This article summarises the key

additions/ modifications made in the 2017 Guidelines as compared to the earlier Guidelines. The first part of the

article, published in the December issue of the Journal, discussed about the

general guidance contained in Chapters I to V of the new Transfer Pricing

Guidelines issued in 2017 (2017 Guidelines). This part of the article deals

with guidance relating to specific transactions:

? Chapter VI – Special

Consideration for Intangibles

? Chapter VII – Special

Considerations for Intra-Group

Services,

? Chapter VIII – Cost

Contribution Agreements, and

? Chapter IX – Business

Restructurings

1. Chapter

VI – Special Considerations for Intangibles

The 2017 Guidelines

have broadened the concept of ‘intangibles’ for transfer pricing purposes, and

also provide detailed guidance on intangibles including several aspects of

intangibles not addressed in the earlier guidelines. The key differences are

discussed in this section.

1.1. Definition of

intangibles

The 2017 Guidelines

provide that the word ‘intangible’ is intended to address something which is not

a physical asset or a financial asset, which is capable of being

owned or controlled for use in commercial activities and whose

use or transfer would be compensated had it occurred in a transaction between

independent parties in comparable circumstances.1 The 2017

Guidelines provide that intangibles that are important to consider for transfer

pricing are not always recognised as intangible assets for accounting purposes

and the accounting or legal definitions solely may not be relevant for transfer

pricing.

___________________________

1 Refer para 6.6 of 2017 Guidelines

The 2017 Guidelines discuss that distinctions are sometimes sought to be

made between (a) trade and marketing intangibles2 (b) soft and hard

intangibles (c) routine and non-routine intangibles and between other classes

and categories of intangibles, but the approach to determine arm’s length price

does not depend on such categorisations.3 An illustrative list of

intangibles is also provided in the 2017 Guidelines. The Guidelines also

provide that factors such as group synergies and market specific

characteristics are not intangibles, since they cannot be owned or controlled

by any one entity in the group.

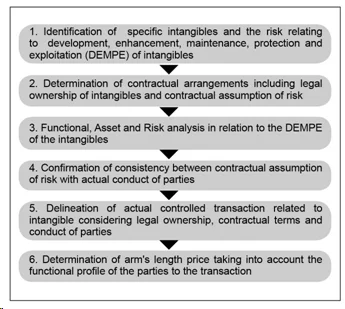

1.2. Framework for transfer

pricing analysis of transactions involving intangibles

Like any other transfer pricing matter, analysis of cases involving

intangibles should be in accordance with principles outlined under Chapter I to

III of the 2017 Guidelines. The Guidelines provide for a similar six-step

framework for analysing transactions involving intangibles.4

________________________________________________

2 Marketing Intangible and Trade Intangible

have also been defined in the 2017 Guidelines.

3 Refer para 6.15 of 2017 Guidelines

4 Refer para 6.34 of 2017 Guidelines

1.3. Intangible ownership and

contractual terms relating to intangibles

The 2017 Guidelines

specifically provide that legal ownership does not necessarily confer the right

to returns generated from the intangible. The Guidelines give an example of an

IP Holding Company which does not perform any relevant functions, does not

employ any relevant assets and does not assume any relevant risks. The

Guidelines provide that such party will be entitled to compensation, if any,

only for holding the title to the IP, and not in the returns otherwise

generated from the IP. The returns from the intangible, even though they accrue

initially to the legal owner of the intangible, will need to correspond to the

functions performed, assets employed and risks assumed by the different

entities in the group.

1.4. Functions, Assets and

Risks relating to Intangibles

1.4.1. Functions

The 2017 Guidelines

provide that determining the party controlling and performing functions

relating to DEMPE of intangibles is one of the key considerations in

determining arm’s length conditions for the controlled transactions.

In case some

functions are outsourced, if the legal owner neither performs nor controls the

outsourced functions relating to the DEMPE of intangible, it would not be

entitled to any ongoing benefit attributable to the outsourced functions.

Depending on the facts, the return for entities performing and controlling such

functions may comprise a share of the total return derived from exploitation of

the intangible.

1.4.2. Assets

The 2017 Guidelines

provide for considering important assets and specifically identify intangibles

used in research, development or marketing, physical assets and funding.

Unlike the earlier

guidelines, there is a detailed discussion in the 2017 Guidelines on funding,

and returns corresponding to funding. The Guidelines provide that funding

returns from intangibles would depend on the precise functions performed and

risks undertaken by the funder. An entity providing funding but not controlling

risks or performing functions relating to the funded activity would be entitled

to lesser returns than an entity which also performs and controls important

functions and controls important risks associated with the funded activity.

In the context of

funding, the Guidelines distinguish between financial risks (risks relating to

funding/ investments) and operational risks (risks relating to operational

activities for which the funding is used). If the investor controls the

financial risk associated with the provision of funding, without the assumption

of operational risks, it could generally expect only a risk-adjusted return on

its investments.

1.4.3. Risks

The 2017 Guidelines

specifically identify risks relating to transactions involving intangibles,

such as risks related to development of intangibles, risk of product

obsolescence, infringement risk, product liability risk, and exploitation risk.5

A detailed analysis of the assumption of these risks with respect to functions

relating to the DEMPE of intangibles is crucial.

The Guidelines also

provide that generally, the responsibility for the consequences of risks

materialising will have a direct correlation to the assumption of risks by the

parties to the transaction.

1.5. Actual (ex post)

Returns

The 2017 Guidelines

also discusses regarding sharing of profit/losses among group entities in case

of variation between actual (ex post) and anticipated (ex ante)

returns.

The 2017 Guidelines

provide that the entitlement of the group entity to the variation depends on

which party assumes the risks identified while delineating the actual

transaction. The entitlement also depends on performance of important functions

or contributing to control of economically significant risks, and for which an

arm’s length remuneration would include a profit-sharing element.

1.6. Illustration on

application of arm’s length principle in certain specific fact patterns

The 2017 Guidelines

identify specific commonly found fact patterns and provide useful guidance on

those and provide detailed guidance on these situations. These are briefly

discussed in this section.

1.6.1. Marketing intangibles

The 2017 Guidelines

discuss a common situation where a related entity performs marketing or sales

functions that benefit the legal owner of the trademark – through marketing

arrangements or distribution/marketing arrangements.6

___________________________

5 Refer para 6.65 of 2017 Guidelines

The Guidelines

provide that such cases require assessment of:

? Obligations

and rights implied by the legal registrations and agreements between the

parties;

? Functions

performed, assets employed and risks assumed by the parties;

? Intangible

value anticipated through the marketer/ distributor’s activities; and

? Compensation

provided to the marketer/distributor.

The Guidelines then

provide that any additional compensation for the marketer/distributor will

arise if it is not already adequately compensated for its functions through the

contractual arrangement.

1.6.2. Research, development and

process improvement arrangements

The 2017 Guidelines

provide that in cases involving contract research and development activities,

compensation on a cost plus modest mark-up basis may not reflect arm’s length

price in all cases. While determining the compensation, the Guidelines give

much weightage to the research team, i.e., including their skills and

experience, risks assumed by them, intangibles used by them, etc. Similarly,

analysis would be required in case of product or process improvements resulting

from the work of a manufacturing service provider.

1.6.3. Payment for use of company name

The 2017 Guidelines

provide that generally, no compensation should be paid to the owner of the

group name for simple recognition of group name, or to reflect the fact of

group membership. A payment would be due only if the use of the group name

provides a financial benefit to the entity using the group name. Similarly,

where an existing successful business is acquired by another business, and the

acquired business begins to use the group name, brand name, trademark, etc., of

the acquirer, there should be no automatic assumption that the acquired

business should start paying for such use of the group name and other

intangibles. In fact, in a case where the acquirer leverages the existing

positioning of the acquired business to expand to new markets, one should

evaluate whether the acquirer should pay a compensation to the acquired

business.

_________________________________

6

Refer para 6.76 of 2017 Guidelines

1.6.4. Other specific cases

The 2017 Guidelines

also provides guidance on various other specific fact patterns involving

intangibles such as transfer of all or limited rights, combination of

intangibles, transfer of intangibles with other business transactions, use of

intangibles in connection with sales of goods/ services.

1.7. Comparability factors

The 2017 Guidelines

provide detailed guidance on comparability factors relating to intangibles.

These factors should be considered in a comparability analysis especially under

the CUP Method (say, benchmarking analysis to find comparable royalty rates for

use of intangibles). The comparability factors specifically mentioned, although

not exhaustive, include exclusivity; extent and duration of legal protection;

geographic scope; useful life; stage of development; rights to enhancements,

revisions and updates; and expectation of future benefit.

Similarly, some key

risks that need to be analysed for a comparability analysis include risks

related to future development of the intangible, product obsolescence and

depreciation, infringement risks, product liability risks, etc.

1.8. Valuation of intangibles

The 2017 Guidelines

tend to favour the CUP Method and the transactional profit split method for

valuing intangibles. The Guidelines also recognise valuation techniques as

useful tools. One-sided methods including RPM and TNMM are generally not

considered reliable for directly valuing intangibles.

Use of cost-based

methods for valuing intangibles have also been largely discouraged, other than

in limited circumstances involving, say, development of intangibles for

internal business operations, especially when such intangibles are not unique

or valuable.

The Guidelines have

provided detailed guidance on the use of Discounted Cash Flow (DCF) Method or

other similar valuation methods for valuing intangibles. Having said that, the

Guidelines also caution that because of the heavy reliance on assumptions and

valuation parameters, all such assumptions and parameters must be appropriately

documented, along with the rationale for using the said assumptions or

parameters. The Guidelines also recommend taxpayers to present a sensitivity

analysis, with alternative assumptions and parameters, as part of their

transfer pricing documentation.

1.8.1. Intangibles having

uncertain valuations

In cases involving

intangibles the valuation of which is highly uncertain at the time of the

transaction, the 2017 Guidelines provide guidance on a much broader concept of

arm’s length behaviour. The Guidelines inter alia provide that in case

the valuation of the intangible is highly uncertain at the time of the

transaction, the parties to the transaction would potentially adopt short-term

agreements, include price-adjustment clauses, adopt a contingent pricing

arrangement, or even renegotiate the terms of the transaction in some cases.

1.8.2. Hard-to-Value Intangibles

(HTVI)

HTVIs include

intangibles for which, at the time of their transfer, (i) no reliable

comparables exist, and (ii) it is difficult to predict their level of success.

The 2017 Guidelines

make an exception regarding the use of ex post results, and provide that

in certain cases involving HTVIs, and subject to certain safeguards and

exemptions, ex post results can be considered as presumptive evidence

about the appropriateness of the ex ante pricing arrangements. The

Guidelines also provide a safe harbour of 20%, within which valuation based on ex

ante circumstances should not be questioned and replaced by valuation based

on ex post results.

2. Chapter

VII – Special Considerations for Intra-Group Services

In the analysis of

transfer pricing for intra-group services, one key issue is whether intra-group

services have in fact been provided, and the other issue is, what is the

intra-group charge for such services under the arm’s length principle. Detailed

guidance has been provided in the 2017 Guidelines on various aspects in the

context of intra-group services such as shareholders’ activities, on call

services, form of remuneration, determination of cost pools, documentation and

reporting, levy on withholding tax on provision of low value-added intra-group

services.

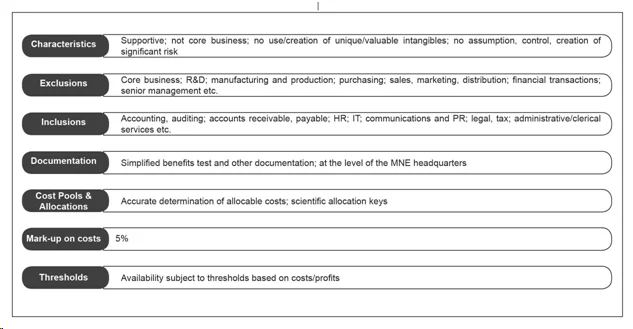

2.1. Low Value Adding

Intra-Group Services

The 2017 Guidelines

recommend an elective, simplified transfer pricing approach relating to

particular category of intra-group services referred to as low value adding

intra-group services. Under this approach, subject to fulfilment of certain

criteria, the arm’s length price of the services would be considered to be

justified without specific benchmarking and detailed documentation of the

benefit test by the recipient.

The guidance

provided in the 2017 Guidelines are summarised below.

3. Chapter

VIII – Cost Contribution Arrangements

The 2017 Guidelines

provide that a Cost Contribution Arrangement (CCA) is a contractual arrangement

among business enterprises to share the contributions and risks involved in the

joint development, production or the obtaining of intangibles, tangible assets

or services, with the understanding that such intangibles, tangible assets or

services are expected to create benefits for the individual businesses of each

of the participants.

Two types of CCAs

are commonly encountered: (1) Joint development, production or the procurement

of intangibles or tangible assets (“Development CCAs”); and (2) Procurement of

services (“services CCAs”).

With regard to

application of arm’s length principle, the general guidance provided in the

2017 Guidelines, including the risk analysis framework, also apply to CCAs. To

apply the arm’s length principle to a CCA, it is therefore a necessary

precondition that all the parties to the arrangement have a reasonable

expectation of benefit. The next step is to calculate the value of each

participant’s contribution to the joint activity, and finally to determine

whether the allocation of CCA contributions (as adjusted for any balancing

payments made among participants) accords with their respective share of

expected benefits.

The Guidelines also

provide that the guidance provided in Chapter VI relating to intangibles and

Chapter VII relating to intra-group services also apply to CCAs, to the extent

relevant.

Further, the

Guidelines provide specific additional guidance in the following areas:

3.1. Participants

A participant must

be assigned an interest or rights in the intangibles, tangible assets or

services that are the subject of the CCA and should have a reasonable

expectation of being able to benefit from that interest or those rights. The

Guidelines discuss in detail regarding determination of participants in CCAs.

3.2. Expected benefits

In determining the

participants’ share of expected benefits, the 2017 Guidelines encourage the use

of relevant allocation keys. The Guidelines also provide that the CCA should

provide for a periodic reassessment of allocation keys. Consequently, the

relevant allocation keys may change over a period of time, and this may lead to

prospective adjustments in the share of expected benefits of the participants.

3.3. Value of Contributions

The 2017 Guidelines

recommend distinguishing between pre-existing contributions and current

contributions for the purpose of valuing them. Any pre-existing contributions

(say, any existing patented technology) should generally be valued at arm’s

length based on the general guidance provided in the 2017 Guidelines, including

the use of valuation techniques. However, any current contributions (say,

ongoing R&D activities) should be valued based on the value of the

functions themselves, rather than the potential value of the future application

of such functions.

3.4. Documentation

The 2017 Guidelines

emphasise that taxpayers should provide detailed documentation relating to CCAs

as a part of the master file. Additionally, the local file should also contain

transactional information including a description of the transactions, amounts

of payments and receipts, identification of the associated enterprises

involved, copies of inter-company agreements, pricing information and

satisfaction of the arm’s length principle. The Guidelines also provide for an

additional disclosure of management and control of CCA activities and the

manner in which any future benefits from the CCA activities are expected to be

exploited.

4. Chapter

IX – Business Restructurings

The 2017 Guidelines

contain an elaborate discussion on transfer pricing aspects of business

restructurings. Business restructuring refers to the cross-border

reorganisation of the commercial or financial relations between associated

enterprises, including the termination or substantial renegotiation of existing

arrangements.

Business

restructurings may often involve the centralisation of intangibles, risks or

functions with profit potential attached to them.

As compared to the

earlier guidelines which included conversion of full-fledged distributors or

manufacturers to low risk ones and also included transfers of intangibles, the

2017 Guidelines also include concentration of functions in a regional or

central entity with corresponding reduction in scope or scale of functions carried

out locally, as a business restructuring transaction.

The Guidelines

address two aspects of a business restructuring – i) arm’s length compensation

for the restructuring itself, and ii) arm’s length pricing of

post-restructuring transactions.

Some key additional

guidance provided in these Guidelines is discussed in this section.

4.1. Arm’s length

compensation for the restructuring itself

4.1.1. Accurate delineation of the

restructuring transaction

The general

guidance relating to arm’s length principle is applicable also for business

restructuring. The 2017 Guidelines recommend performing accurate delineation of

transactions including detailed functional analysis in pre and

post-restructuring scenarios. In doing so, the Guidelines place special emphasis

on the risks transferred as a part of the restructuring, and importantly,

whether such risks are economically significant (i.e., whether they carry

significant profit potential and hence, may explain a significant reallocation

of profit potential).

Like earlier

guidelines, one needs to also analyse the business reasons for and expected

benefits from restructuring, and other options realistically available to the

parties.

4.1.2. Transfer of something of value

The 2017 Guidelines

provide that in case physical assets such as inventories are transferred

between foreign associated enterprises as a part of the restructuring, the

valuation of such assets is likely to be resolved as a part of the overall

terms of the restructuring. In practice, there may also be an inventory rundown

period before the restructuring becomes effective, to mitigate complications

relating to cross-border inventory transfers.

Similarly, in case intangibles

are transferred as a part of the restructuring, the Guidelines provide that the

valuation of such intangibles should be done in line with the guidelines

provided for valuation of intangibles, including guidance provided for valuing

HTVIs (Chapter VI).

In case of transfer

of an activity, the 2017 Guidelines are aligned with the earlier

guidelines and provide that the valuation of such an activity should be done as

a going concern of the entire activity, rather than individual assets.

4.1.3. Indemnification for termination or substantial

renegotiation of existing arrangements

Indemnification

means any type of compensation that may be paid for detriments suffered by the

restructured entity, whether in the form of an up-front payment, of a sharing

in restructuring costs, of lower (or higher) purchase (or sale) prices in the

context of the post-restructuring operations, or in any other form.

The 2017 Guidelines

provide for consideration of the following aspects in this regard:7

? Whether,

based on facts, the commercial law supports the right to indemnification for

the restructured entity

? Whether

the indemnification clause, or its absence, is at arm’s length

? Which

party should bear the indemnification costs

Each of the above

aspects has been discussed in detail in the OECD guidelines.

4.1.4. Documentation

The 2017 Guidelines

provide for documenting important business restructuring transactions in the

master file. Further, in the local file, taxpayers are required to indicate

whether the local entity has been involved in, or affected by, business

restructurings occurring in the past year, along with related details.

4.2. Arm’s Length

compensation for post- restructuring transactions

The 2017

Guidelines, like the earlier guidelines, provide that the arm’s length

principle should apply in the same manner to restructured transactions, as they

apply to transactions which were originally structured as such.

______________________________

7 Refer para 9.79 of 2017 Guidelines

Further, there

could be inter-linkages between the restructuring and the business arrangement

post-restructuring. In these situations, the compensation for the restructuring

and for the subsequent controlled transactions could be potentially dependent

on each other, and may need to be evaluated together from an arm’s length

perspective.

5. Concluding

Remarks

The 2017 Guidelines have addressed some key

challenges faced by taxpayers with respect to the specific

transactions/situations covered in this part of the article. In several

situations, the Guidelines provide for arm’s length behaviour in principle,

considering the overall scheme of things, and not merely evaluating the price

of isolated transactions

In the Indian

context, transfer pricing for transactions involving intangibles appears to be

a significant focus area for Indian tax authorities. Analysis of control of

functions and assumption of risks vis-à-vis provision of funding in

transactions relating to intangibles is extremely pertinent in the Indian

context given India’s leading position as a preferred destination for several

MNCs for intangible creation/upgradation in verticals such as technology,

engineering, pharma, etc.; and also given the huge marketing and promotional

spend incurred by many Indian distributors. The guidance also aligns, in

principle, with the approach of valuing intangible transfers using a DCF

approach, albeit with several safeguards relating to the assumptions and

other parameters used for valuations. Overall, the guidance provided in the

2017 Guidelines is largely being implemented by tax authorities, as evidenced

by the nature of queries and depth of discussions during APAs as well as

transfer pricing audits.

Guidance on low

value adding intra-group services has already been largely implemented in the

Indian safe harbour rules.

The 2017 Guidelines also provide several

examples relating to intangibles and CCAs in Annexes to Chapters VI and VIII,

respectively. Readers are encouraged to study the examples for a better understanding

of these concepts.