The purpose of this article is to present income taxpayer view and some asks. Its cause is some movement in the government about relooking at tax code project more actively. After all, hope of taxpayer cannot be taken or taxed.

Ideally and reasonably, the tax code should mean an enabling force to lead Bharat towards the vision of 2047. For this to happen, taxpayer inputs are critical. Normally taxpayer inputs are taken as a checkbox ticking process. Tax administration does not record reasons for acceptance or rejection of inputs nor communicates anything about them, leave alone reasoning them out. Taxpayer suggestions pass as ‘consultation’, but falls way short of taking the shape of ‘consideration’. Everyone knows that the powerful finally do what they want and what will balance the budget as the obvious and fundamental matters remain off the agenda for decades. At the same time, it will be unfair to ignore work done by this NDA government in last 11 years towards making positive changes.

Nothing in this article that sounds sweeping, is not meant to be so, as there will always be exceptions. The matters in the following paragraphs are based on trends, concept of pre-dominance for the purpose of relevance, emphasis and common sense.

Nation: From Claws to Clauses

The claws of British Raj ended in 1947 and 1950 as we celebrate 75 years of Samvidhaan. The Claws of British ended and a new Rule of Law was envisaged where the nation will run with Clauses that will work for its citizens. The transition is ongoing from the CLAWS of the RAJ to CLAUSES of the STATE and not complete. The legacy system of income taxes is modelled on the Raj. Social Contract (rights, obligations and functions of citizens and government) is still not in place as a diverse country like ours would like. Now we are faced with the magical opportunity to make Bharat glorious for everyone where everyone works towards that common dream. The state obviously is funded by taxes and in that context; the taxpayer is that sub set of the citizenry, which is akin to National Treasure or the precious lot1, that makes a tangible contribution towards making Bharat glorious.

1 Budget Documents of 2024: 19% of Union Budget met by Income taxes

Taxpayer — KarDaataais the real Rashtra Samvardhak

Often the Sarkar takes credit for all development and good news. That is not true largely. Like the AnnaDaata, that is glorified in every political speech (despite them remaining poor and dependent), a taxpayer is the AnnaDaata. She gives nourishment to all schemes, spending, and development through taxes and therefore is a राष्ट्रपोषक, राष्ट्रसंवर्धक, and राष्ट्रकर्तारः. So, taking credit by executive would be like RBI taking credit for every rupee spent or earned since it prints the currency.

The point here is critical: understanding of the KarDaataaas VikasPoshak and should therefore be central to tax laws (by the way, it is not). While many people in the country take to streets, block roads for months, climb on Red Fort and remove tricolour to thrust their demands or protest; the taxpayers who contribute 19 per cent of Union Budget 2024 via income taxes don’t do any of this despite having fair case for a much better treatment. The words of then revenue secretary and now the Reserve Bank of India Governor, Shri Sanjay Malhotra talking to DRI officers pointed out: “We are here not only for revenue, we are here for the whole economy of the country, so if in the process of garnering some small revenue, we are hurting the whole industry or the economy of the country, it is certainly not the intent. Revenue comes in only when there is some income, so we have to be very cautious so that we do not in the process, as they say, kill the golden goose”2

2 https://www.cnbctv18.com/economy/revenue-secretary-sanjay-malhotra-stresses-balanced-approach-to-customs-duty-enforcement-19519098.htm - cnbctv18.com, December 4, 2024

Let’s look at who is this taxpayer?

a) Out of about 140,00,00,000 people of India, 7,54,61,286 individuals file tax returns3.

3 Income Tax Returns Statistics AY 2023-24, Published in June 2024

b) Of the 7.54 Crores individual tax returns, 2,81,61,3614 individual tax returns contributed to ₹6,77,350 Crore as Income Tax Liability5 as declared by them as tax on ₹61,77,988 Crores of GTI or Gross Total Income6. Thus, only 2 per cent of the population in India pays income taxes.

4 Ibid Page 31

5 Ibid Page 6

6 Ibid Page 6

c) Of the above 7.54 Crore people, about 6.92 Crore7 people are in the slab of up to ₹15,00,000 GTI, and declare some 40 Lac Crore as GTI8.

7 Ibid Page 21

8 Ibid page 21

d) During her working life, a taxpayer contributes 5-10-20-30-40 per cent of working life towards this goal excluding indirect taxes and other taxes and levies. How? Because the time spent by her at work, results in earnings, out of that earning, a portion goes as tax. Therefore, she gives on an average 5 per cent to 43 per cent of working life time for the country. That is how Karadaatais Annadataor Vikas Poshak that nourishes the nation.

e) What is a common taxpayer trying to do: He is wanting to come out of poverty / lack and improve his ability to buy for himself and family a life of dignity, comfort, safety and wishes to die without lack and pain.

f) This taxpayer is also “valuable convertible currency” — she can move to other countries and contribute to that country’s development and growth and pay taxes there if the opportunity is better elsewhere. It is well known that Indians are TOP expats anywhere in the world who contribute more and take less from those governments. Richest group in America is of Indian origin — they seek little benefits, they are most educated, they have open outlook, contribute to economy and society in every sphere from taxes to politics.

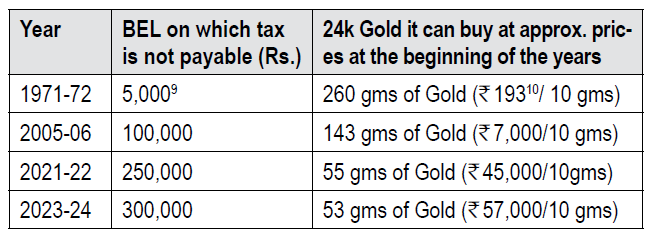

g) What is beating down the taxpayer in achieving his goal: Inflation and tax obligation defeat the citizen’s aspirations given in (e) above. Therefore, one cannot talk of taxes without inflation. Normally one can compare rise in basic exemption limit by comparing it with inflation indices. But for a moment I wish to present the ‘gold standard’ on how even the Basic Exemption Limit (BEL) furthers this beating of taxpayer:

9 Finance Bill, 1971 for FY 2071-72

10 https://www.bankbazaar.com/gold-rate/gold-rate-trend-in-india.html

Analysis:

i) Why Gold: Gold has been historically and presently the store of value for all central banks. Value of currency is not the real value nor is declared inflation true reflection of what currency can do. This comparison tells us that BEL is actually going down instead of up, it hasn’t protected taxpayers, and erodes their ability to save and invest. Even if one were to take, ₹700,000 as that BEL, it is more than 30 per cent lower. The author does understand gold as investment class, however it has been so for millennia.

ii) The Basic Exemption Limit if one wants 143 gms. gold should be ₹10.56 lacs at ₹73,909 / 10 gms gold price on 1st April, 2024.

iii) The table shows that BEL has been beating the hell out of taxpayer, especially those on the edge who are trying to stay afloat to remain in the middle income group.

iv) Similar exercise can be done for upper limit of 30 per cent from which maximum rate applies. It could have the same outcome.

h) A taxpayer tries to race and beat the scourge of inflation eating into his savings by investing in modes like the stock market. However, today LTCGs is taxed at flat rate above ₹1.25 Lacs despite continuation of STT (which was brought in place of exemption of LTCG).

i) Inflation basket: The inflation basket doesn’t take two major expenses of middle income group adequately —housing costs and education cost. For emerging middle-income group, which pays this tax at a level that it bleeds, inflation is not factored by tax system fairly. BEL is not ‘inflation adjusted’.

j) What do you get for being a taxpayer: It must be noted that taxpayer doesn’t get ONE BENEFIT from Sarkar that a non-taxpayer doesn’t get (well we received certificates for 1-2 years). Further the taxpayer is susceptible to come into a ‘harassment net’ in the form of not given tax credit despite tax credit in Form 26AS or sending claims for unpaid taxed that are of 10-15 years old without showing any basis and even adjusting refunds against those so called unpaid demands. In fact, if you are general category, your taxes will be used to deny your children admissions on merit by huge margins to the extent that you pay two to three-times apart from being discriminated on marks. One reason for brain drain.

k) Paying taxes will debar you from every incentive a non-taxpayer enjoys at the expense of the taxpayer.

Therefore, the only response a government with a reasonable mind-set, which can grasp the above, is to protect this taxpayer number, and let it grow organically so that it can contribute more by earning more. Disrupting its earning, taking taxes excessively, being unfair will have adverse results.

Tax Administration — A Business Case

The tax administration consists of unelected people but it carries substantial power. The taxpaying citizens’ ask from tax administration is small and reasonable: have clear to understand and easy to comply tax laws and procedures.

At a structural level, the problem with the tax administration is that an individual administrator has nothing to lose personally for a decision he takes or not take whereas the taxpayer has a large monetary stake. This problem gets bigger by slow, expensive, cumbersome and little recourse to justice.

Typically, administrative system is modelled to self-perpetuate — making more of itself and increase the work and importance for itself. This is despite the bureaucracy often identified with sub-par outcomes, corruption, revenue bias, inability to listen to people it is meant to serve, slow implementation, and low standards of services.

Considering the above facts and facets about the taxpayer, the supreme role of tax administration should be to make lives of taxpayers easy, remove difficulties with pace and not have adversarial attitude. The idea of Sarkar vs. Kardaataa where the previous is chasing the latter is a remnant of the Raj. Yet, Sarkar remains the biggest litigant and from tax litigation its track record at winning at all three levels is far from admirable. Therefore, adversity, except with proven evaders and criminals, should be avoided. It just makes business sense.

The idea of serving the taxpayer where he can earn more and therefore he can in absolute terms pay more tax is genetically and historically missing. Tax laws should be made and presented as enablers.

Taxpayer Asks

The following paragraphs carry some simple ideas. Ideas that can:

a) be implemented without much effort,

b) be disproportionately in favour of benefits while evaluating effort vs. benefits ratio,

c) yield long term and short term benefits to taxpayer and tax collector.

d) makeViksit Bharat Sankalp a reality.

e) be measuring rods to evaluate existing laws and as tools to fix undesirable tax laws and their administration.

I. SIMPLICITY OF DRAFTING

Law is how it reads, just as money is what money can buy. Law need not be simple, but its drafting certainly can be.

Anyone who opens the ITA or Rules can tell that it’s not in English that common taxpayer can read and understand both. It is written in terse, dated, Queen’s English that is already BANNED in many countries11 where Queen / King are still on their currency. Such legal writing is culturally misplaced and at best a remnant of the Raj. US and UK had a Plain English movement12 in 1970s. New Zealand has a Legislation Manual13 on drafting laws in a language that is clear for mortals to decipher. It says: “Drafters must never lose an opportunity to make legislation easier to understand. This is primarily a matter of using plain language and drafting clearly14”. The Legislation Manual prohibits use of certain words that are everywhere in Indian tax laws.

Indian legislative drafting is far from plain English. India is not Bharat so far as legislative drafting of income tax laws is concerned. We are more British than even the present Britain despite the Queen having left 75 years ago and now even the planet. We haven’t won the battle between Authority and Accessibility yet, which such drafting poses. Lawyers and even CAs too, often tend to believe that complexity in writing is a sign of expertise and even genius. While actually it is only a form of barrier to communication and access at best. A recent MIT report15, posted by Elon Musk16 says the same thing and gives causes and means of obfuscating laws through such writing. How are Indian laws written? Well, most Dharma Shashtras, ArthaShashtra — ideas on conduct and economics are written in poetry, with high level of aesthetics.

Clarity can only come when the language is not a barrier, and drafting is for understanding and not casting a spell. Lack of clarity shows lack of understanding and /and certainly lack of adequate care for the reader. About 0.02 per cent people said English was their first language, 6.8 per cent people said it was their second language, and 3.8 per cent said it was their third language as per last census of 2011. If I were the head of drafting team of Law Ministry, I would have them put this framed:

11 Search Plain English movement and Pg45 , Para 158 of NZ Legislation Manual

12 The movement began in the 1970s in the United States and England. It was a response to criticism of the complexity of legal English and the lack of clarity in consumer information

13 https://www.lawcom.govt.nz/assets/Publications/Reports/NZLC-R35.pdf

14 Ibid Para 118, Page 35

15 https://news.mit.edu/2024/mit-study-explains-laws-incomprehensible-writing-style-0819

16 17th December, 2024 on X

Simplicity is the price for Clarity.

Clarity is the pre-requisite of greatness.17

Here is what research, experience and common sense tells us: Sentences longer than 27 to 30 words don’t land on the other side as they should. I tried redrafting such sections and normally found that in most cases there is 30 per cent flab. The short point is that Income Tax Act should be redrafted largely to:

1. Remove long sentences and break them down in shorter sentences about 30 words in length;

2. Remove / Reduce endless web of clauses, sub clause, sub-sub clauses, explanations, provisos, cross references. Remove all obfuscating words and replace them with common sense words;

3. Shorten the entire law of 1000s of pages by 20 to 30 per cent as legalise is akin to cholesterol and visceral fat in the words of a recent report18.

4. Keep the intent, meaning, key words, numbering and flow as it is. The Act should be contemporaneous and can be rearranged where necessary and yet reduced in size.

Is this doable? Very easily. How long should this take? Perhaps 6-12 Months, if one starts with important clauses.

17 Inspired by Da Vinci quote “Simplicity is the ultimate sophistication”

18 https://www.teamleaseregtech.com/reports/jailed-for-doing-business/ - Jailed for Doing Business, 2022

II. CLARITY

Clarity amongst other meanings would be:

– Words are simple and commonly used

– Where needed, words are defined; no undefined key word should be there;

– Words should not be absurd / redundant – Example: Assessment Year. I wonder whether this has any meaning at all except confusing people. You have year of Birth, year of graduation. Take the word “actually incurred” in Sections 10(5), 10(13A), 17(2) Proviso, 35 (2B)/ (5B) and Section 220 explanation;

– Low on repetition within the section of words and phrases and structuring;

– It’s not over the top long with numerous explanations, provisos, further tarnished by multiple amendments – Example: Read Rule 11UA, Rule 2(a) has 101 words in one sentence.

– Keep control of phrases such as “being”. The word Being seeks to change reality. It creates notion and fiction rather than deal with reality. Such subjectivity causes litigation and tax evasion. Ideas of notional rent (a property which can be reasonably let out). Rent is real, it’s not a word or fiction. Law creates a fiction and then creates a charge.

– Keep control over the phrase “as may be prescribed”. This is the passport to endlessly add directions on taxpayers.

Here is an example of Clarity

Original:

“Notwithstanding anything contained herein, a person who knowingly fails to comply with the provisions of this section shall, upon conviction, be liable to a fine not exceeding fifty thousand rupees or imprisonment for a term not exceeding one year, or both.” (41 words)

Clear:

“If someone knowingly violates this section, he may be fined up to ₹50,000, imprisoned for up to one year, or both.” (21 words)

As you will see Clarity and Simplicity are twins. When they play together, the game is unambiguous.

III. CONGRUENCE OF LAWS WITH EASE OF COMPLIANCE

It is a stated State Policy of PM Modi’s government where ease of living and ease of doing business are pillars of everything. However, the laws are not congruent with the state policy.

Example: Size of ITR. A blank PDF ITR 6 is 80 Pages, ITR 3 is 58 pages, ITR 7 is 33 Pages.ITR 2 is 34 Pages. I could not find ease anywhere in those pages.

Why? Because snoop for data which is otherwise available. For example, for small businesses / companies it is asking Financial Statements

details at trial balance line item level. Today the same government has, and I believe government is one in this country:

i) access to GST data — which is invoice level sale and purchase and expenses.

ii) Annual Filing with MCA of every line item of Balance Sheet and Profit and Loss Account.

iii) AIS and TIS give transactions;

iv) There is NSDL CAS Data for Financial Assets which an assessee can offer to share.

It’s hard to understand why ITD cannot use some of this data instead of seeking it again under every regulation and then causing internal mismatch within the ITR or ITR and TAR or even ITR and other data sets / points like customs / GST etc. It seems like a trap set up or a synonym for ‘got you’.

Duplication and Excess is an impediment. It is probably a means of the state to see if the same data comes at 3–4 places. But doesn’t help Ease of Doing Business and Ease of Living.

Action Point

1. Take Company Identification Number (CIN) and MCA filing challan number of small companies in ITR, if filing is done and audited accounts are uploaded there;

2. This can be done post ITR also — like UDIN for TAR — within say 30 days instead of giving huge financial data. This will mean authorising ITD to fetch data from MCA;

3. Same for LLP;

4. Further, there is an option to attach FS for all others where there is no tax audit or only take total assets, total liabilities, Sale, Expenses and Profit figures where there is GST.

5. Today there are many options to reduce excess, duplicity and cumbersome data filling which often are made a cause of mismatch and dispute.

IV. RESTRAINT ON AMENDMENTS AND NOTIFICATIONS

RBI brings out Master Circulars / Master Directions once a year on a fixed day. It consolidates all Circulars and Notifications.

125 Notifications and 18 Circulars are issued till 15th December, 2024 under the Direct Tax Laws. Most Notifications are very specific and irrelevant to most people. Circulars are often Q&A or clarifications. Many seem like announcements. Here is the statistics:

| Calendar Year |

Notifications |

Circulars |

| 2024 (15 Dec) |

125/2024 |

18/2024 |

| 2023 |

106/2023 |

20/2023 |

| 2022 |

128/2022 |

25/2022 |

Wouldn’t it be great to have a Quarterly Notification and Circular giving all that is needed unless its life and death situations — like flood relief institutions etc.? Income Tax Department (ITD) must end piecemeal and haphazard approach, which makes income tax law fragmented, messy, and lying all over the place.

Action Point

a. Bring One Notification per quarter or month

b. Bring One Circular per quarter or month

c. Bring and Annual Master Direction collating all changes of the year — Notifications and Circulars.

d. Eventually review all Circulars and Notifications and withdraw what is already a law or Rule and make collation of Circulars that are applicable from a date onwards.

V. FAIRNESS & TIMELINES

a) Laws tilted in favour of tax department

i. Penalties only on taxpayer, nothing on tax officer for their shortcomings.

ii. Interest charged: 12 per cent, Interest given: 6 per cent. This promotes delay in refunds apart from being unfair. Why should a tax payer pay double interest whereas government will pay 6 per cent for delay? This is unfair and promotes late refunds and also causes working capital problems for taxpayer.

iii. Tax Department should be treated akin to trade credit for MSME. Same laws of repayment should apply as often government causes business downfall due to cash flow crunch.

b) Taxpayers’ Charter and Taxpayer Services should be made a law, at least most of it. This will mean that government is committed to taxpayer and treat them as clients. Taxpayer rights and protections are not in the law, but in taxpayer charter on the wall. Much of the taxpayer service should become part of law and tax officer should be bound to deliver basic services – timely response, not closing queries, closing grievances without confirmation of assessee, escalation available for assessee, and so on. RTI like mechanism where 14 days’ rule will apply to provide data to taxpayer. Power without corresponding responsibility and accountability is lacking in the present law.

c) Approval & Discretion without Time lines: This mechanism is most prone to abuse. We all live within time. Taxpayer has to comply within a timeline. Then why not for tax collector at every stage? Example: Taxpayer services like Section 197 certificate. There cannot be anything that requires permission or application or justice without timeline — Say I have to file an appeal in 60 days, shouldn’t ITD dispose appeal in xxx days?

VI. ARBITRARY UNMOVING MONETARY LIMITS

Arbitrary limits that remain unchanged for years and decades:

a. Section 54E: ₹50 lac permitted investment has remained same since 1st April, 2007.

b. TP Study: International transactions of ₹ One Crore and above need a TP Study. This limit is there since TP law was introduced in 2001.

c. ₹100,000 remained as a limit for exempting LTCG from 2018 till 2024.

d. ₹10 Crore on Capital Gains investment in House Property is arbitrary — no explanation, just a law that if you sell shares and buy a property which was allowed without limit, now will be allowed till ₹10 crores. What if a young citizen was planning and saving to buy a dream house for 20 years, and now he will have to pay tax on the tax paid money I invested.

e. Mediclaim limit, 80C limit of ₹150,000, ₹50,000 Standard Deduction Limit have remained unchanged for years.

f. R100 for school allowance19 — this is not a limit; it is an insult. In fact, higher education allowance is a must for taxpayers. Today general category will pay ₹20 lacs minimum in Deemed Medical colleges per year per child despite getting adequate marks. Is this honouring middle income group?

19 Section 10(14), read with Rule 2BB

VII. CONSISTENCY, SURPRISES AND TURNAROUNDS

Taxpayers want consistency and stability. This is the bedrock of any relationship. One of the main ask is to keep the policy and law consistent.

LTCG

Late FM Arun Jaitley, mentioned that India won’t impose tax on LTCG20. In February 2018 tax imposed on LTCG by Shri Jaitley. But it did not end there, STT wasn’t rolled back. Till November ₹36,000 Crores of STT21 collected in FY 24-25 and also LTCG for FY 2023-24 was ₹36, 867 Crores from Individual ITRs between the range of 150,000 to 15,00,00022.

20 25 December 2016, https://www.business-standard.com/article/reuters/india-won-t-impose-long-term-capital-gains-tax-finance-minister-jaitley-116122500535_1.html

21 https://www.thehindubusinessline.com/markets/stt-collection-hits-36000-crore-reaching-97-of-budget-target-amid-market-rally/article68858203.ece

22 Income Tax Returns Statistics AY 2023-24, Published in June 2024, page 25

This is one recent example of lack of consistency and turnaround.

Budget as a Surprise Genie

Is Budget a magic show, where new changes are released? Much of this can stop. There is zero reason to bring out changes via Budgets without informing people in advance.

Example: Sudden change to limit of ₹10 Crore for property Purchase from sale of Shares.

If someone is in the middle of a transaction or is planning for years to buy a property, his costing changes in a big way. If there was knowledge that such changes are effective, then people can plan better. Such changes are used in the Budget as if they are a trap, as in a war where surprise is an element of ambush. Yes some rate changes etc. which are expected, or minor amendments to make law more efficient. However, taxpayer benefit should be above all and taxpayer needs to know what is coming when it’s a major change.

Imagine if this was known in advance that you have 12 months to sell equity, make gains and buy a house if you need to before 12.5 per cent and ₹10 Crore kicks in. Will it result in homes price inflation? Will there be a sell out in equity? I don’t think so. India is way too large now for such changes rocking the markets.

Example of Turnaround: Adding MAT to Tax Free SEZ Units midway in 10-year time period.

SEZ were exempt from tax as scheme. One fine day MAT on SEZ was introduced. This is breaking a promise. Once an investor has started a project with knowledge that there won’t be taxes, and then taxes creep in, it is breaking the contracts through law. A sovereign right need not be used to disrupt and throw taxpayers under the bus.

Predictability attracts investments as it reduces risk and is the bedrock of Trust.

Finally, taxmen always ask this question: will all these increase tax compliance and revenue? The answer is yes, because this government itself has adopted some simplification measures that resulted in better compliance, more tax, and more taxpayers. Mahabharata says Dharma always wins in the end. It means if one does the right things, the end result will be right.

There is a vision and idea of Amrit Kal. Another article will deal with some of the specific changes that are necessary in tax laws and procedures and affecting most taxpayers. Some of these may be redundancy, absurdity, unclarity, complexity and the like. Amrit only comes from manthan, and income tax law requires true manthan, where Amrit and Laxmi can both emerge for all people of Bharat.

The faculty answered the various queries raised by the members which reflected how deeply the audience got interested on the subject. More than 200 members present gained immensely from the expert deliberation from the faculties. The video of the lecture is available at www.bcasonline.org & www.bcasonline.tv, respectively, for the benefit of all.

The faculty answered the various queries raised by the members which reflected how deeply the audience got interested on the subject. More than 200 members present gained immensely from the expert deliberation from the faculties. The video of the lecture is available at www.bcasonline.org & www.bcasonline.tv, respectively, for the benefit of all.