-X.

4) Quality Control

While no major criticisms were found regarding the firm’s quality control system, the PCAOB inspection raised concerns about the effectiveness of monitoring activities within the firm. These concerns suggest that there may be gaps in ensuring that audit procedures consistently align with PCAOB standards across all audits, which could increase the risk of non-compliance in future audits.

The deficiencies identified in the PCAOB inspection report reflect significant gaps in K G Somani & Co. LLP’s audit processes, especially in their testing procedures, risk assessments, and compliance with independence rules. The firm’s inability to test key areas adequately, such as revenue recognition, journal entries, and internal controls, may have led to inaccurate or unsupported opinions on the financial statements and ICFR of its clients. These findings underscore the critical need for corrective action to bring the firm’s audit practices into compliance with PCAOB standards.

Additionally, the potential breach of independence requirements due to the indemnification agreement with the audit client needs to be urgently addressed. The firm must also take steps to improve its internal quality control processes to prevent future instances of non-compliance.

The PCAOB has set a 12-month period for the firm to address these deficiencies. Failure to do so will result in public disclosure of any unresolved issues. The firm’s response to the PCAOB draft inspection report will be evaluated to ensure that the necessary corrective actions are taken to comply with PCAOB standards and maintain the integrity of its audits.

3. THE SECURITIES EXCHANGE COMMISSION (SEC)

a) SEC Charges ADM and Three Former Executives with Accounting and Disclosure Fraud

On January 27, 2026, The SEC in the matter of materially inflating the performance of one of the key segments i.e. Nutrition segment of Archer-Daniels-Midland Company (ADM) filed the following:

- Charges against ADM and two former executives.

- Litigated action against one of its former executives.

As per SEC, the said segment was one that ADM highlighted to its investors as an important driver of the company’s overall growth.

The SEC further highlighted the role of the former executives in directing the ‘adjustments’ to Nutrition segment with other segments of ADM to offset the falling targets in the Nutrition segment in fiscal year 2021 and 2022. These adjustments included retrospective rebates and price change between the Nutrition and Other segment which were not available to other customers thereby passing on the operating profit to Nutrition segment. These transactions thus helped ADM and the executives to show that the Nutrition segment has achieved the desired operating profit of 15% to 20% as promised by the executives to the investors.

The order finds that the above adjustments in annual and quarterly reports of ADM led to false and were misleading as these transactions were inconsistent with the representations by the ADM that intersegment transactions were recorded at amounts “approximating market”.

The former executives of ADM were charged with violating the antifraud provisions of the federal securities laws, reporting, books and records, and internal accounting control provisions of the federal securities laws in case of all the concern executives and aiding and abetting ADM’s violations of the antifraud and failing to reimburse ADM for certain executive compensation as required in case of one of the executive.

The following penal charges are levied:

- ADM – civil penalty of $40,000,000

- Executive 1 – Disgorgement and prejudgment interest – $404,343, Civil penalty of $125,000, three-year officer and director bar.

- Executive 2 – Disgorgement and prejudgment interest – $575,610 and Civil penalty of $75,000

- Executive 3 – Permanent injunctions, an officer and director bar, disgorgement of ill-gotten gains with prejudgment interest, civil penalties, and reimbursement of certain executive compensation to ADM pursuant to the Sarbanes-Oxley Act.