Nature of preparatory and auxiliary activities

Article 5(4) enlists a number of business activities which do not constitute a PE, even if the activities are carried out through a fixed place or office. These activities are generally termed as preparatory and auxiliary in nature2. Para 58 of the OECD Commentary (2017) provides that such a place of business may well contribute to the productivity of the enterprise, but the services it performs are so remote from the actual realisation of profits that it is difficult to allocate any profit to the fixed place of business in question.

The Table below classifies the negative list of Article 5(4):

|

As per the earlier OECD

Model Convention, 2014

|

As per BEPS Action Plan

(AP) 7

(Para 78 of the OECD

Commentary, 2017)

|

|

Notwithstanding the

preceding provisions of this Article, the

the term ‘permanent

establishment’ shall be deemed not to include:

a) the use of facilities

solely for the purpose of storage, display or delivery of goods or

merchandise belonging to the enterprise;

b) the maintenance of a

stock of goods or merchandise belonging to the enterprise solely for the

purpose of storage, display or delivery;

c) the maintenance of a

stock of goods or merchandise belonging to the enterprise solely for the

purpose of processing by another enterprise;

d) the maintenance of a

fixed place of business solely for the purpose of purchasing goods or

merchandise or of collecting information, for the enterprise;

e) the maintenance of a

fixed place of business solely for the purpose of carrying on, for the

enterprise, any activity not listed in

sub-paragraphs a) to d), provided that this activity has a preparatory or

auxiliary character;

f) the maintenance of a fixed

place of business solely for any combination of activities mentioned in

sub-paragraphs a) to e), provided that the overall activity of the fixed

place of business resulting from this combination is of a preparatory or

auxiliary character

|

Notwithstanding the preceding provisions of this

Article, the term ‘permanent establishment’ shall be deemed not to

include:

a) the use of facilities

solely for the purpose of storage, display or delivery of goods or

merchandise belonging to the enterprise;

b) the maintenance of a

stock of goods or merchandise belonging to the enterprise solely for the

purpose of storage, display or delivery;

c) the maintenance of a

stock of goods or merchandise belonging to the enterprise solely for the

purpose of processing by another enterprise;

d) the maintenance of a

fixed place of business solely for the purpose of purchasing goods or

merchandise or of collecting information, for the enterprise;

e) the maintenance of a

fixed place of business solely for the purpose of carrying on, for the

enterprise, any other activity of a

preparatory or auxiliary character;

f) the maintenance of a

fixed place of business solely for any combination of activities mentioned in

sub-paragraphs a) to e), provided that the overall activity of the fixed place

of business resulting from this combination is of a preparatory or auxiliary

character,

provided

that such activity or, in the case of sub-paragraph f), the overall activity

of the fixed place of business is of a preparatory or auxiliary character

|

* Highlighted part is amended under BEPS AP 7

As can be observed from the above, initially, OECD was of the view that the enlisted negative activities from Article 5(4)(a) to Article 5(4)(d) of the OECD Model Convention, 2014 would apply automatically to exclude the constitution of a PE, more so considering the erstwhile business models. For example, a non-resident company maintains warehouse facilities solely for the purpose of storage of its goods in the Source State. The delivery of goods would be undertaken through an independent third party in the logistic business. Under the erstwhile PE provisions, the foreign company is not required to substantiate that this activity is auxiliary in nature as the application of Article 5(4)(a) of the OECD Model Convention is automatic. Only Article 5(4)(e) and Article 5(4)(f) subject the specified activities to be of a ‘preparatory and auxiliary character’. In the above example, if a non-resident company maintains a warehouse for storage of finished goods [Article 5(4)(a)] and maintains an office for procurement activities, Article 5(4)(d) and Article 5(4)(f) would apply and the ‘overall activity of the fixed place of business resulting from this combination’ should be of a preparatory or auxiliary character to be exempted from constitution of a PE. In reality, the multinational enterprises (MNEs) have benefited from the automatic application of the enlisted negative activities by ensuring that their fixed place of business solely carries on the enlisted negative activity [Article 5(4)(a) to Article 5(4)(d)].

The Executive Summary of the BEPS Action Report No. 7 (at point 10) states that ‘depending on the circumstances, activities previously considered to be merely preparatory or auxiliary in nature may nowadays correspond to core business activities. In order to ensure that profits derived from core activities performed in a country can be taxed in that country, Article 5(4) is modified to ensure that each of the exceptions included therein is restricted to activities that are otherwise of a “preparatory or auxiliary” character… BEPS concerns related to Article 5(4) also arise from what is typically referred to as the “fragmentation of activities”. Given the ease with which multinational enterprises (MNEs) may alter their structures to obtain tax advantages, it is important to clarify that it is not possible to avoid PE status by fragmenting a cohesive operating business into several small operations in order to argue that each part is merely engaged in preparatory or auxiliary activities that benefit from the exceptions of Article 5(4). The anti-fragmentation rule proposed in [this report] will address these BEPS concerns.’

In order to understand the above in detail, let us consider the following examples:

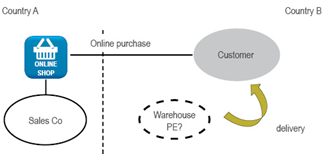

– The above example includes a company operating an online shop in Country A and selling goods to customers in Country B through a website.

– For delivery and storage of goods, the company maintains a warehouse in Country B.

– Erstwhile Article 5(4) included an exception wherein maintenance of a fixed place in India solely for the purpose of storage and delivery would not constitute a PE. This was based on the principle that such activities are considered as preparatory and auxiliary in the entire scheme of business operations.

– However, with the advancement of internet, the manner in which businesses are operated has evolved. Given this, since most of the business operations of the company are undertaken online, maintenance of a warehouse in Country B for storage and delivery may no longer be considered as preparatory and auxiliary in nature but the core activity. This therefore makes the exceptions provided under Article 5(4) redundant.

– BEPS AP 7 / MLI Article 13 seek to address the above challenges and amend the PE provisions to be in line with the advanced business model.

Anti-fragmentation: Splitting for creating preparatory and auxiliary activities

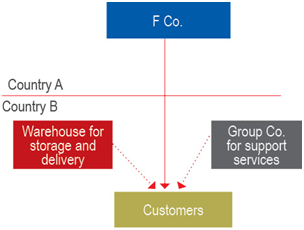

Earlier, the determination of PE and the enlisted negative activities was considered vis-à-vis the said enterprise which carried on such activities, and not that of the group companies assessed in totality. The aggregation of ‘places of business’ carried on by other members of the group companies was specifically denied by the OECD Commentary (2014). So, the MNEs fragmented their business operations into various activities among different places and different related enterprises, with a view to fall within the negative list and avoid the existence of a PE in the Source State. For example, large multinationals can fragment their operations into smaller businesses (such as entity A storing goods, entity B delivering goods and entity C providing sales support activities), thereby arguing that each business part is just preparatory and auxiliary in nature.

MLI Article 13 provides for amendment in the PE provisions to avoid such situations by aggregating the activities provided by group companies in the Source State to determine whether or not a PE is constituted. The following examples can help in understanding fragmentation of activities by foreign companies:

Example 1:

Thus, in the above example F Co. has fragmented its business activities in Country B by incorporating two separate entities undertaking (i) warehouse and storage functions, and (ii) support services.

Example 2:

Paragraph 1 of MLI Article 13

‘A Party may choose to apply paragraph 2 (Option A) or paragraph 3 (Option B) or to apply neither Option’.

The member State may choose to apply paragraph 2 of Article 13 (Option A) or paragraph 3 of Article 13 (Option B) or not to apply any option. Under Option A, the specific activities mentioned in the tax treaties will not constitute a PE, insofar as the activities of the PE are preparatory and auxiliary in nature. In other words, the activities of a PE, even if aligned with sub-paragraphs (a) to (f) of Article 5(4), will only be exempt from being a PE if the overall conduct of the activities is preparatory and auxiliary in nature. A majority of the member States have agreed to this view.

Further, under Option B, paragraph 78 of the OECD Commentary (2017) provides that ‘some Member States consider that some of the activities referred to in Article 5(4) are intrinsically preparatory and auxiliary and, in order to provide greater certainty for both tax administrations and taxpayers, take the view that these activities should not be subject to the condition that they be of a preparatory or auxiliary character, and that concern about inappropriate use of the specific activity exemptions can be addressed through anti-fragmentation rules’. This option allows the member States to continue to use the existing language; however, at the same time they have agreed that an enterprise cannot fragment a cohesive business operation into smaller business operations in order to call it preparatory and auxiliary.

Paragraphs 2 & 3 of MLI Article 13

Article 5(4) of the OECD Model Tax Convention (2017) is modified to provide for Option A or Option B. Both the options preserve the specific variant of listed activities under each Covered Tax Agreement (CTA). It does not replace the list of exempt activities in the current CTAs with the above BEPS AP 7-suggested Article 5(4). Hence, in order to accommodate the model version and the existing version, Article 13 of the MLI provides for the following:

• Option A – provides additional condition that the specific activity exemption would apply only if the listed activities are of preliminary or auxiliary nature (POA) (remains explicit);

• Option B – provides automatic exemption to listed activities, irrespective of the same being POA in nature (i.e., remains explicit);

• If member states decide to not choose any option: the provisions of Article 5(4) as existing under the CTAs will remain in force (i.e., remain implicit).

|

Option A

|

Option B

|

|

Notwithstanding the

provisions of a Covered Tax Agreement that define the term ‘permanent

establishment’, the term

|

Notwithstanding the provisions of a Covered Tax

Agreement that define the term ‘permanent establishment’, the term

|

|

(continued)

‘permanent establishment’

shall be deemed not to include:

(a) The activities

specifically listed in the Covered Tax Agreement (prior to modification by

this Convention) as activities deemed not to constitute a permanent

establishment, whether or not that exception from permanent establishment

status is contingent on the activity being of a preparatory or auxiliary

character;

(b) The maintenance of a

fixed place of business solely for the purpose of carrying on, for the

enterprise, any activity not described in sub-paragraph a);

(c) The maintenance of a

fixed place of business solely for any combination of activities mentioned in

sub-paragraphs a) and b),

provided that such activity

or, in the case of sub-paragraph c), the overall activity of the fixed place

of business, is of a preparatory or auxiliary character

|

(continued)

‘permanent establishment’

shall be deemed not to include:

(a) The activities

specifically listed in the Covered Tax Agreement (prior to modification by

this Convention) as activities deemed not to constitute a permanent

establishment, whether or not that exception from permanent establishment

status is contingent on the activity being of a preparatory or auxiliary

character, except to the extent that the relevant provision of the Covered

Tax Agreement provides explicitly that a specific activity shall be deemed

not to constitute a permanent establishment provided that the activity is of

a preparatory or auxiliary character;

(b) The maintenance of a

fixed place of business solely for the purpose of carrying on, for the

enterprise, any activity not described in sub-paragraph a), provided that

this activity is of a preparatory or auxiliary character;

(c) The maintenance of a

fixed place of business solely for any combination of activities mentioned in

sub-paragraphs a) and b), provided that the overall activity of the fixed

place of business resulting from this combination is of a preparatory or

auxiliary character

|

An alternative rule is designed for those countries that are of the opinion that the examples stated under Article 5(4)(a) to Article 5(4)(d) of the OECD Model (2014) should always be deemed as not creating a PE, without the need to further go into the deliberation of whether or not they meet the general preparatory and auxiliary nature standard.

Paragraph 4 of MLI Article 13

Article 13(4) of the MLI relates to the anti-fragmentation rule wherein, irrespective of the above options (i.e., Option A or Option B or none), the member States will have another option to implement the anti-fragmentation rule. The objective is to avoid fragmentation of activities between closely-related parties so as to fall within the scope of preparatory and auxiliary character, and thereby avoid constituting a PE in the Source State. It provides as under:

‘Para 4. A provision of a Covered Tax Agreement (as it may be modified by paragraph 2 or 3) that lists specific activities deemed not to constitute a permanent establishment shall not apply to a fixed place of business that is used or maintained by an enterprise if the same enterprise or a closely related enterprise carries on business activities at the same place or at another place in the same Contracting Jurisdiction and:

a) that place or other place constitutes a permanent establishment for the enterprise or the closely related enterprise under the provisions of a Covered Tax Agreement defining a permanent establishment; or

b) the overall activity resulting from the combination of the activities carried on by the two enterprises at the same place, or by the same enterprise or closely related enterprises at the two places, is not of a preparatory or auxiliary character,

provided that the business activities carried on by the two enterprises at the same place, or by the same enterprise or closely related enterprises at the two places, constitute complementary functions that are part of a cohesive business operation.’

Accordingly, clause 4.1 is inserted to Article 5(4) of the OECD Model Convention and its commentary is provided in paragraphs 79 to 81 of the OECD Commentary (2017). Under Article 13(4) of the MLI (above), the scope for specific activity exemption is not available where there is at least one of the places where these activities are exercised (and) must constitute a PE or, if that is not the case, the overall activity resulting from the combination of the relevant activities must go beyond what is merely preparatory or auxiliary. Until now, the PE status remained embedded per se to its place of business through which the business activities were carried on. But now, the different places of business in the Source State would be combined and if at least one of the places constitutes a PE, then all places of business would constitute a PE for the enterprise as well as for its closely related enterprises carrying on activities in the said Source State. Accordingly, the profits attributable to the PE would be subject to tax in India.

BEPS AP 7 had made application of the anti-fragmentation rule mandatory for those opting for Option B, but the MLI has changed its applicability from mandatory to optional for all three options (including Option B).

India has opted for option A, i.e., wherein PE exemption to listed activities under Article 5(4) shall be subject to activities being preparatory-auxiliary in nature, whereas for the anti-fragmentation rule India is silent, indicating that this rule will be applicable if there is no reservation from the other contracting State in the CTA. It must be noted that in paragraph 51 of the Positions on Article 5, India states that it does not agree with the interpretation given in paragraph 74 because it considers that even when the anti-fragmentation provision is not applicable, an enterprise cannot fragment a cohesive operating business into several smaller operations in order to argue that each is merely engaged in a preparatory or auxiliary activity.

Understanding ‘complementary functions’ and ‘cohesive business operations’

In order to determine the preparatory and auxiliary character, the activity carried on would be compared with the main and core business of the enterprise. Further, based on Article 14 of the MLI, the activity so carried on would be combined with other activities that constitute ‘complementary functions’ that are part of a cohesive business carried on by the same enterprise or closely related enterprises in the same state. Neither MLI nor the OECD Commentary defines the terms ‘complementary functions’ and ‘cohesive business’. However, both these terms cannot be interpreted independently but together as a ‘part of’ the whole. Further, it refers to complementary functions, rather than complementary products or complementary business, etc., indicating interconnected (or closely connected) functions, or intertwined, or interdependent functions, with respect to technology, or value-added functions, or the nature of their ultimate purpose or use.

Paragraph 7 of the OECD Report on ‘Additional Guidance on the Attribution of Profits to Permanent Establishments’, BEPS AP 7, dated March, 2018, provides that ‘the anti-fragmentation rule recommended in the Report on Action 7 (at paragraph 39) is contained in the new paragraph 4.1 of Article 5. It prevents paragraph 4 from providing an exception from PE status for activities that might be viewed in isolation as preparatory or auxiliary in nature but that constitute part of a larger set of business activities conducted in the source country by the enterprise (whether alone or with a closely related enterprise) if the combined activities constitute complementary functions that are part of a cohesive business operation’.

Attribution of profits to PE

Paragraph 8 of the OECD Report on ‘Additional Guidance on the Attribution of Profits to Permanent Establishments’, BEPS AP 7, dated March, 2018, provides that Article 5(4.1) is applicable in two types of cases. First, it applies where the non-resident enterprise or a closely related enterprise already has a PE in the source country, and the activities in question constitute complementary functions that are part of a cohesive business operation. A determination will need to be made as to whether the activities of the enterprises give rise to one or more PEs in the source country under Article 5(4.1). The profits attributed to the PEs and subject to source taxation are the profits derived from the combined activities constituting complementary functions that are part of a cohesive business operation. This is considering the profits each one of them would have derived, if they were a separate and independent enterprise performing its corresponding activities, taking into account, in particular, the potential effect on those profits of the level of integration of these activities. Examples of this type of fact pattern are contained in new paragraph 30.43 of the revised Commentary (at point 40-41 of the Report on AP 7).

Paragraph 9 of the OECD Report on ‘Additional Guidance on the Attribution of Profits to Permanent Establishments’, BEPS AP 7, dated March 2018, provides that the second type of case to which Article 5(4.1) applies is a case where there is no pre-existing PE but the combination of activities in the source country by the non-resident enterprise and closely related non-resident enterprises results in a cohesive business operation that is not merely preparatory or auxiliary in nature. In such a case, a determination will need to be made as to whether the activities of the enterprises give rise to one or more PEs in the source country under Article 5(4.1). The profits attributable to each PE so arising are those that would have been derived from the profits made by each activity of the cohesive business operation as carried on by the PE, if it were a separate and independent enterprise, performing the corresponding activities taking into account, in particular, the potential effect on those profits of the level of integration of these activities.

Understanding ‘preparatory and auxiliary character’

Paragraph 60 of the OECD Commentary (2017) provides that an activity that has a preparatory character is one that is carried on in contemplation of what constitutes an essential and significant part of the activity of the enterprise as a whole. It is usually carried on for a relatively short period, which, depending on the circumstance, could be carried on for a longer duration. Auxiliary activity supports the essential and significant part of the activity. In absolute terms, auxiliary activities would not require significant proportion of the assets or employees, when compared with the total assets or employees of the enterprise.

Further, Paragraph 61 of the OECD Commentary (2017) provides that the activity purported to be covered under the specified activity exemptions ought to be carried on for the enterprise itself. If the activity is undertaken on behalf of the other enterprises at the same fixed place of business, the said activity would not be exempt from the PE status in the garb of Article 5(4) of the applicable tax treaty. The OECD Commentary (2017) provides an example that if an enterprise that maintained an office for the advertising of its own products or services, which was also engaged in advertising on behalf of other enterprises at that location, would be regarded as a PE of the enterprise.

Understanding ‘closely related enterprises’

Article 15 of the MLI defines the term ‘Closely Related Enterprises’ (CRE). The concept of CRE is distinguished from the concept of ‘Associated Enterprises’ of Article 9 of the OECD Model Convention. It is important to note that the term ‘control’ is not defined therein. Further, the member States that have made reservations to Article 12-14 of the MLI can opt out of Article 15.

‘Article 15 – Definition of a Person Closely Related to an Enterprise

1. For the purposes of the provisions of a Covered Tax Agreement that are modified by paragraph 2 of Article 12 (Artificial Avoidance of Permanent Establishment Status through Commissionnaire Arrangements and Similar Strategies), paragraph 4 of Article 13 (Artificial Avoidance of Permanent Establishment Status through the Specific Activity Exemptions), or paragraph 1 of Article 14 (Splitting-up of Contracts), a person is closely related to an enterprise if, based on all the relevant facts and circumstances, one has control of the other or both are under the control of the same persons or enterprises. In any case, a person shall be considered to be closely related to an enterprise if one possesses directly or indirectly more than 50 per cent of the beneficial interest in the other (or, in the case of a company, more than 50 per cent of the aggregate vote and value of the company’s shares or of the beneficial equity interest in the company) or if another person possesses directly or indirectly more than 50 per cent of the beneficial interest (or, in the case of a company, more than 50 per cent of the aggregate vote and value of the company’s shares or of the beneficial equity interest in the company) in the person and the enterprise.

2. A party that has made the reservations described in paragraph 4 of Article 12 (Artificial Avoidance of Permanent Establishment Status through Commissionnaire Arrangements and Similar Strategies), sub-paragraph a) or c) of paragraph 6 of Article 13 (Artificial Avoidance of Permanent Establishment Status through the Specific Activity Exemptions), and sub-paragraph a) of paragraph 3 of Article 14 (Splitting-up of Contracts) may reserve the right for the entirety of this Article not to apply to the Covered Tax Agreements to which those reservations apply.’

India has adopted Article 15 of the MLI. However, India has reserved its right to not include the words ‘to which it is closely related’ in Article 5(6) of the OECD Model Convention (2017). For instance, India has not reserved the right to paragraph 4 of Article 13 of the MLI, which means that it has accepted to bring the anti-fragmentation rule to the existing tax treaties. Again, this can only be confirmed if the other contracting state doesn’t create reservation to paragraph 4 of Article 13.

Paragraph 5 to 8 of MLI Article 13

Paragraph 5 contains compatibility clauses which describe the relationship between Article 13(2) through (4) and provisions of CTA. Paragraph 6 contains reservation rights of the member States, indicating that the provisions addressing the concerns of BEPS AP 7 are not required in order to meet a minimum standard test. The member State may reserve the right for the entirety of Article 13 of MLI not to apply to its CTAs.

Paragraph 7 requires that parties that opted for Option A or Option B to notify the depository of the Option so selected. Paragraph 180 of the Explanatory Statement further confirms that ‘An Option would apply to a provision only where all Contracting Jurisdictions have chosen to apply the same Option and have made such a notification with respect to that provision’. For example, if a contracting State chooses Option A while the other chooses Option B, the asymmetrical decisions conclude in the non-application of the provision in its entirety. This is illustrated in paragraph 7 of Article 13, which states that ‘an Option shall apply with respect to a provision of a CTA only where all Contracting Jurisdictions have chosen to apply the same Option and have made such a notification’. Accordingly, India has selected and notified Option A. Unless the other contracting State selects Option A, the tax treaty will remain unchanged.

Paragraph 8 requires each party that has not opted out of applying Paragraph 4 (anti-fragmentation rule) or for the entirety of Article 13, to notify the depository of each of its CTAs that includes specific activity exemptions. Paragraph 181 of the Explanatory Statement further confirms that ‘Paragraph 4 will apply to a provision of a CTA only where all Contracting Jurisdictions have made such a notification with respect to that provision pursuant to either paragraph 7 or paragraph 8.’

The extract of Article 13(5) to Article 13(8) is provided below:

‘Para 5. a) Paragraph 2 or 3 shall apply in place of the relevant parts of provisions of a Covered Tax Agreement that list specific activities that are deemed not to constitute a permanent establishment even if the activity is carried on through a fixed place of business (or provisions of a Covered Tax Agreement that operate in a comparable manner).

b) Paragraph 4 shall apply to provisions of a Covered Tax Agreement (as they may be modified by paragraph 2 or 3) that list specific activities that are deemed not to constitute a permanent establishment even if the activity is carried on through a fixed place of business (or provisions of a Covered Tax Agreement that operate in a comparable manner).

Para 6. A Party may reserve the right: a) for the entirety of this Article not to apply to its Covered Tax Agreements; b) for paragraph 2 not to apply to its Covered Tax Agreements that explicitly state that a list of specific activities shall be deemed not to constitute a permanent establishment only if each of the activities is of a preparatory or auxiliary character; c) for paragraph 4 not to apply to its Covered Tax Agreements.

Para 7. Each party that chooses to apply an Option under paragraph 1 shall notify the Depository of its choice of Option. Such notification shall also include the list of its Covered Tax Agreements which contain a provision described in sub-paragraph a) of paragraph 5, as well as the article and paragraph number of each such provision. An Option shall apply with respect to a provision of a Covered Tax Agreement only where all Contracting Jurisdictions have chosen to apply the same Option and have made such a notification with respect to that provision.

Para 8. Each party that has not made a reservation described in sub-paragraph a) or c) of paragraph 6 and does not choose to apply an Option under paragraph 1 shall notify the Depository of whether each of its Covered Tax Agreements contains a provision described in sub-paragraph b) of paragraph 5, as well as the article and paragraph number of each such provision. Paragraph 4 shall apply with respect to a provision of a Covered Tax Agreement only where all Contracting Jurisdictions have made a notification with respect to that provision under this paragraph or paragraph 7.’

India context: Impact analysis of key India tax treaties:

|

India’s notification

|

Particulars of Article 13

|

Australia

|

UK

|

Singapore

|

France

|

Netherlands

|

|

Notified Option A, i.e., India’s tax treaties will be modified

with the language of Article 13(2)

|

Specific activity exemption

|

Notified Option A paragraph 13(2) modified India-Australia

Treaty Article 5(4)

|

Not selected Option A or B, Treaty remains the same

|

Notified Option B, the Treaty remains unchanged

|

Notified Option B, the Treaty remains unchanged

|

Notified Option A, paragraph 13(2) modified India-Australia

Treaty Article 5(4)

|

|

Remained silent to reserve Article 13(4), i.e., the provisions

will apply to the existing tax treaties

|

Anti- fragmentation rule

|

Notified paragraph 13(4), Treaty changes

|

Notified paragraph 13(4), Treaty changes

|

Reservation to Article 13(4) – No change in

the Treaty

|

Remained silent – Treaty changes

|

Notified paragraph 13(4), Treaty changes

|

CONCLUSION

The specific activity exemption provisions are important from the point of view of the relief they provide to non-resident entities who have only incidental activities in India. Hence, one needs to be careful while applying these provisions to a particular case. The amendment provided in Article 13 of the MLI is largely impacting industries such as e-commerce / EPC / consumer, wherein foreign companies have typically been taking exemptions from PE pursuant to the negative list / anti-fragmenting activities in India. However, on account of amendments made by Article 13, it is imperative for all foreign companies to revisit their existing PE positions.