By Sunil Gabhawalla | Rishabh Singhvi | Parth Shah, Chartered Accountants

Refunds under tax enactments arise as a matter of Government policy or pursuant to excess payments. The legislative source of such refunds plays a pivotal role in deciding the entitlement criteria, process, limitation, restriction, etc.; and hence should not be lost sight of, while studying refund provisions. This article is aimed at examining the structural aspects of refunds under GST law.

I. INTRODUCTION : LEGAL FRAMEWORK

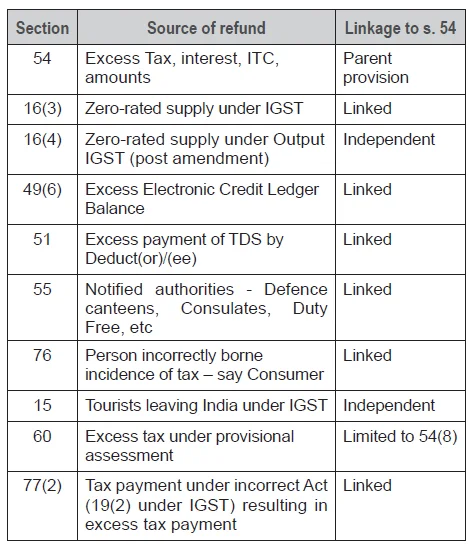

Refund entitlements are present across the entire GST law – a simple tabulation summarises this array1. While the provisions are scattered, section 54 appears to be the parent provision for processing GST refunds. Hence, the refund entitlements can be basketed into those which are: (a) specifically mapped to S. 54 for conditions, restrictions, etc (b) not specifically mapped to S. 54.

-

The list excludes refund entitlements under Central / State Industrial or

Budgetary policies which would be governed by the respective

notifications issued by the administering Ministry.

On a perusal of the various refund provisions, it is noteworthy that most of the refund cl