By Anil Sathe | Chaitee Londhe, Chartered Accountants

The Hon’ble Finance Minister, during the Union Budget presentation, repeatedly emphasised the government's endeavour to simplify taxation. This series of articles on the Finance (No. 2) Act of 2024 has thoroughly analysed various amendments to the Income-tax Act, 1961 (“the Act”) in five earlier parts, bringing out various nuances of these amendments and helping readers assess whether this promise of simplification has been realised.

In this Article, we continue this analysis, examining a few other significant amendments made to the Act.

(A) AMENDMENTS RELATING TO TDS AND TCS:

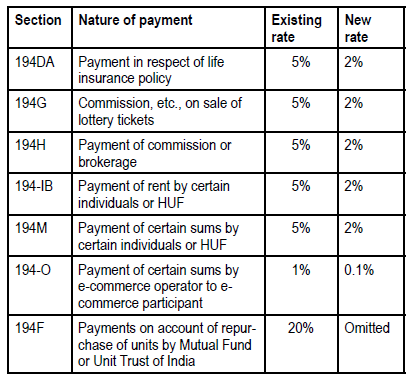

Reduction in TDS rates:

A series of welcome amendments in the following sections of the Act has been made, reducing the rates of TDS w.e.f. 1st October, 2024 as under:

It may be pointed out that in addition to the above, the Memorandum explaining the provisions of the Finance Bill (“Memorandum”) also contained a proposal to reduce the rate of TDS applicable to payments of insurance commissions u/s 194D of the Act from 5 per cent to 2 per cent in case