March 2024

Section 92C, read with section 92B, of the Income-tax Act, 1961 — In light of peculiar facts, TPO was correct in recharacterizing part consideration of merger in form of cash and CCD as income. Cash payment was to be treated as deemed loan and ALP for CCD interest was determined at Nil.

By Geeta Jani | Dhishat B Mehta | Bhaumik Goda, Chartered Accountants

14 Dimexon Diamonds Ltd vs. ACIT

[2024] 159 taxmann.com 118 (Mumbai - Trib.)

ITA No: 2429/Mum/2022

A.Ys.: 2018–19

Date of Order: 30th January, 2024

Section 92C, read with section 92B, of the Income-tax Act, 1961 — In light of peculiar facts, TPO was correct in recharacterizing part consideration of merger in form of cash and CCD as income. Cash payment was to be treated as deemed loan and ALP for CCD interest was determined at Nil.

FACTS

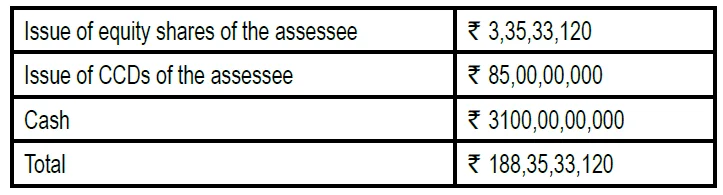

DIHPL, an Indian company, was a wholly owned subsidiary of DIHBV, a Netherlands company. Assessee, another Indian company, was a wholly owned subsidiary of DIHPL. DIHPL and the assessee undertook a reverse merger whereby DIHPL merged into the assessee. Assessee discharged following consideration to DIHBV, which held the entire equity capital of DIHPL.

In the transfer pricing report, the assessee disclosed the