BACKGROUND

The audit profession is as old as civilisation itself, but its relevance is being questioned today, perhaps more strongly than ever before. This article is an attempt to identify the root causes for the erosion of confidence in the audit function and actions required to transform this profession particularly in the context of India’s growth and the aspiration of the Indian Auditing Profession to be the world leader.

Having been part of the audit profession for over four decades my views may be somewhat biased in favor of the profession though I have tried to be impartial in my assessment of the state of the profession and the actions required to transform the audit function.

Auditing limited companies, made mandatory around a hundred years before, was always a check on the so-called ‘principal/agent problem’ inherent in the corporate form of business. As Adam Smith once pointed out, “managers of other people’s money could not be trusted to be as prudent with it as they were with their own”.

After more than seven decades of statutory recognition in India, the auditing profession is in the twilight zone transitioning from one era to another. There is a general feeling of concern, angst and helplessness. Critics of the profession believe there has been a significant delay, while hardcore loyalists passionately believe that its past glory is intact, if not enhanced and spoken glowingly about the profession’s contribution to nation building. The loyalists allege that a lot of criticism (including from its members) is biased and incorrect. I personally believe the condition of the audit profession world over and in our country is not as bad as the critics point it, nor is it as sparkling as loyalists profess it to be.

Whatever be the reality, it is time for introspection and taking corrective steps to make the audit function “fit for the future”. To determine the appropriate steps, we begin by:

- Understanding the present situation, i.e., the current state

- Analysing the trends, challenges, headwinds and tailwinds, and

- Evaluating and considering the impact of external and internal factors.

CURRENT STATE

Ever since the dawn of the 21st century, the world has been plagued by several corporate failures, from Enron, Worldcom, etc., to the more recent Carillion in UK and Wirecard in Germany. In many of these, there are allegations of governance failures, frauds and audit failures.

Closer home in our country, too, we have witnessed failures and frauds in financial services entities and other companies in the business of technology, steel, jewellery, real estate, construction, etc.

Whilst laying the blame at the feet of the audit profession for what could be business failures and not necessarily audit failures may be inappropriate, it cannot be denied that in some cases, the auditors have failed to detect large craters in the balance sheet and not just holes in the balance sheet. A senior Indian Government official rightly remarked: “we don’t expect auditors to find a needle in a haystack, but surely their duty extends to finding the elephant in the room!”

Some concerns arising out of these failures are:

- World’s most prominent companies with the best systems, reputed auditors, high profile boards collapsing suddenly overnight under the weight of shoddy accounting and auditing with no warning signals

- Poor corporate governance

- Savings and retirement plans evaporating – in many cases, overnight

- Investors experiencing complete erosion of the value of their investments

- Erosion of credibility of oversight and enforcement actions

- Auditors missing glaring signs

Tim Steer, in his book titled “The Signs Were There” states “….the dives in share prices and the company disasters that resulted in bankruptcy could have been predicted by a little more than a browse through the annual reports if you know where to look….the warning signs are regularly there in the form of accounting shenanigans or other clear signs that the business is changing direction for the worse, or that excellent results are being reported only because of one-off and non-recurring items. Often these red flags are either not seen or are ignored by investors and other stakeholders.

Tim Steer further states in the context of the failure of Carillion in the UK, “the collapse in January 2018 of Carillion, which had received enormous amounts of public money as one of the UK government’s favourite construction and support service companies, is just one in a long line of corporate disasters where even a cursory look at the balance sheet by anyone with a smattering of financial training would have evoked a feeling of dejavu and the realisation that the company was heading for a fall”.

In his Review Report on quality and effectiveness of audit, Sir Donald Brydon stated: “The quality and effectiveness of audit has become an increasingly contested issue …….Audit is not broken, but it has lost its way and all the actors in the audit process bear some measure of responsibility.

Regulators, too, have expressed similar sentiments. These statements correctly reflect the state of the auditing function in India and the rest of the world.

What are the causes? What should be done to fix it? What is the future? I will deal with these later in the article, as we must first also consider the trends, challenges, headwinds and tailwinds, if any, impacting the audit function.

TRENDS, CHALLENGES AND HEADWINDS

The future of auditing, if done the way it is presently, is indeed bleak, given the developments in technology and other changes in regulations, headwinds, etc. The audit function was designed in another century. Built to last, as the saying goes. It was not built to withstand rapid, radical change. A twentieth-century system cannot function forever and effectively in the 21st century.

So what is the conclusion? Has our audit function, which I was a part of for over four decades, suddenly decayed or have the audit professionals become cowboys or toxic? The answer is a firm ‘NO’. We are transitioning from another era and are undergoing the labor pains of a new birth. It will involve a lot of transformation effort with changes in mindset, skillset and toolset.

No one can predict the future. We are not soothsayers. Of course, one thing is certain and that is “change”. We can no longer function as in 1949 or in the way we have been doing so far. Disruption of the audit function is a certainty. It is not about ‘whether’, but ‘when’. Unfortunately, it can happen faster than we can expect or anticipate as it is not just ‘change’ which is happening but “exponential change”.

The Auditing profession is in a remarkable state of flux. In less than two decades, the way in which audit professionals work and what they will do will change radically. We saw auditors adapt during the pandemic, which for the first time demolished many myths. We are already witnessing many challenges, some of which we never imagined would happen after 73 years. Some examples are:

- Disappearance of branch audits

- Remote physical verification

- Same services being provided by other professionals

- Moves to eliminate audits of smaller entities

- Audits of sustainability reports and integrated reporting

Although everyone would be impacted, the unfortunate part is that the changes will impact the audit function earliest.

Even if we cannot predict the future, we need to be able to observe, understand trends, read the tea leaves correctly and smell the coffee brewing. No purpose will be served by criticizing or ignoring or resisting some of the developments. We need to understand the principles which are driving them.

As the saying goes, “We cannot direct the wind, but we can adjust the sails”

Some of the drivers of this change are:

- Technology

- Liberalisation

- Exclusivity

- Convergence

- Corporatisation of professions

I will briefly explain each of these.

Technology

We are told the average desktop computer will have the same processing power as the human brain which neuroscientists tell us is 1016 calculations per second.

By 2050, according to Ray Kurzweil, the average desktop machine will have more processing power than all of humanity combined.

Technology is growing exponentially in that it more than doubles in power while dropping in price on a regular basis. Moore’s Law is a classic example.

The developments in storage, speed of processing, connectivity, IOT, Big Data, Analytics, Robotics, Artificial Intelligence, etc. will undoubtedly disrupt what services are required, how services will be rendered, who will deliver the services, where services will be rendered and how services will be priced. The audit function cannot be immune to the disruption and will need to transform and adapt if it has to remain relevant and effective.

Liberalisation

As our country continues to liberalise and dismantle bottlenecks in doing business, we will witness decreases in attest requirements and more reliance on self-certification. The audit profession cannot seek legislations which are akin to ‘employment guarantee programmes’. The profession should earn its existence by creating a compelling need for audit services and delivering quality similar to other businesses or professions that have more number of persons dependant and operate in highly competitive environments where price, value and quality of service are some of the criteria which determines who succeeds.

Exclusivity

Alongside liberalisation we will witness actions to eliminate monopolies and eliminate exclusivity. This will further be facilitated by developments in technology which obviate the need for dependence on external professionals but will also shape environments functioning on sophisticated technologies where the traditional professional trained in a significantly manual environment would become extinct. If audit continues to be a relevant function and is expected to use technology and operate in complex technology environments designed by tech professionals questions would be asked as to why technology companies which designed such systems should not be eligible to audit those systems with the help of “techies” and other professionals proficient in accounting. After all, audit is about verifying data, exercising judgements and drawing conclusions. We may not wish that this happens but audit professionals who, perhaps, number 150,000+ in a population of 1.4 billion should justify their exclusivity to provide audit services.

Convergence

Increasingly we are witnessing a thirst for bundled services like a departmental store or a shopping centre. We have already discussed the impact of technology on the audit function and if we consider the increasing need for involvement of specialists in forensic, tax, valuations, technology, etc. in rendering audit services will mean that audit service providers will not only have to partner with other service providers but perhaps will have to house those skill sets under their roof. What will then be the identity of the audit firm? What changes are required in the regulations?

Corporatisation of professions

We have seen how audit services cannot be provided without the involvement of other service providers and the rapidly changing identity of an audit firm. Further, the need to invest in technology to render audit services and to house the specialists who will be involved will require huge investments. When I began my career more than four decades ago, the audit partner who attested the financial statements was a well-versed individual who was not only a specialist in audit but in corporate laws, taxation, valuation, etc. and there seldom was a need for involving anybody else. The changes we

are witnessing in other professions, for example, the medical profession where the delivery of medical services has shifted from individuals to multi-speciality institutions, and the investment required in building state-of-the-art facilities has resulted in the creation of a corporate form of organisations with the investors/financiers not being exclusively from the medical profession. The audit profession needs to introspect about this and seriously consider allowing financial and other strategic partners in audit firms.

FUTURE OF AUDIT: THE ESSENTIAL BUILDING BLOCKS

Let us come back to what needs to be done. We need to address and change:

- The why and what of audit

- Who does the audit

- How audit is done and, finally

- The output of the audit

We will need to address the perception of audit quality as well as the substance of audit quality

To succeed in this, we must:

- Be willing to accept the present state instead of being in a denial mode.

- Introspect and identify the root causes.

- Identify possible actions with a clearly visualised end.

- Be willing to transform (which is the most difficult of all) and, above all,

- Develop the ability to implement and swiftly embrace change.

I would classify my suggestions into seven buckets or silos:

- Purpose

- Structural factors

- Environmental factors

- Execution of audit

- Output factors

- Oversight and evaluation

- Other factors – frequency, timelines, fees, etc.

Purpose

Too long has the audit profession taken shelter behind the words “True and Fair” and the auditing standards which it wrote for itself and about which the users have little knowledge or care about. Any extra “asks” by the users have been rebuffed and rationalized as “Expectation Gap”.

If this rationalisation were to continue the ‘gap’ would widen and the audit profession and its users would be so far apart that audit services would become unnecessary and irrelevant. If the users’ expectation is that audit should address fraud, the profession must take appropriate steps to incorporate this in their audit approach. If the users’ expectation is that the audit should provide some form of assurance of the continuance of the entity in future, the auditor (who is the expert) should be willing to advance a few steps in this direction to meet the expectation.

Sir Donald Brydon, in his Review Report states: “the purpose of an audit is to help establish and maintain deserved confidence in a company, in its directors and in the information for which they have responsibility to report, including the financial statements”.

Our honourable Prime Minister, Shri Narendra Modi, in November 2019, said: “We must challenge the frauds. Both internal and external auditors need to find innovative methods to catch frauds. We need to encourage the core values of auditors for the same”.

Clearly, there is a case for revisiting the purpose of the audit. The sooner the profession addresses this, the faster it will prevent further erosion of confidence in the audit function.

Root causes

A survey conducted by IFIAR some time ago identified a number of causes for poor quality. Some of these are:

- Failure to maintain/monitor independence.

- Failure to evaluate non-audit services.

- Deficiencies in auditing accounting estimates, internal control testing, audit sampling, revenue recognition, group audits, etc.

- Inadequate training and learning of audit professionals.

- Audit quality is not considered in performance assessment.

- No timely supervision and review.

- Insufficient depth of Engagement Quality Control Review (EQCR).

Inspections by regulators have frequently pointed out the above as root causes of audit failures.

Besides poor audit quality, there is an allegation that the audit profession has put ‘self interest’ above ‘public interest’.

The Building Blocks

The essential building blocks for the transformation of the Audit function are summarised in the table below:

|

Structural Factors

|

Environmental

Factors

|

Execution of Audit

|

|

• Profile of the Profession

• Audit Market Profile

• Choice and Concentration

• Size of the Firms

• Auditor Appointment

• Auditor Compensation

• Auditor Independence

• Multi-disciplinary firms

|

• Corporate Financial Reporting Eco-system

• Internal Audit System

• Independent Directors, Audit Committee,

Boards

• Proxy Advisors, Credit Rating Agencies

• Regulators and Regulations

|

• Responsibility

• Audit Procedures

• Tools & Technology used

• Evaluation of Audit test Results

|

|

Output Factors

|

Oversight & Evaluation

|

Other Factors

|

|

• Mandatory Communication to Audit Committee

• Audit Report

• Form

• Type

• Reporting to Regulator

• Enhancements

• Management Letter

• Group Audit

|

• EQCR

• Evaluation of Auditor’s performance by

Audit Committee

• Inspection of Audit engagements by

Regulators

• Peer Reviews, Quality Review Board reviews,

etc.

|

• Frequency

• Timelines

• Transparency

|

Due to constraints of space, I will deal with some of the elements in the building blocks.w

STRUCTURAL FACTORS

Profile of the Profession and Audit Market profile

Every profession should have a profile consistent with the constituency it serves. Our country’s rapid expansion since liberalisation has created a situation where the audit market profile is inconsistent with the size of businesses and industries. There are a large number of sole proprietorships and very small firms involved in rendering audit service. With increasing complexity and investments required in technology and audit tools, these firms will find it exceedingly difficult to render audit service and pass regulators’ scrutiny of their work. Size enables strength and resilience. There is an urgent need for consolidation.

Choice and Concentration

Although the concentration in the Indian Audit Market is not as high as it is in many countries in the western world, yet it is not low enough to provide clients with a sufficiently wide choice. A number of suggestions have been made to address this, including auditor rotation, joint audits, etc., but these do not solve the problem. Rotation does not solve the problem, for the audits would continue to be rotated within the select few, And in some cases, the rotation would be a disincentive for an audit firm to invest in specialised resources required for a particular industry.

A joint audit is also proposed as a solution to widening professional opportunities and address concentration. In some banks, there are more than six joint auditors. The reality is that this only fragments the audit market and does not build firms of the size required to address concentration. Also, divided responsibility leads to divided accountability and impairs audit quality. If this argument is extended it means that appointing a hundred auditors for a large business would deliver better quality than a single firm carrying out the audit. Imagine if we were to have a law which mandatorily requires joint surgeries (by more than one surgeon) to enhance the quality of the surgeries and also provide opportunities for all practising surgeons!

Auditor appointment and Auditor independence

Appointment of auditors by an independent authority is often promoted as the panacea for the audit failures. This is on the mistaken belief that addressing auditor independence will miraculously enhance audit quality as it proceeds on the assumption that auditors are more likely to be compromised if appointed by the company they audit. If true, this is a sad reflection of the members of the audit profession. I do not believe that the manner of appointments have been the cause for audit failures including the recent failures in India and that we should amend the appointment process merely to deal with a few toxic professionals. In reality, besides independence and absence of nexus with the auditee, audit quality depends on a number of factors including size or the firm, quality and experience of audit professionals, ability to deploy the resources required to do a high-quality audit, audit methodology, auditor’s toolkit, etc.

There have been other proposals like (1) prohibiting auditors from providing non-attest services to their audit clients and (2) requiring audit firms to separate their non-audit businesses to create an “audit only” firm. While there is some merit in the former proposal as the audit firm has the rest of the market to render non-attest services, creating ‘audit only’ firms considerably weakens the audit firm and impairs delivery of quality audits.

Auditor’s compensation

If audits are to be carried out effectively by deploying experienced professionals using state-of-the-art tools and involving specialists then auditors have to be well compensated. Audit fees are presently very low in our country and this is further split into fragments by dividing amongst several joint auditors. Fixing of the audit fees by a regulator is not the solution. Entities vary by size, complexity, geographical spread, level of technology, nature of businesses, etc. and fees cannot be fixed or vary with reference to the results or any component of the financial statements. Equally, the audit profession must recognize that fixing fees on an ‘hourly rate’ model is flawed in a digital age when millions of transactions can be analysed by a mere press of a button using digital tools. Increasingly buyers of audit services will look for ‘value delivered’ rather than pay for the cost of input. Too often we have witnessed auditors seeking fee increases based on cost increases without delivering ‘incremental value’ or making efforts to reduce their input costs by using technology. Unfortunately, audit is not considered a ‘premium’ service and the enthusiasm to pay high fees is limited.

Multi-disciplinary firms

Audit in today’s complex and technology dominated environment requires a multi-disciplinary approach. This would be more efficient if the resources and capabilities are under one roof. The future, in my view, is multi-disciplinary firms and the profession should allow unlimited sharing of resources with non CAs even if it means that the CA firm is dominated or led by a non-CA. The bogey of difficulty in taking action when audit failures happen is often cited as an argument against multi-disciplinary firms whereas regulations can be shaped to take action against erring firms or erring professionals, whatever be their profession.

ENVIRONMENTAL FACTORS

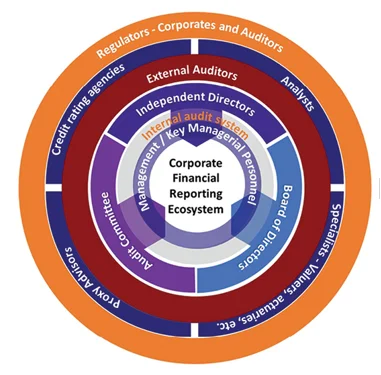

Corporate Financial Reporting and Audit Ecosystem

The audit function cannot alone deliver quality audit. It is influenced and facilitated by the entire Corporate Financial Reporting System. The Financial Reporting and Audit Ecosystem comprise of many participants, each having a very distinct role in ensuring the veracity of financial information and ultimately the efficient functioning of the capital markets. These participants (see graphic below) include:

1. Preparers of financial information – Management, including key managerial personnel

2. Internal monitoring mechanism – internal auditors

3. Corporate governance – audit committee, independent directors, board of directors

4. External auditors

5. Other stakeholders – credit rating agencies, analysts, proxy advisors, specialists such as valuers and actuaries

6. Regulators

7. And last but not least, the users of financial reports – shareholders, lenders, other stakeholders, potential investors, etc.

Any deficiencies in the role played by any one or more of these participants could lead to sub-optimal functioning of the entire ecosystem.

In addition to the components and participants in the financial reporting ecosystem, there are also influences on the financial reporting ecosystem, which have an effect, both positive and negative, as they drive the behaviour of the participants. These, too, need to be reviewed and, if necessary, re-calibrated to produce the desired effect. Some of these are:

- Provisions of various laws which deal with the roles, responsibilities and accountability of the participants in the ecosystem.

- Penalty and prosecution provisions in the various laws.

- Role and process of investigative agencies.

- Multiplicity and overlapping investigative/regulatory agencies.

- Whistleblower mechanisms.

- Standards – accounting standards, auditing standards, secretarial standards, internal audit standards, etc.

Internal Audit System

The internal audit function plays an important role in assisting the board in providing assurance on the effectiveness and efficiency of the risk management, internal control and governance process in the company. It also plays a complementary role in facilitating external audit quality.

In order to improve the internal audit function:

- Internal audit should be subject to regulation and oversight just as the statutory audit.

- Minimum qualifications for the internal auditor should be prescribed, including membership of a professional body or the Institute of Internal Auditors.

- Internal auditors, too, should be accountable for their work.

- Education and training needs of internal auditors should be addressed, including continuing professional education requirements, as well as focus on skills of the future.

Other environmental factors

Some of the other suggestions to improve the reporting environment and supporting the audit function are discussed below:

CEOs and CFOs play a very critical role in financial reporting. Not only are they signatories to the financial system, but also acknowledge and confirm their responsibility for the financial statements being free of fraud and error. They are, in effect, the architects of all business transactions and reporting. Currently, there are term limits and rotation requirements for external auditors and Independent Directors but no term limits for internal auditors, CEOs and CFOs. We must critically examine if term limits and reappointment rules should be extended to these individuals too.

MCA, SEBI or NFRA should set up a data science department that will focus its efforts on the review of the financial statements and filings to detect reporting, disclosure and audit failures. The principal goal of the department should be the detection and prosecution of violations involving false or misleading financial statements and disclosures. The department should also focus on identifying and exploring areas susceptible to fraudulent financial reporting and should include the ongoing review of financial information and the use of data analytics.

A practical public document should be brought out detailing the various deficiencies, frauds, and misstatements noticed by ROC, SFIO, NFRA, etc. This would help corporates, auditors, regulators and other users.

EXECUTION OF AUDIT

Let me first begin with ‘who’ does the audit as audit quality is also influenced by who performs the audit. I believe the current model is flawed.Audit procedures are significantly carried out by trainees or fresh graduates. To expect them to discover frauds or interpret visible signals of misreporting or failure is similar to a medical student carrying out a surgery and the busy eminent surgeon coming in at the end when the sutures are to be done. Our experienced and qualified auditors spend disproportionately less time compared to that of trainees either because they are too busy or that spending more hours increases the cost of audit and erodes audit profitability. A first step towards correcting this is to ensure that articleship with specific focus on specialisation should begin only after passing the CA exam.

Having briefly dealt with who does the audit, I will touch upon the “how” of audit.

The audit has, over the years, moved away from a “thinking audit” to an “inking audit”. The focus has shifted to documenting the processes rather than effectively carrying out the processes.

Auditors seem to have lost their sense of smell. The focus on testing and reliance on internal controls through walk-throughs, etc., has diluted the effectiveness of audit. There is more emphasis on the correctness of the accounting and the disclosures rather than the propriety and genuineness of the transactions. With this and the sampling methods where a speck of the entire population is tested to form conclusions, the auditors seem to be losing their sight or vision too. Sampling methods, howsoever scientific, dilute audit quality. With the use of technology, it is today possible to scan the entire population, focus on outliers, identify questionable patterns, etc. It is time the auditing standard on “Sampling” is revised. It is also time the audit profession uses technology extensively. Additionally, disclosure in the audit report of the sampling methodology used may be considered.

Sir Donald Brydon, in his Review Report, recommended that auditors be required to undergo initial and ongoing periodic training in forensic accounting and fraud awareness. In my view, every audit team should include a forensic specialist.

Yet another issue is the focus of audit. Auditors today are rarely able to walk into a client’s office with an expectation of what they should be seeing. Instead, audit today is about verifying what is presented rather than confirming expectations. I am reminded about the Sherlock Holmes story about “the dog that did not bark”. The analytical review procedures carried out by auditors generally analyse the information presented to them. That too, the focus is on analysing variances beyond certain predetermined thresholds and documenting the reasons. The absence of changes in expenses or income when there should be a change is happily ignored. A case of not probing why “the dog did not bark”!

OUTPUT FACTORS

The Auditor’s Report

I read with interest the dipstick survey carried out by BCAJ in May 2021, seeking views on the format, size, utility, components and other contents of the Statutory Auditors’ Report. I was alarmed and disappointed when 83.6% of auditors responded ‘Yes’ to the question – “In your opinion, will additional reporting requirements prescribed in CARO 2020 be onerous and will increase responsibilities for the auditors (evergreening of loans, going concern, reporting on defaults, etc.)?” Are we so concerned about the increase in responsibilities? Isn’t this what is expected of an auditor? Should we not focus on these matters in our audit and report our findings for the benefit of users, including regulators? It would appear that getting an auditor to do more work to bridge the ‘expectation gap’ is more difficult than getting a tooth extracted by a dentist!Another shocking response to the survey is by 59% of auditors having > 5 years’ experience who responded “Somewhat, but needs improvement” to the question “Do you believe there is adequate, emphatic and clear guidance covering situations for auditors on preparing/issuing Audit Report? This response should have woken up the professional body and resulted in swift corrective action.

I, personally believe, “sunshine is the best disinfectant”. Over the years, I have witnessed the profession resisting any changes to the bland, template-driven audit report. This is strange as the only visible output of the audit to the users is the audit report and if anything can influence the perception of audit quality, it is the audit report. Most audit reports are similar, if not identical, barring minor differences due to the recent inclusion of Key Audit Matters. Does this mean audit quality in all cases is uniform? It is time we brought out into the open the information on what and how the auditor has performed the audit, when the audit commenced, when it ended, the number of hours spent by each category of audit personnel, the number of qualified professionals involved in the audit, the time spent by the audit partner, the use of audit tools, the sampling methodology and the number of items tested, independent external confirmations obtained and the results thereof, experts consulted, errors the auditors found, materiality, etc. rather than the bland statements that the audit has been done in accordance with the auditing standards (written by the auditors themselves only known to and understood by only them)!

Audit reports contain lengthy statements pointing out the roles and responsibilities of management and boards, limitations of the audit and clearly describing the auditor’s responsibility. Has these deterred regulators and investigative agencies? Have auditors been absolved of the blame? Users of audit reports see these cautionary statements with the same disdain as smokers see the statutory warnings in cigarette packs which state “cigarette smoking is injurious to health”!

CONCLUSION

The future of “audit” is bleak, and there are dark clouds on the horizon. I have great respect for the audit profession and sympathy for they are being attacked from all sides – intense competition, unremunerative prices for their services, inability to attract talent to the audit function, demanding clients and society, disruptions due to technology, intense regulatory scrutiny, pursued by multiple investigative agencies for the same work, etc. I am confident that this, too, shall pass but that depends on how the profession addresses some of the matters highlighted in this Article.

The need for a thorough overhaul and transformation is urgent. The issues need to be brought out into the open, for discussion and debate and should not be only within the walls of the Council Hall of ICAI. Wisdom also resides outside the hallowed Council Hall! We cannot forever continue to be in denial mode and hope the present glory (or distrust) would continue. Regulators like NFRA, RBI, SEBI, IRDA, etc. provide a useful role and show us the mirror. We may not like the reflection but let us not throw stones at the mirror. Instead, let us address the image reflected. I have just written a few thoughts in view of space limitations. I have many more thoughts, which are for another time.

We must not attempt any quick fixes or band-aids, or address the issues on piecemeal basis. Code of Ethics, AQMM, UDIN, etc. are some examples of positive actions which are piecemeal and do not move the needle. Such fixes are like changing the dress on a mannequin and hoping it transforms into a live human being!

The future of audit is in our hands only, and I am confident the Audit Profession will reshape itself to be one of the premier professions in our country’s journey to be the third largest economy. We can hardly claim to the partners in nation-building without rebuilding the Audit Profession. Perhaps, what we need is a Review similar to one by Sir Donald Brydon in UK. Let me list some of the questions for debate:

Need for economies of scale – the importance of consolidation of SMPs.

- Declining interest in an accounting career and its effect on the future of auditing.

- Trend of questioning authority by the lay public. Experts are no longer thought to be beyond criticism or scrutiny.

- The rise of NFRA and the end of disciplining by peers – some of NFRA’s orders indicate that the auditors did not know the accounting or auditing standards.

- The days of government-mandated work are over – need to justify the value of work.

- Recent developments in law enforcement e.g., tax fraud, shell companies and rising demands on accountants and auditors.

- How should education change – curriculum, selection of students, exams, training, lifelong learning.

- Audit reports in a language that a reasonably intelligent and earnest user can understand.

- What kind of competition would the audit face?

It is said that people change, not when they see light, but when they feel the heat. I am hopeful my fellow professionals effect the changes swiftly without measuring the transformation action on the ‘popularity’ scale.